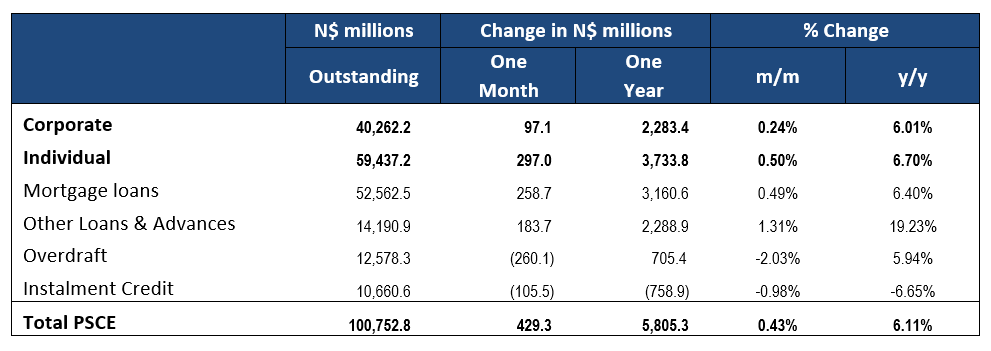

Overall

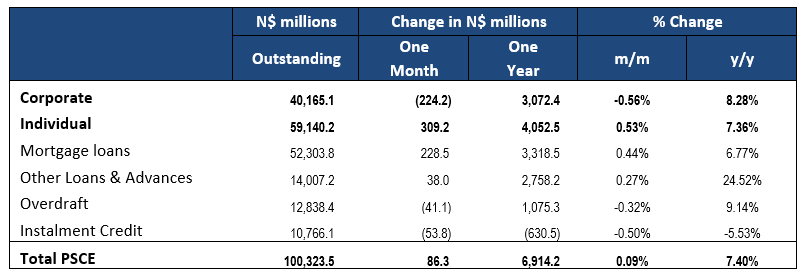

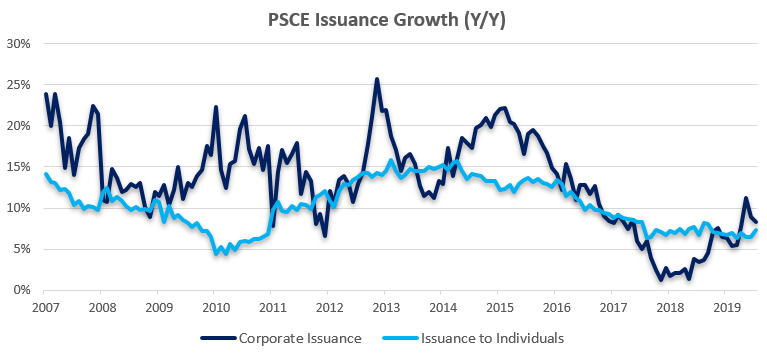

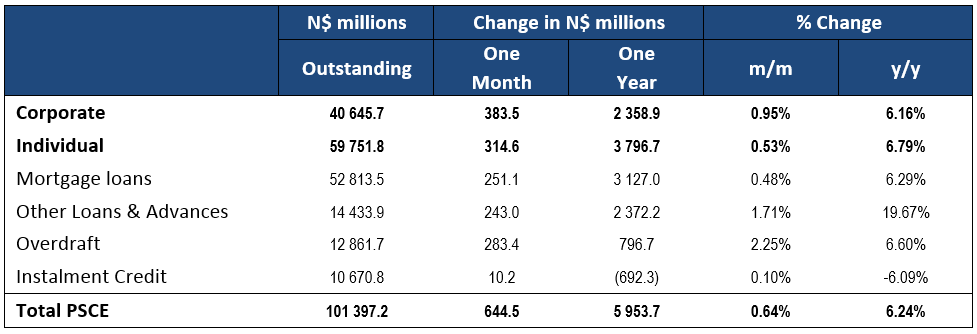

Private sector credit (PSCE) increased by N$644.5 million or 0.64% m/m in September, bringing the cumulative credit outstanding to N$101.4 billion. PSCE grew at a marginally faster rate of 6.2% y/y in September compared to 6.1% y/y in August. On a rolling 12-month basis N$5.95 billion worth of credit was extended to the private sector, down 10.2% y/y. Individuals took up N$3.80 billion while N$2.36 billion was extended to corporates, and the non-resident private sector decreased their borrowings by N$201.9 million.

Credit Extension to Individuals

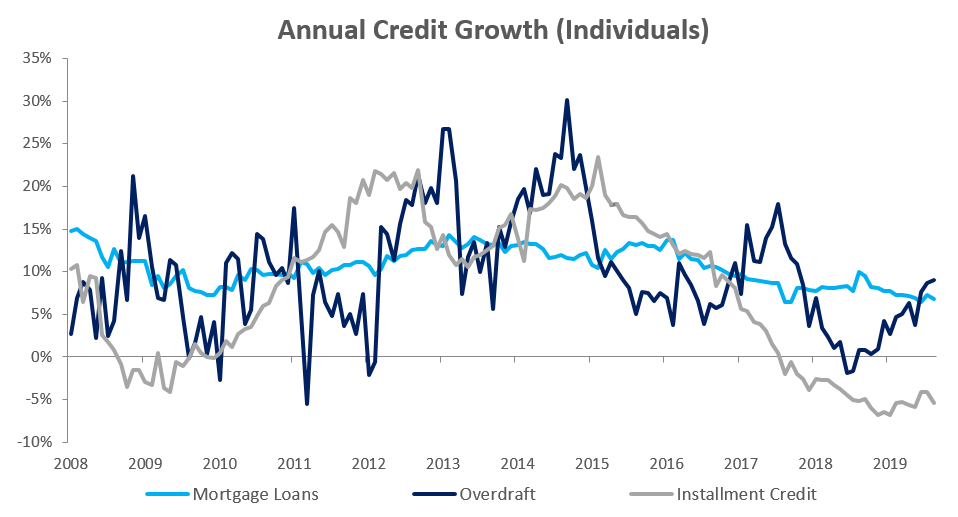

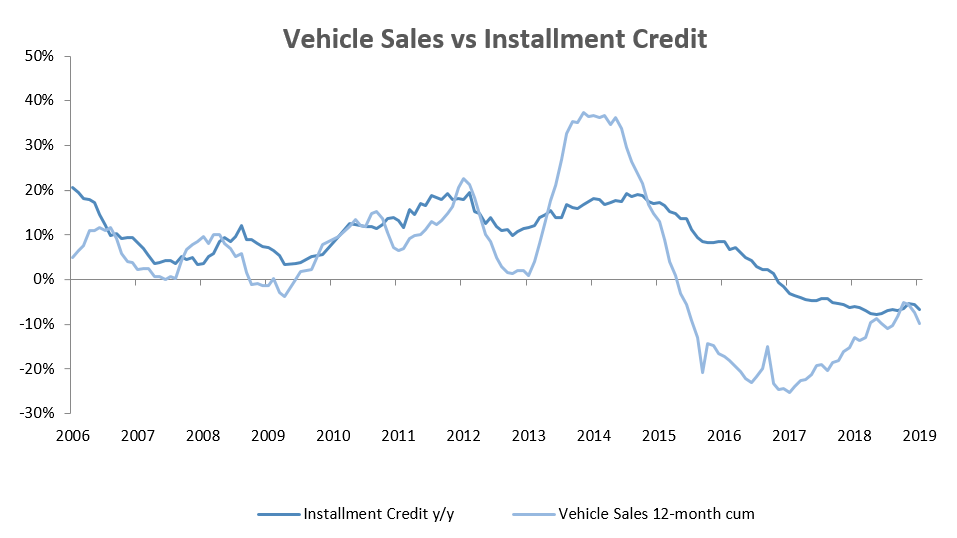

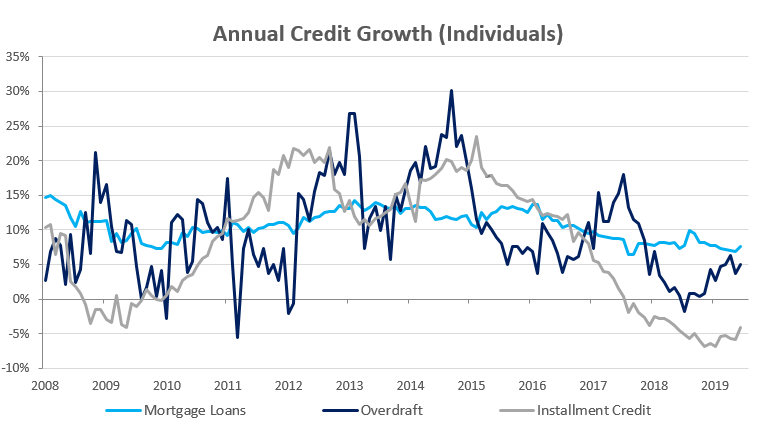

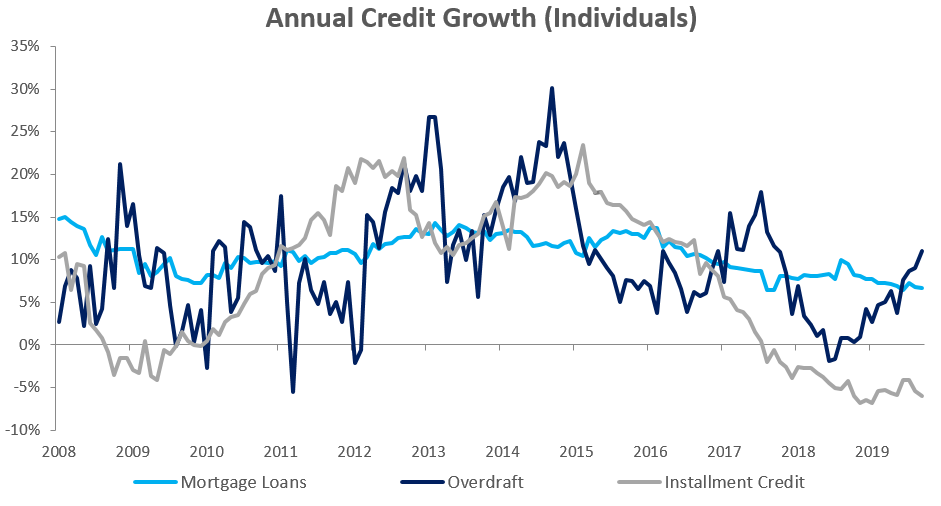

Credit extended to individuals increased by 6.8% y/y in September, almost unchanged from the 6.7% y/y growth recorded in August. Mortgage loans extended to individuals increased by 0.4% m/m and 6.7% y/y. Installment credit continued to contract, by 0.7% m/m and 6.0% y/y. Other loans and advances (which is made up of credit card debt, personal and term loans) grew by 2.3% m/m and 23.1% y/y in September. Household demand for overdraft facilities remained relatively strong in September, increasing by 1.8% m/m and 11.0% y/y.

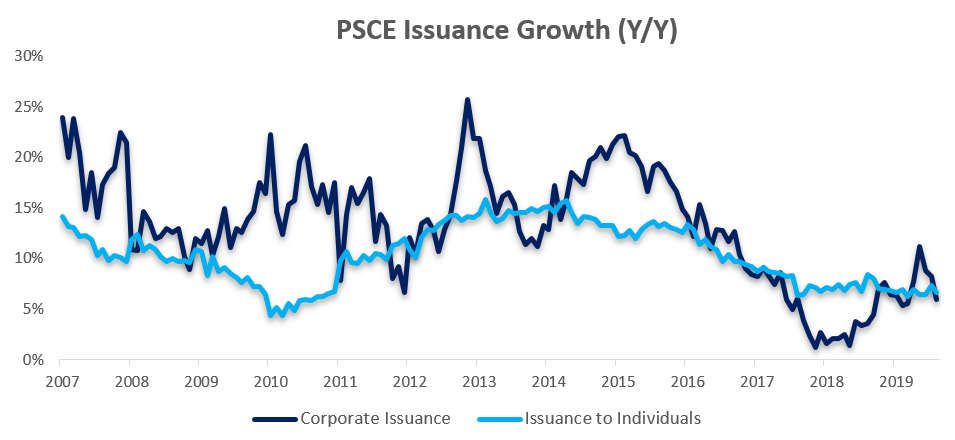

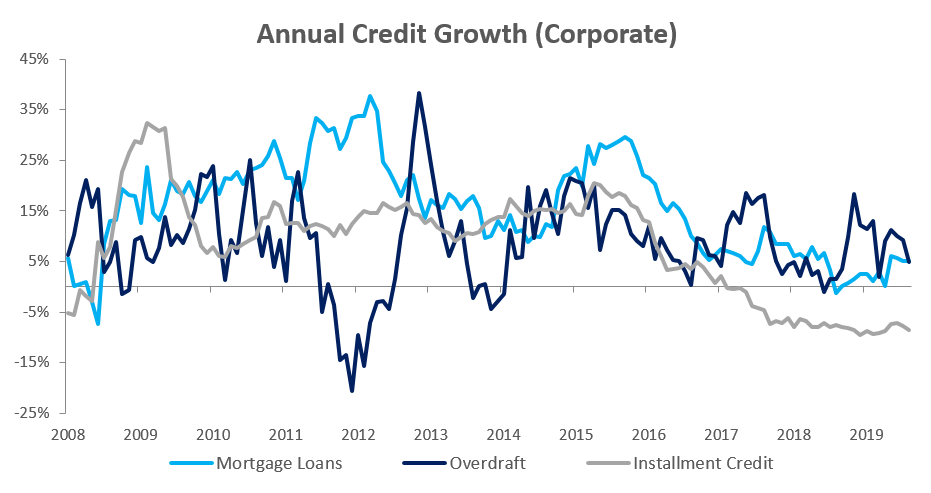

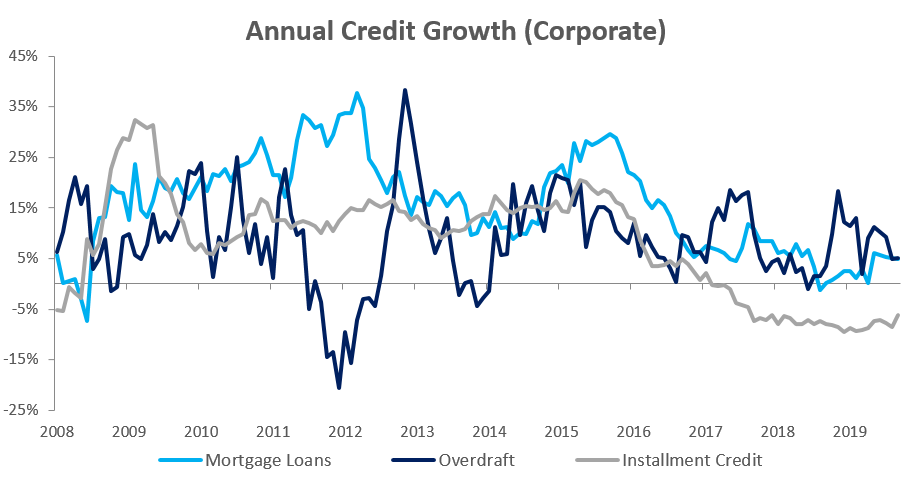

Credit Extension to Corporates

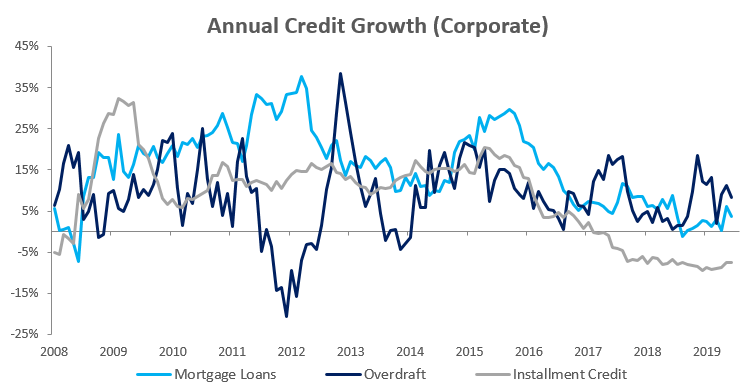

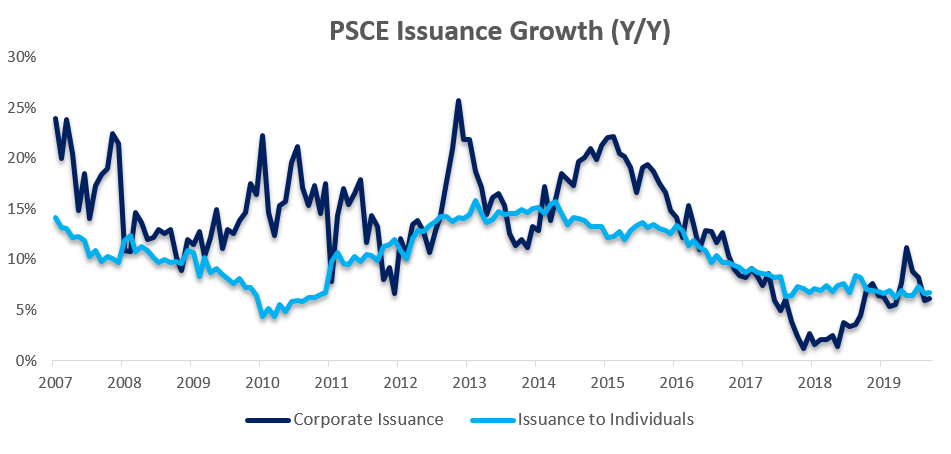

Credit extension to corporates grew by 1.0% m/m and 6.2% y/y. On a rolling 12-month basis N$2.36 billion was extended to corporates as at the end of September, an increase of 44.1% y/y. Although the uptick in the general demand for credit by corporates over the last year seems positive, the biggest driver of the increase in credit extended to corporates was shorter-term debt. Overdraft facilities extended to corporates grew by 2.4% m/m and 5.1% y/y, while other loans and advances to corporates increased by 1.1% m/m and 16.0% y/y. The increase in these categories indicates that businesses are still relying on overdrafts and credit card debt to keep the lights on. Mortgage loans by corporates increased by 1.0% m/m and 4.9% y/y, while installment credit increased by 1.4% m/m, but contracted by 6.2% y/y.

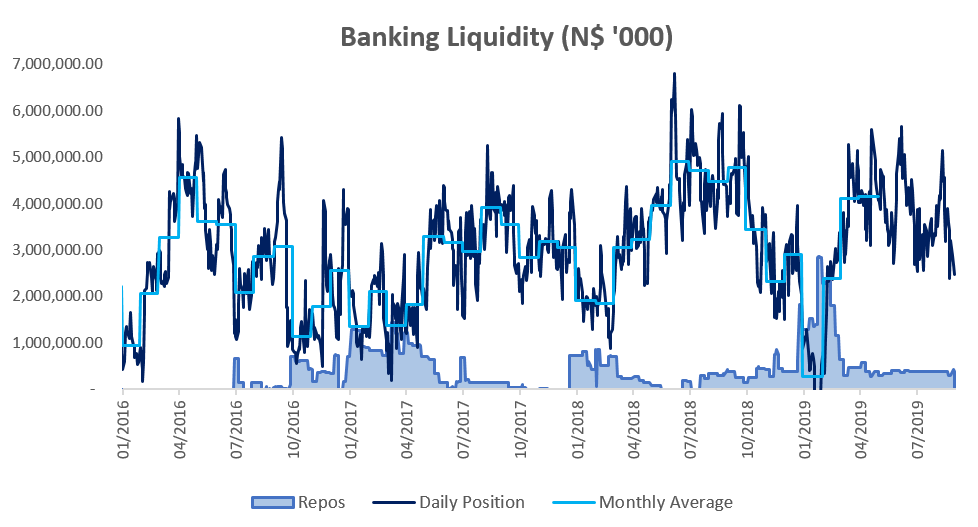

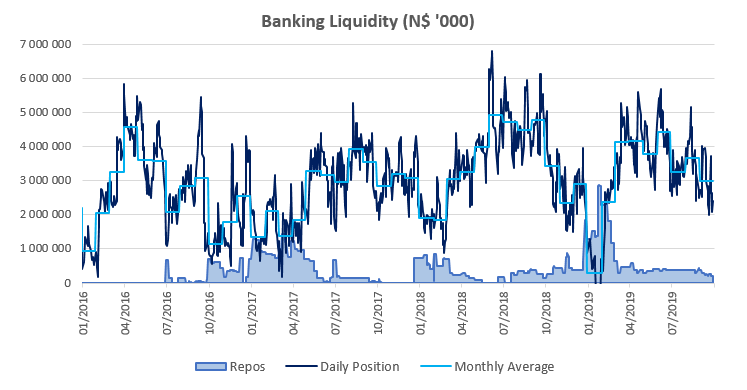

Banking Sector Liquidity

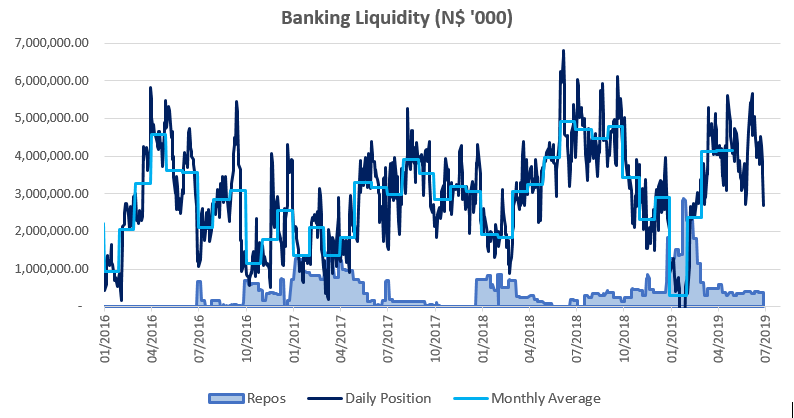

The overall liquidity position of commercial banks declined by N$670.0 million in September to reach an average of N$2.99 billion. The Bank of Namibia attributed the decline in liquidity to lower domestic Government spending mainly due to lower economic activity coupled with higher foreign currency outflows as a result of import payments during the review period.

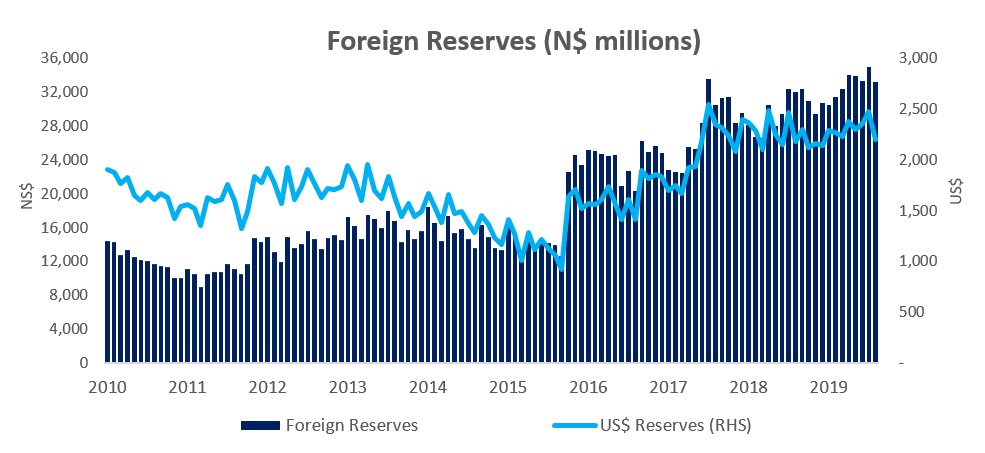

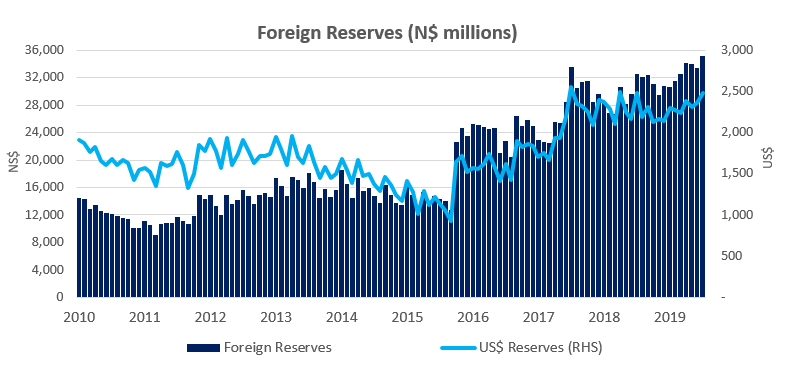

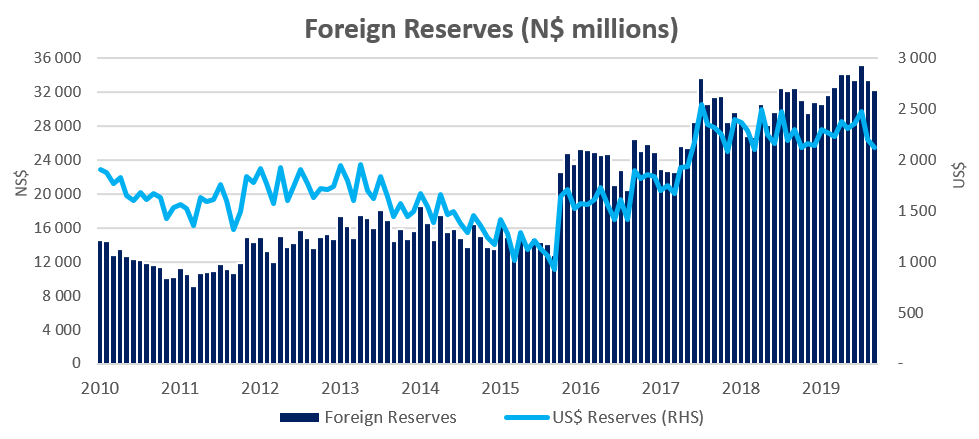

Reserves and Money Supply

As per the BoN’s latest money statistics release, broad money supply rose by N$1.34 billion or 8.4% y/y in September, following an 8.0% y/y increase in August. Foreign reserve balances fell by N$1.16 billion to N$32.3 billion in September from N$33.4 billion in August. According to the BoN, the decrease was mostly due to an increase in net foreign capital outflows during the period under review.

Outlook

Private sector credit extension continues to languish, increasing by 6.2% y/y during September. It has been 35 months since PSCE last recorded double digit growth. As expected, the 25-basis point rate cut in August has not resulted in higher demand for credit, as consumers are already overindebted and growth opportunities for businesses are few due to a lack of demand. As mentioned earlier, corporates continue to rely on short-term debt to keep the lights on instead of taking on longer-term credit to invest in capital projects to expand operations. We do not expect conditions to improve in the short- to medium-term.