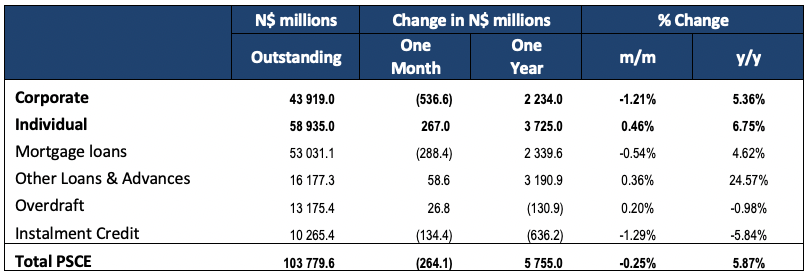

Overall

Private sector credit (PSCE) declined by N$1.23 billion or 1.19% m/m in April, bringing the cumulative credit outstanding to N$102.42 billion. On a year-on-year basis, private sector credit increased by 3.4% in April, compared to 5.8% in March. While this is still positive growth, it is the lowest annual growth rate on our records dating back to 2002. On a rolling 12-month basis, N$3.32 billion worth of credit was extended to the private sector. Of this cumulative issuance, individuals took up the lion’s share of credit, amassing N$3.15 billion worth of debt while N$485 million was extended to businesses. The non-resident private sector decreased their borrowings by N$312 million.

Credit Extension to Individuals

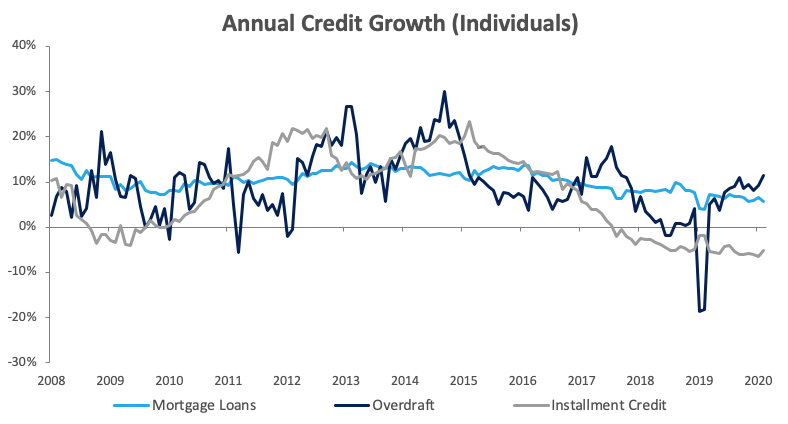

Credit extended to individuals increased by 5.7% y/y in April, compared to 7.2% y/y recorded in March. On a monthly basis, household credit decreased by 0.7% following the increase of 0.4% recorded in March. This decline was mostly a result from individuals paying back overdrafts during the month, resulting in a 16.0% m/m decrease in this category. Other loans and advances (or OLA, which is made up of credit card debt, personal and term loans) grew by 4.3% m/m and 22.3% y/y in April. Installment credit contracted by 3.3% m/m and 6.9% y/y. The value of mortgage loans extended to individuals declined by 0.1% m/m, but increased by 5.2% y/y.

Credit Extension to Corporates

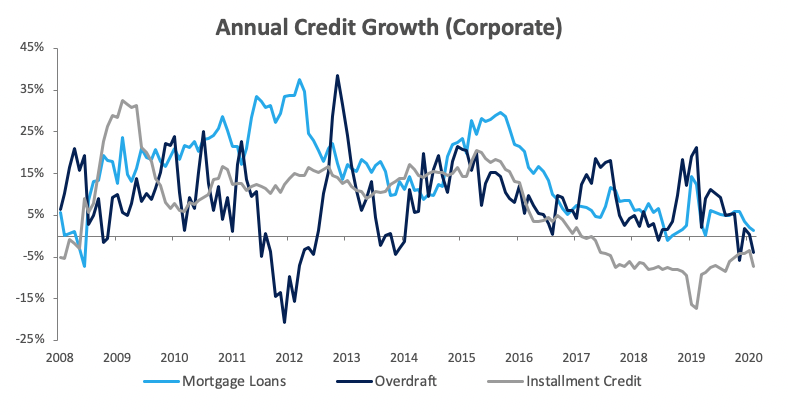

Credit extended to corporates contracted for a third straight month, declining by 1.5% m/m in April. On a year-on-year basis credit extension to corporates grew by a mere 1.1%, compared to the 4.6% y/y growth registered in March. The monthly decline can mostly be attributed to repayments of ‘other loans and advances’ by corporates which decreased by 3.0% m/m, but grew by 10.6% y/y. Overdraft facilities extended to corporates increased by 0.2% m/m, but fell 4.3% y/y. The persistent contraction in installment credit continued in April, declining by 1.4% m/m and 7.1% y/y. Leasing transactions to corporations declined by 2.7 m/m and 21.5% y/y. Mortgage loans extended to corporates contracted by 1.3% m/m. The Bank of Namibia (BoN) attributes this category’s decline to repayments made by businesses in the tourism and real estate sectors. This makes sense given that these sectors were harshly impacted by the lockdowns, and would not have taken up new mortgage loans to expand their businesses.

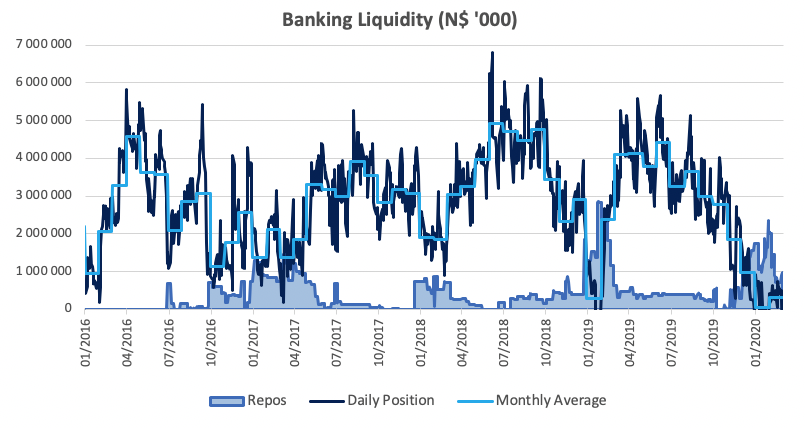

Banking Sector Liquidity

The overall liquidity position of commercial banks improved substantially during April, increasing by N$3.08 billion to reach an average of N$3.33 billion. The balance of repo’s outstanding fell from N$1.52 billion at the start of April to N$147.4 million at the end of the month. The BoN ascribed the spike in the liquidity level to fiscal operations after the government redeemed the GC20 bond, as well as several payments made by the government such as the COVID-19 stimulus package and VAT refunds.

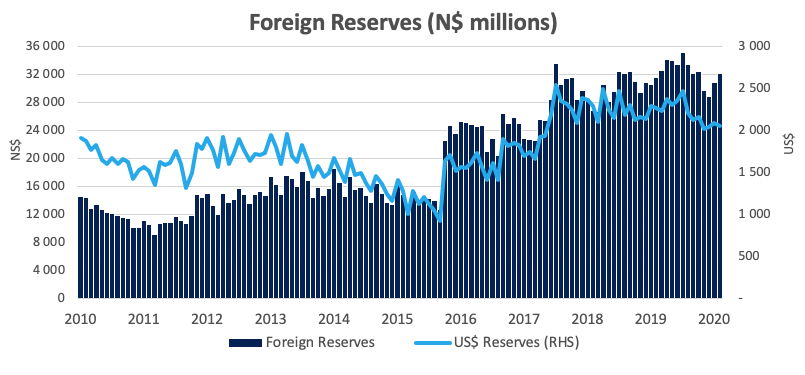

Reserves and Money Supply

As per the BoN’s latest money statistics release, broad money supply rose by N$4.35 billion or 13.0% y/y in April. Foreign reserve balances rose by N$2.57 billion to N$35.5 billion in April. According to the BoN, this increase due to SACU receipts of N$5.2 billion that were received during the month coupled with exchange rate revaluations due to the Namibian dollar against major currencies.

Outlook

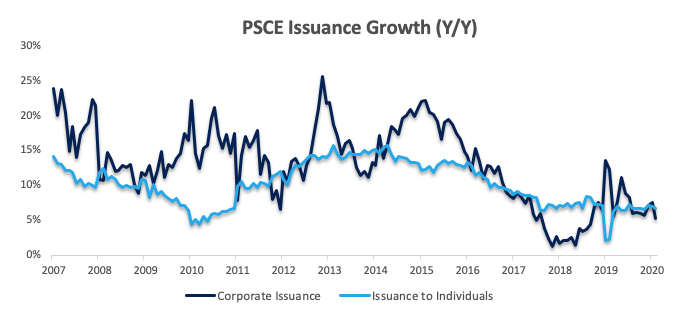

Private sector credit extension continued to languish, increasing by 3.5% m/m during April. It has been 42 months since PSCE last recorded double digit growth. Rolling 12-month private sector credit issuance is down 46.6% from the N$6.23 billion figure as at April 2019. Rolling 12-month private sector credit issuance of N$3.32 billion is now at levels last seen in 2010.

Instead of taking on additional long-term credit, many businesses would have applied for payment holidays on their existing credit facilities, as the government imposed lockdowns wiped out their revenues. It is for this same reason that commercial banks would have been extra prudent in extending credit during April as the risk of default would have increased because the general economic malaise. We believe that the BoN will follow the SARB decision in cutting the repo rate by 50 basis points at its June meeting. While this should provide some relief to indebted consumers and businesses, it is unlikely that it will increase the risk appetite of the banks and we therefore stick to the view that we don’t anticipate that the more accommodative monetary policy will be effective in stimulating economic activity to the extent that it eliminates the impact of the external shock to the economy.

Going forward we expect that a portion of credit extension will be distressed borrowing by businesses and consumers as economic conditions are expected to remain dire. We don’t foresee businesses in general making use of credit to invest in large capital projects any time soon.