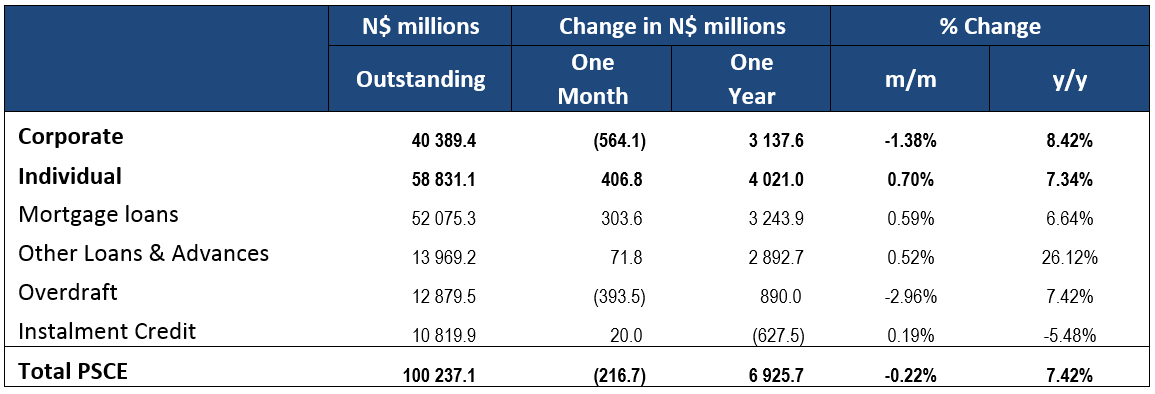

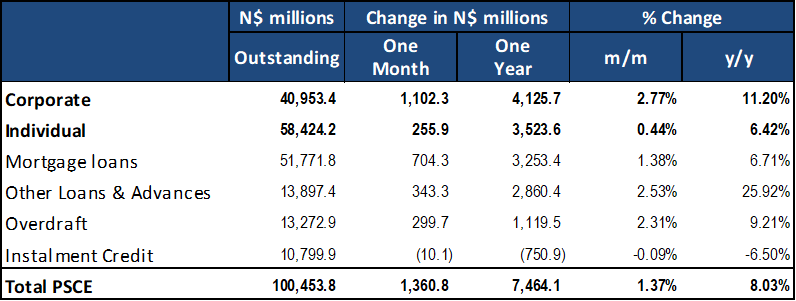

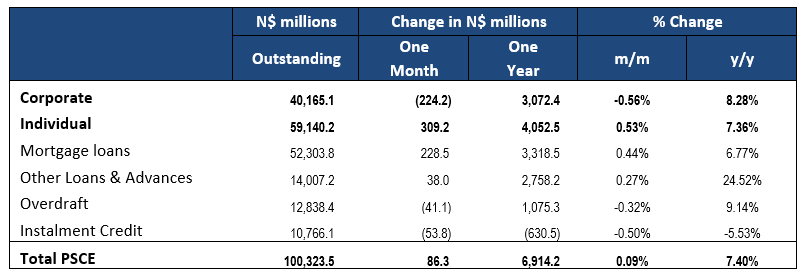

Private sector credit extension (PSCE) increased by N$86.3 million or 0.09% m/m in July, bringing the cumulative credit outstanding to N$100.32 billion. On a year-on-year basis, private sector credit extension saw a steady increased of 7.4% in July, as seen in the preceding month. On a rolling 12-month basis N$6.9 billion worth of credit was extended to the private sector, with individuals taking up N$4.1 billion while N$3.1 billion was extended to corporates, and the non-resident private sector has decreased their borrowings by N$210.7 million.

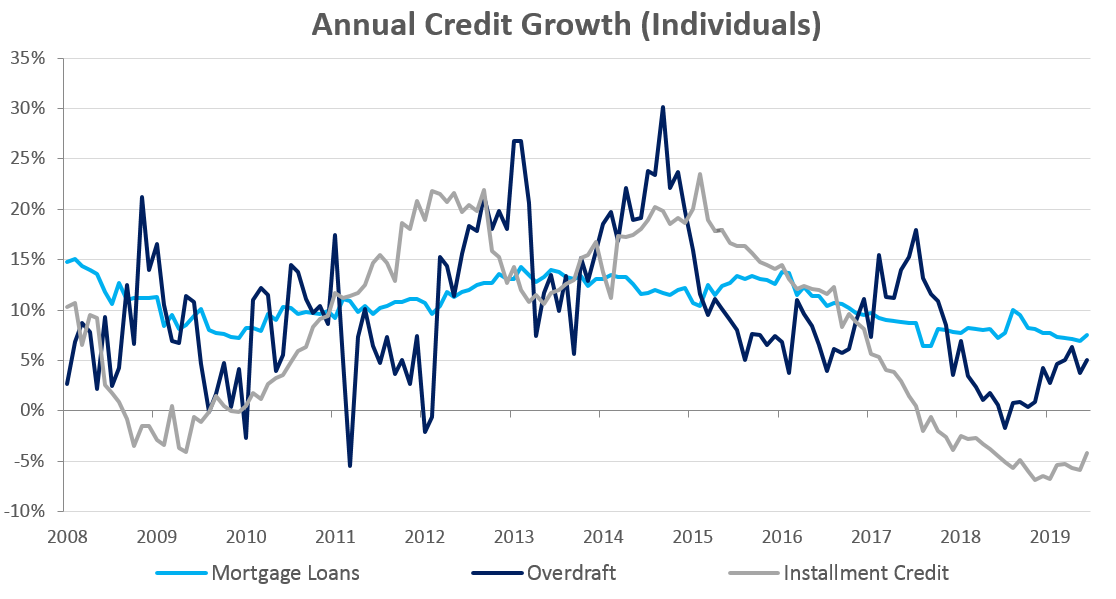

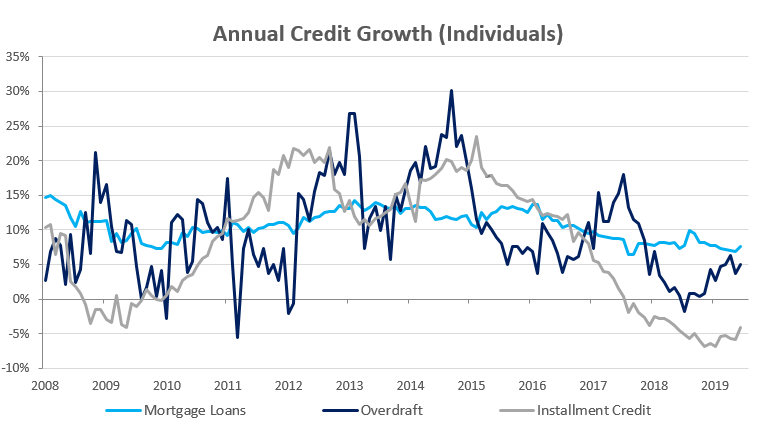

Growth in credit extension to individuals increased by 0.5% m/m and 7.4% y/y in July, compared to 0.7% m/m and 6.5% y/y growth recorded in June. Other loans and advances (which is made up of credit card debt, personal and term loans) grew by 0.6% m/m and 27.3% y/y in July. The increase in the uptake of short-term debt remains of concern as household demand continues to rise when compared to the use of more productive loans such as mortgages. Short term debt is characterized by high interest rates and high default rates compared to mortgage loans. Installment credit, often used to finance vehicles contracted by 0.3% m/m and 4.1% y/y. Mortgage loans to individuals grew by 0.7% m/m and 7.3% y/y, while overdraft facilities extended to individuals have increased by 1.0% m/m and 8.7% y/y.

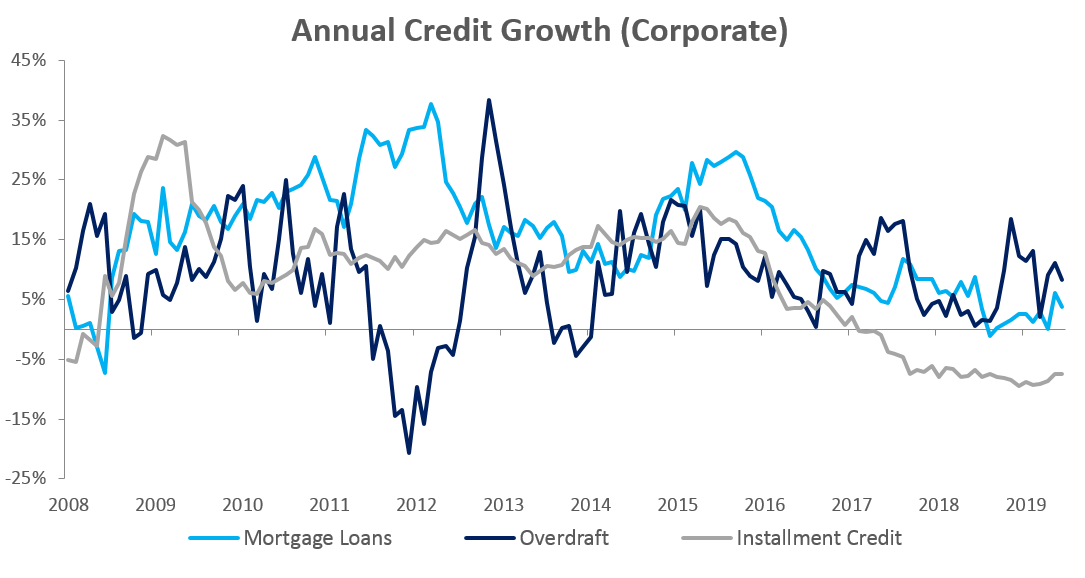

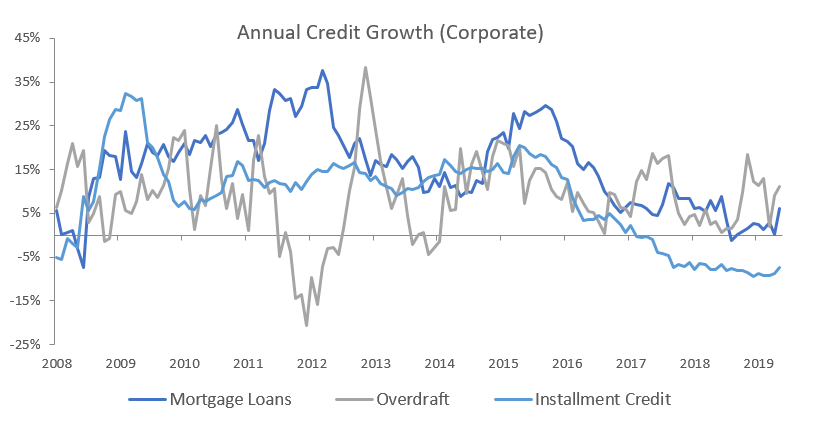

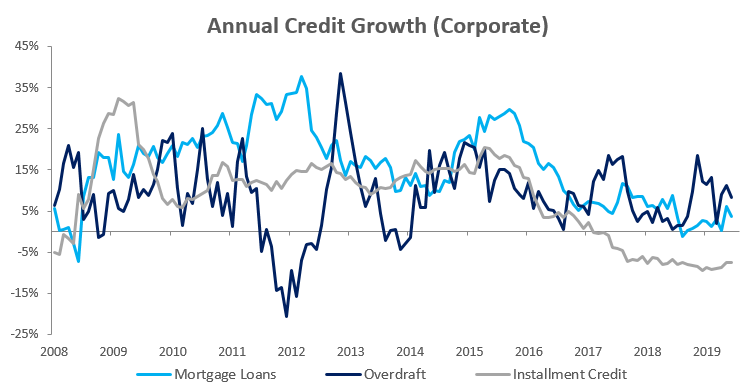

Credit extension to corporates further contracted by 0.6% m/m following the 1.4% m/m contraction recorded in June. On an annual basis, however, credit extension to corporates increased by 8.3% y/y in July, compared to the 8.9% y/y growth registered in June. Overdraft facilities extended to corporates decreased by 0.8% m/m, but are still up 9.3% y/y. The year-on-year increase was caused by business in the fisheries and housing sector taking on overdrafts facilities. Mortgage loans to corporates contracted by 0.5% m/m but increased by 5.2% y/y. Installment credit extended to corporates, which has been contracting since February 2017 on an annual basis, remained depressed, contracting by 0.7% m/m and 7.7% y/y in July.

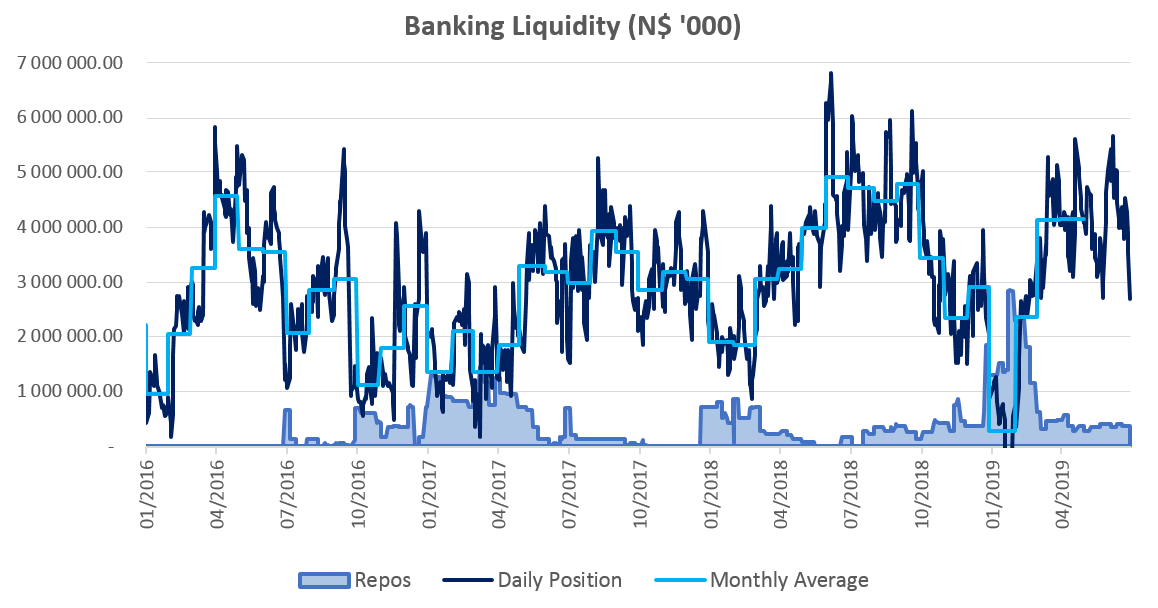

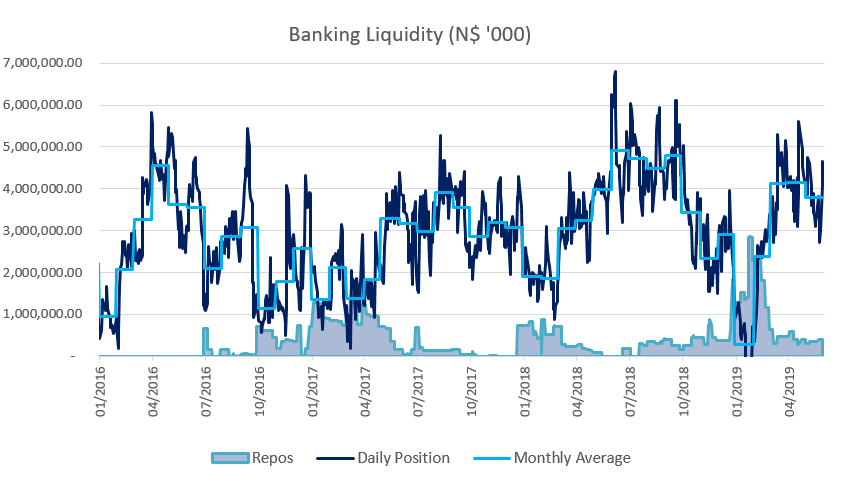

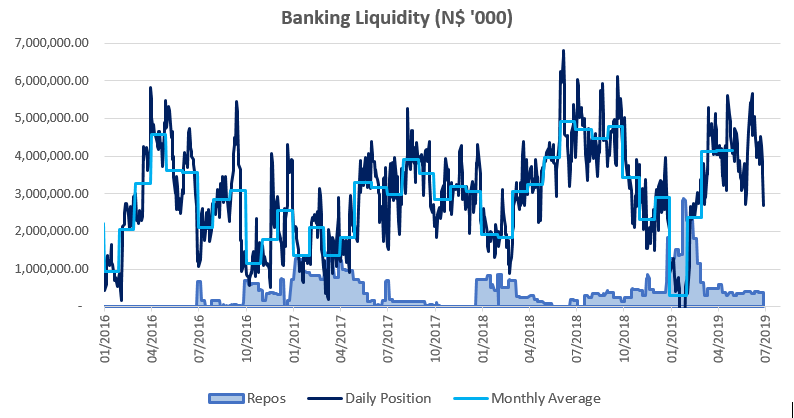

The overall liquidity position of commercial banks declined by N$1.2 billion to reach an average of N$3.25 billion. The Bank of Namibia (BoN) attributes the decline in liquidity balances to outflows as a result of payments of corporate taxes during the period under review. The decreased liquidity resulted in an increase in the use of the BoN’s repo facility by commercial banks, with the outstanding balance of repo’s increasing from N$388.7 million at the start of July to N$391.5 million by month end.

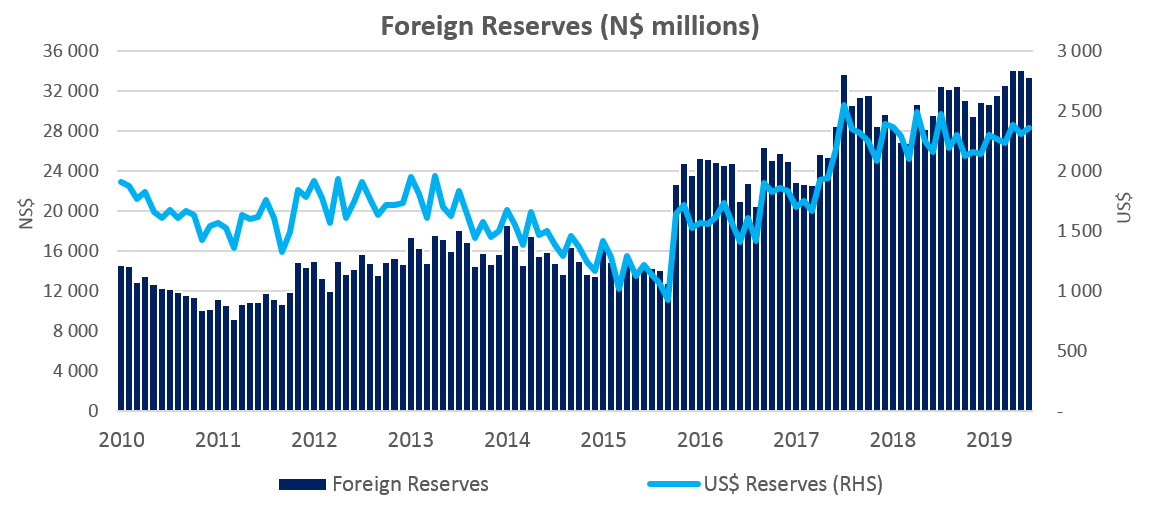

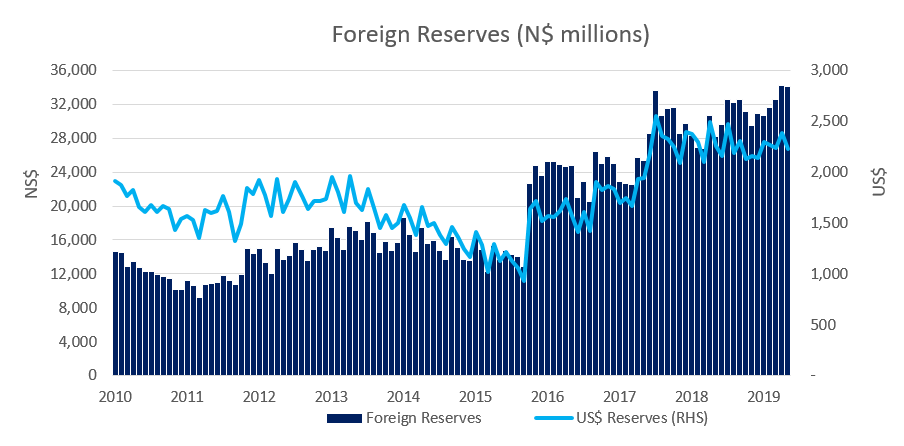

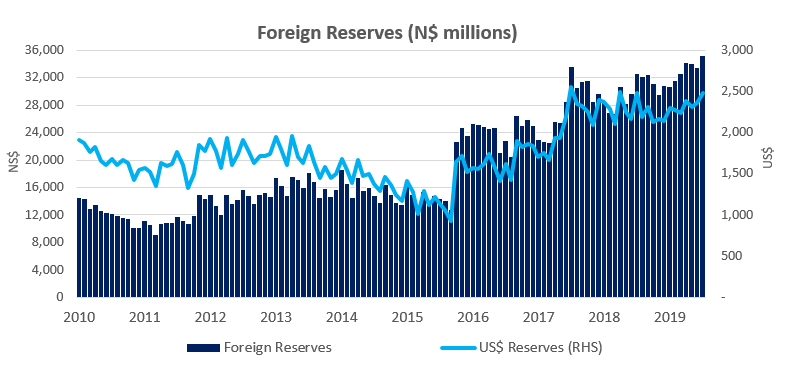

As per the BoN’s latest money statistics release, broad money supply rose by N$6.74 billion or 6.6% y/y in July, following a 7.3% y/y increase in June. Foreign reserve balances rose by N$1.75 billion to N$35.2 billion in July from N$33.4 billion in June. According to BoN this was largely due to SACU payments received during the month under review.

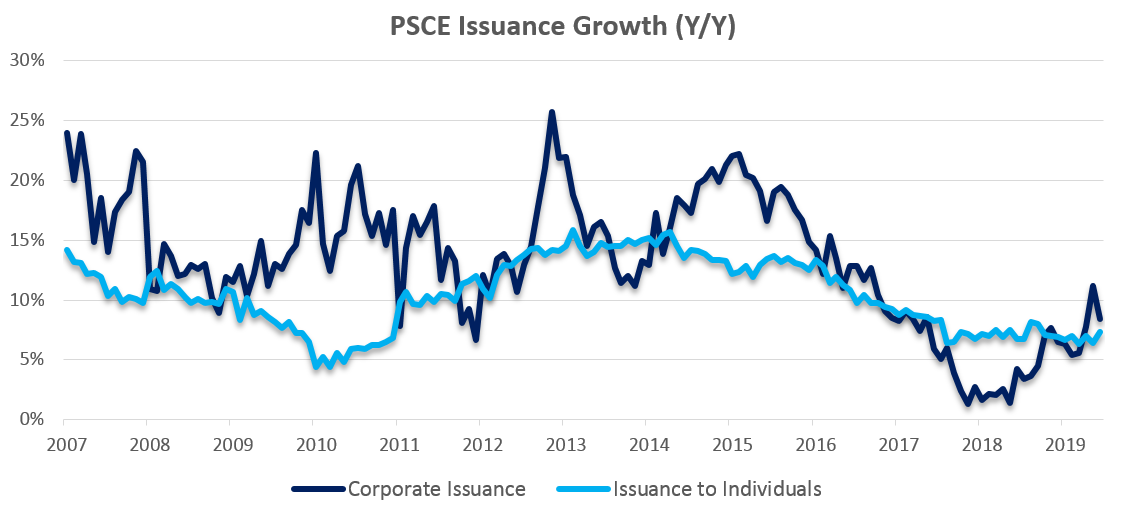

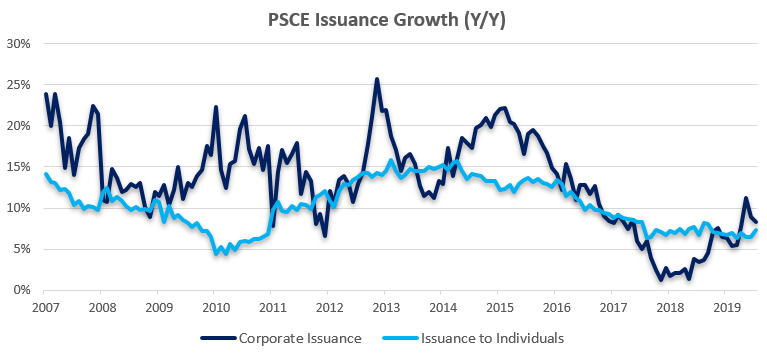

Private sector credit extension growth increased as at the end of July by 7.40% y/y. From a 12-month rolling perspective, credit issuance is up 25.6% from the N$5.5 billion issuance observed at the end of July 2018, with individuals taking up most (58.6%) of the credit extended over the past 12 months. Most of the growth in PSCE for July stemmed from other financial corporations and mortgages extended to individuals.

Corporates increased their demand for overdraft facilities on a year-year basis. The uptake of overdrafts is an indication of lack of liquidity in the fisheries and construction industries to finance working capital in the short-term. Our expectation is for private sector credit extension to remain under pressure as both consumer and business confidence remains low.

As we expected the BoN took the decision to cut the Repo rate by 25 basis points at its August MPC meeting. This should bring heavily indebted consumers and corporates some relief. However, interest rates remain accommodative by historical standards and further rate cuts are unlikely to result in a meaningful increase in the uptake of credit.