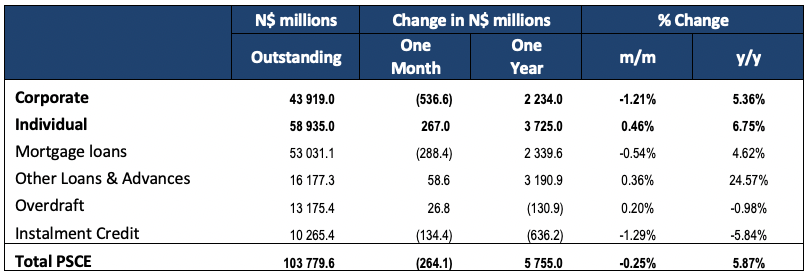

Overall

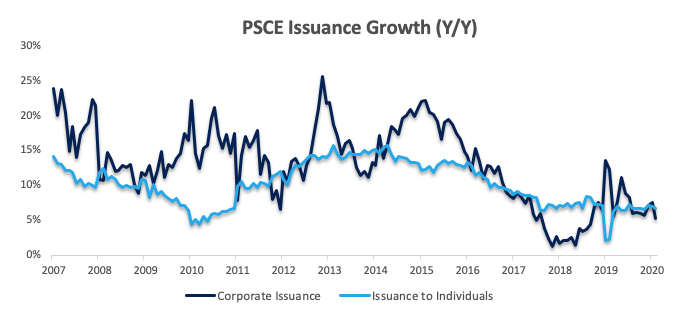

Total credit extended to the private sector (PSCE) decreased by N$130.5 million or 0.13% m/m in March, bringing the cumulative credit outstanding to N$103.6 billion. This is the second consecutive month that we have seen a month-on-month contraction in credit extension. On a year-on-year basis, private sector credit extension grew by 5.79% in March, compared to 5.87% in February. N$2.23 billion worth of credit has been extended to corporates and N$3.73 billion to individuals on a 12-month cumulative basis, while the non-resident private sector has decreased their borrowings by N$204.0 million.

Credit Extension to Individuals

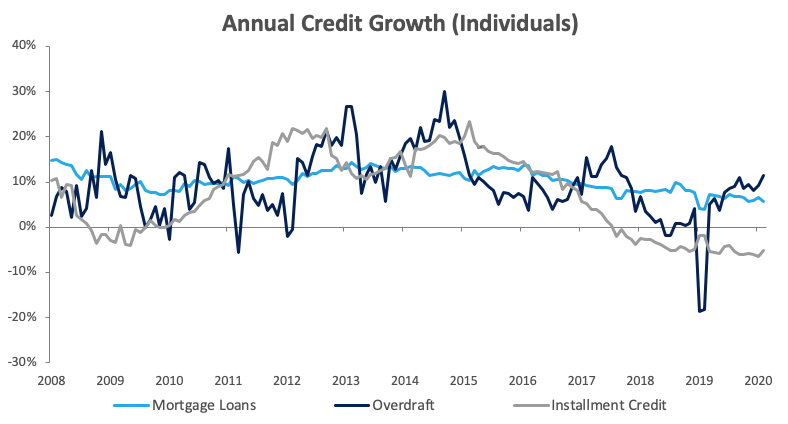

Credit extended to individuals increased by 0.4% m/m and 7.2% y/y in March, versus 0.5% m/m and 6.7% y/y in December. Installment credit remained depressed, contracting by 0.4% m/m and 4.8% y/y. Individuals repaid their overdrafts during the month, resulting in a decline of 1.0% m/m, but an increase of 14.4% y/y. The value of mortgage loans extended to individuals grew by 0.6% m/m and 5.9% y/y. Other loans and advances (or OLA, which is made up of credit card debt, personal and term loans) grew by 0.5% m/m and 27.2% y/y in March. We expected the OLA category to be higher considering that a large number of consumers were ‘panic buying’ staple products (such toilet paper) ahead of the lockdown.

Credit Extension to Corporates

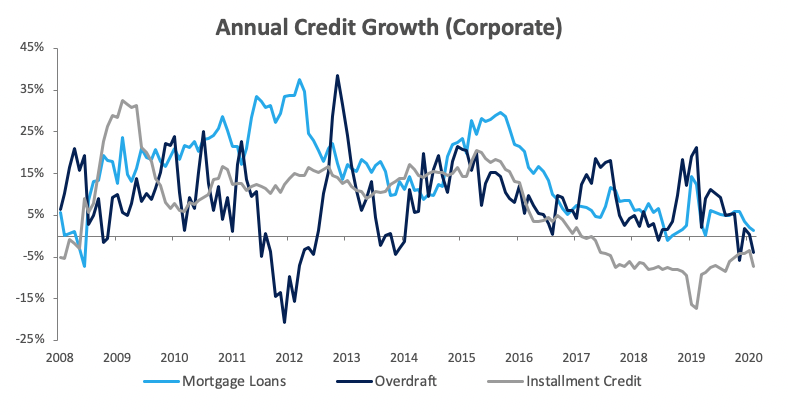

Credit extended to corporates contracted by 0.7% m/m in March after contracting by 1.2% m/m in February. On an annual basis credit extension to corporates increased by 4.6% y/y in March. The month-on-month contraction is mostly caused by businesses paying back overdrafts. Overdraft facilities extended to corporates decreased by 3.9% m/m and 1.1% y/y. Mortgage loans to corporates increased by a moderate 0.2% m/m and 0.3% y/y. Installment credit extended to corporates, which has been contracting since February 2017 on an annual basis, remained depressed, contracting by 0.8% m/m and 7.5% y/y in March.

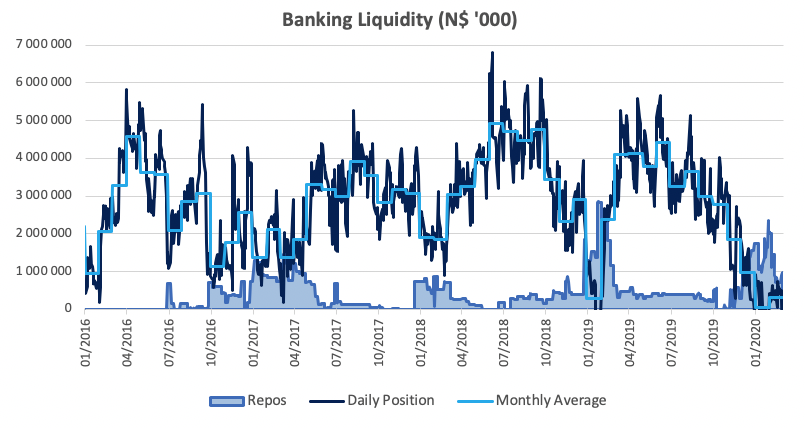

Banking Sector Liquidity

The overall liquidity position of commercial banks decreased by N$71.3 million to reach an average of N$254.5 million. Commercial banks continued to utilise the BoN’s repo facility, as the overall liquidity position remained low. The balance of repo’s outstanding increased from N$1.01 billion at the start of March to N$1.61 billion at the end of the month. The BoN ascribes the low liquidity position to the commercial banks buying liquid assets such as treasury bills, as opposed to keeping cash in the current weak domestic economic environment. It is worth noting that the liquidity position improved substantially in April.

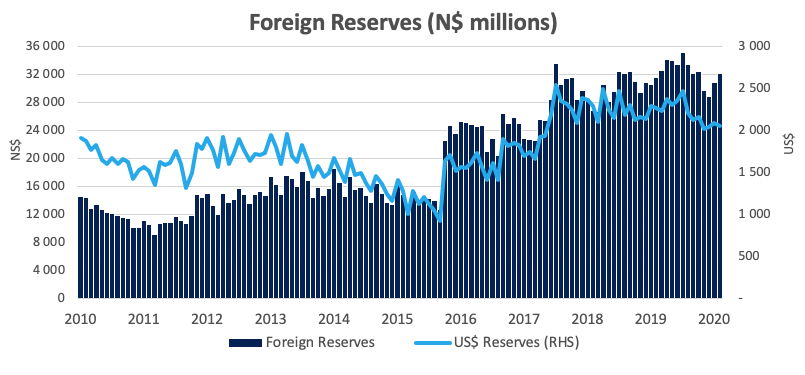

Reserves and Money Supply

Broad money supply rose by N$9.23 billion or 5.9% y/y in March, as per the BoN’s latest monetary statistics release. Foreign reserve balances rose by 2.5% m/m to N$32.97 billion in March. According to the BoN, the increase was supported by a favourable exchange rate during the period.

Outlook

Private sector credit extension remained depressed at the end of March, increasing by only 5.8% y/y, with annualised growth slowing for a second consecutive month. From a rolling 12-month perspective, credit issuance is up 5.9% from the N$5.36 billion issuance observed at the end of March 2019, with individuals taking up most (70.3%) of the credit extended over the past 12 months.

While this hasn’t been the case in March, when the lockdown started, we expect both consumers and businesses to have increased their uptake of short-term debt in April to cover costs while economic activity, and subsequently some individual’s incomes and company revenues, ground to a halt. The second surprise 100 basis point repo rate cut in April should provide these financially stressed businesses and consumers with some relief, but we don’t expect it to push PSCE growth as banks will remain very weary of who they are providing loans to given the current economic situation.