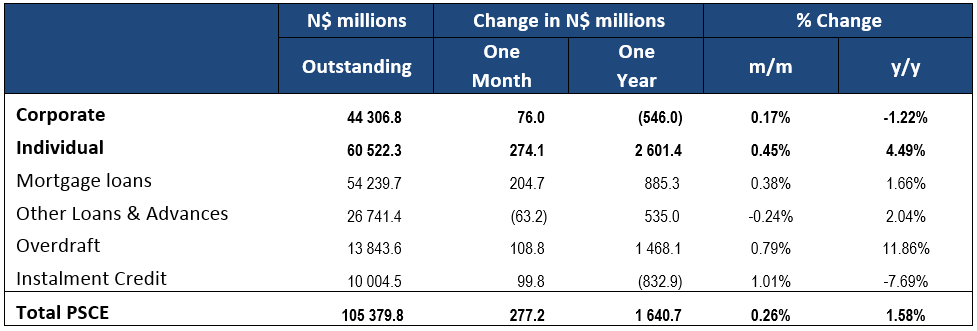

Overall

Private sector credit (PSCE) increased by N$224.1 million or 0.2% m/m in January, bringing the cumulative credit outstanding to N$105.6 billion. On a year-on-year basis, private sector credit grew by 1.50% y/y in January, on par with December’s increase of 1.58% y/y. Cumulative credit extended to the private sector over the last 12-months amounted to N$1.56 billion. Of this cumulative issuance, individuals took up N$1.4 billion worth of debt while N$428.8 million was extended to businesses. The non-resident private sector decreased its borrowings by N$312.9 million.

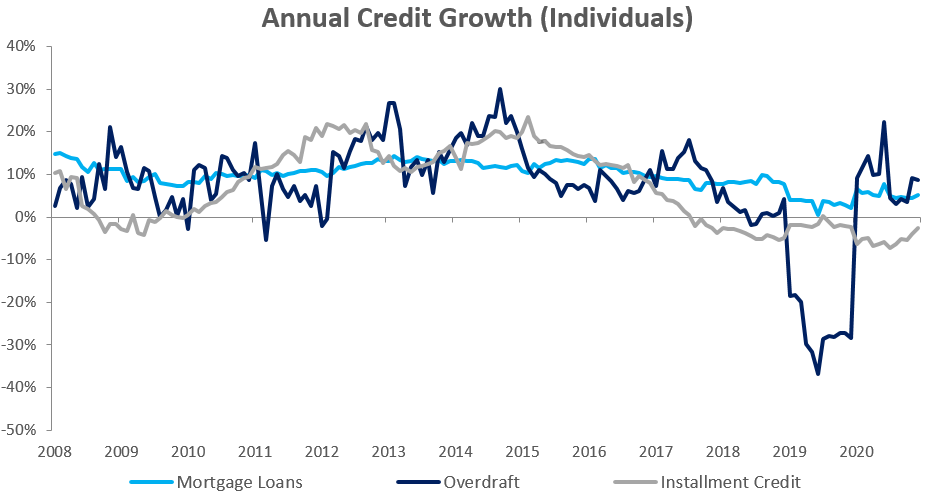

Credit Extension to Individuals

Credit extended to individuals fell by 0.7% m/m, but rose 2.5% y/y in January, growing at almost half the pace than the 4.5% y/y increase recorded in December. All categories recorded a contraction on a monthly basis. Individuals paid back overdrafts during the month, resulting in a 1.7% m/m decrease in this category, but rose 2.3% y/y. Instalment credit declined by 1.3% m/m, while mortgage loans extended to individuals contracted by 0.5% m/m.

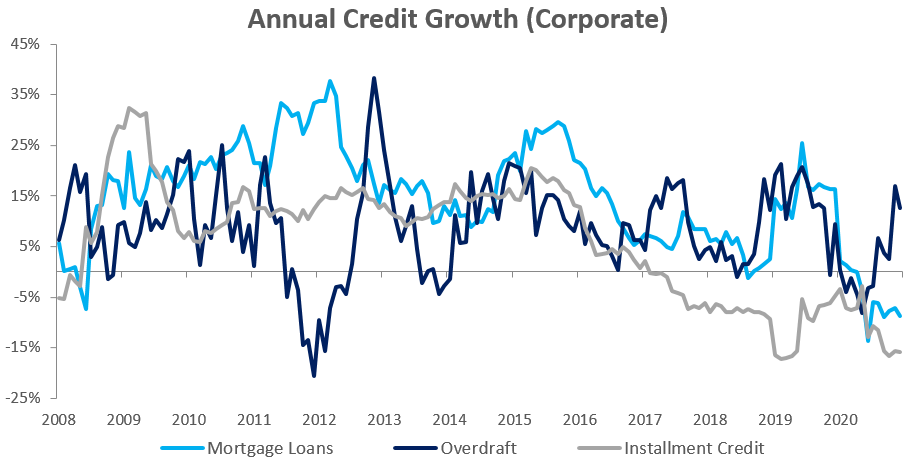

Credit Extension to Corporates

Credit extended to corporates grew by 1.0% y/y in January, after contracting by 1.2% y/y in December. On a month-on-month basis, credit extension to corporates rose 1.3% in January. The month-on-month growth in corporate credit was primarily driven by increased uptake in overdraft facilities which registered growth of 3.7% m/m and 14.2% y/y. The Bank of Namibia indicated that this was mostly due to increased demand for short-term credit facilities to finance their working capital requirements during the month. Demand for instalment credit by corporates remained low, increasing by 1.5% m/m, but contracting 12.8% y/y. Mortgage loans to corporates, grew by 2.7% m/m, but contracted by 3.2% y/y, the lowest annual contraction rate in nine months.

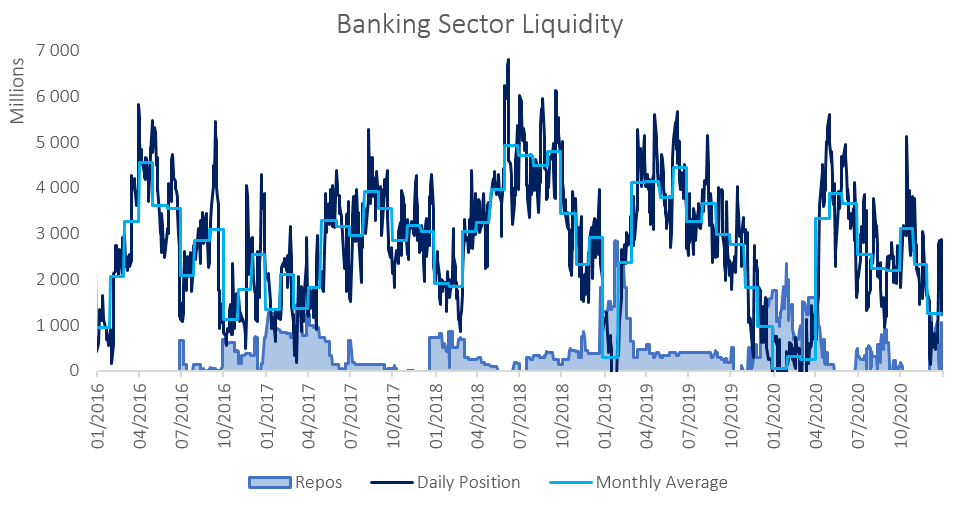

Banking Sector Liquidity

The overall liquidity position of commercial banks deteriorated further during January, declining by N$474.3 million to reach an average of N$775.1 million. According to the Bank of Namibia, the decline is due to periodic corporate tax payments to the government. Commercial banks continued to utilize the BoN’s repo facility in January, with the balance of repo’s outstanding falling from N$1.04 billion at the start of January to N$845.7 million at the end of the month.

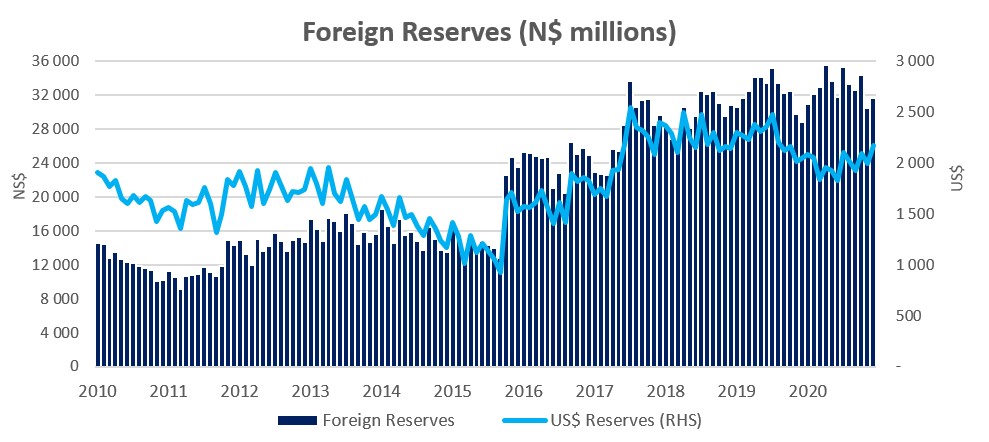

Reserves and Money Supply

Broad money supply rose by N$11.7 billion or 10.2% y/y in January, as per the BoN’s latest monetary statistics release. Foreign reserve balances increased notably in January, up 8.3% m/m or N$2.63 billion to a total of N$34.4 billion. The BoN ascribed the increase to SACU receipts during the month.

Outlook

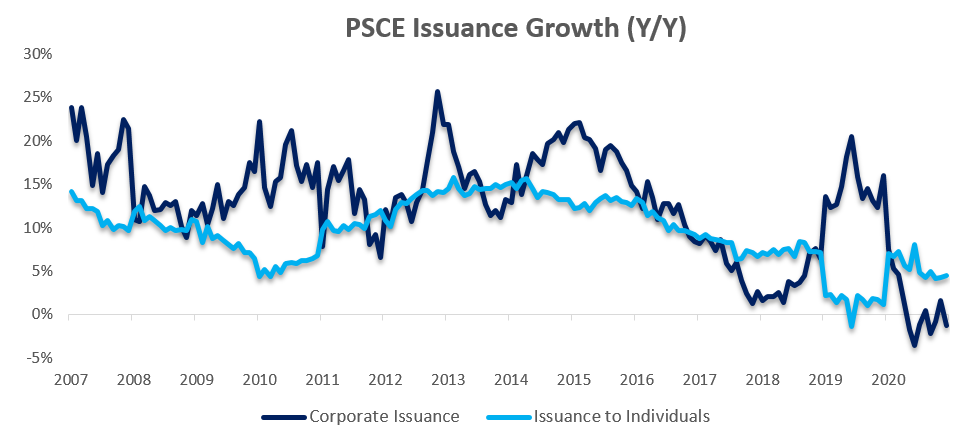

Overall, PSCE growth remains extremely subdued and was very much in line with the growth seen in December on a year-on-year basis, increasing by 1.5%. Rolling 12-month issuance is down 77.0% y/y to N$1.56 billion as at the end of January, with individuals taking up most (92.6%) of the credit extended over the past 12 months.

We expect the Bank of Namibia’s MPC to keep interest rates at its current level for the most part of the year, with the South African FRA curve pricing in the possibility of a 25 bp hike towards the end of the year. Although inflation and other market conditions will likely inform the MPC’s decision. Further rate cuts are likely to have very little, if any, impact on PSCE growth, as rates are already at historically low levels. Significant PSCE growth is likely to only return once economic conditions improve meaningfully.