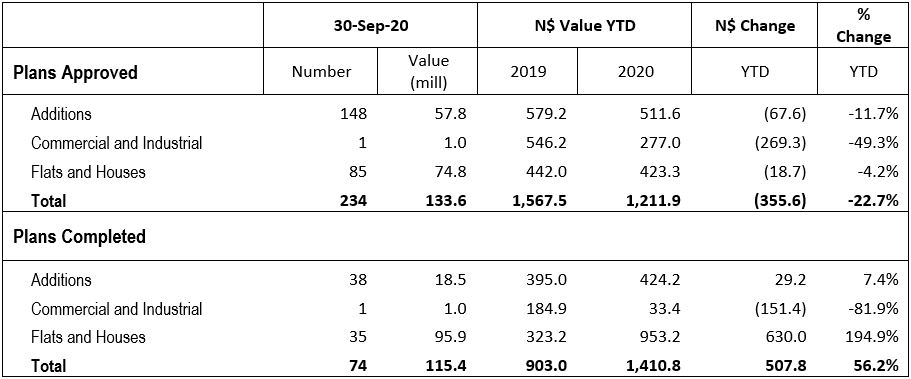

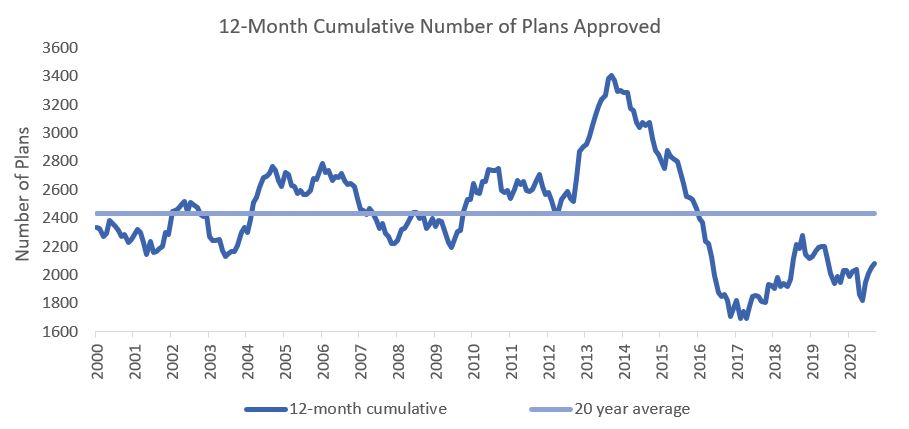

The City of Windhoek approved a total of 234 building plans worth N$133.6 million in September. In value terms approvals rose by 19.3% m/m but fell by 69.1% y/y. A total of 74 completions to the value of N$115.4 million were recorded in September, a decrease of 67.1% y/y in number but a 5.0% y/y increase in value. The year-to-date value of approved building plans reached N$1.21 billion, 22.7% lower than the comparative period a year ago. On a twelve-month cumulative basis, 2,081 building plans were approved worth approximately N$1.64 billion, 10.5% lower in value terms than approvals at the end of September 2019.

The majority of building plan approvals were made up of additions to properties. For the month of September 148 additions were approved worth N$57.8 million, 6.3% less in number and 9.6% less in value than in August. Year-to-date, 1,166 additions have been approved with a value of N$511.6 million, a 4.5% y/y decrease in number and 11.7% y/y decrease in value. 38 additions worth N$18.5 million were completed during the month. In 2020 thus far 839 additions have been completed worth N$424.2 million, an increase of 3.2% y/y in number and 7.4% y/y in value.

New residential units accounted for 85 of the total 234 approvals registered in September, worth N$74.8 million. Year-to-date 391 new residential units have been approved worth N$423.3 million, an increase of 37.2% y/y in number but a decrease of 4.2% y/y in value. 35 new residential units worth N$95.9 million were completed during the month, increases of 84.2% y/y in number and 294.1% y/y in value. Year-to-date 592 residential units have been completed at a value of N$953.2 million, increasing by 163.1% y/y in number and 194.9% y/y in value. On a 12-month cumulative basis the number and value of residential completions are at the highest levels since 2005.

Only 1 new commercial unit, valued at N$1.0 million, was approved in September, bringing the year-to-date number of commercial and industrial approvals to 33, worth a total of N$277.0 million. On a rolling 12-month basis, the number of commercial and industrial approvals have slowed further to 45 worth N$306.4 million as at September, representing an increase of 2.3% y/y in number and a decrease of 45.0% y/y in value.

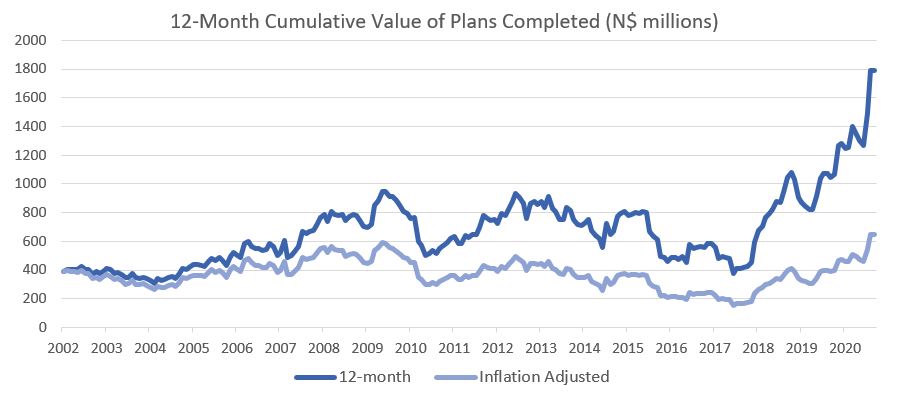

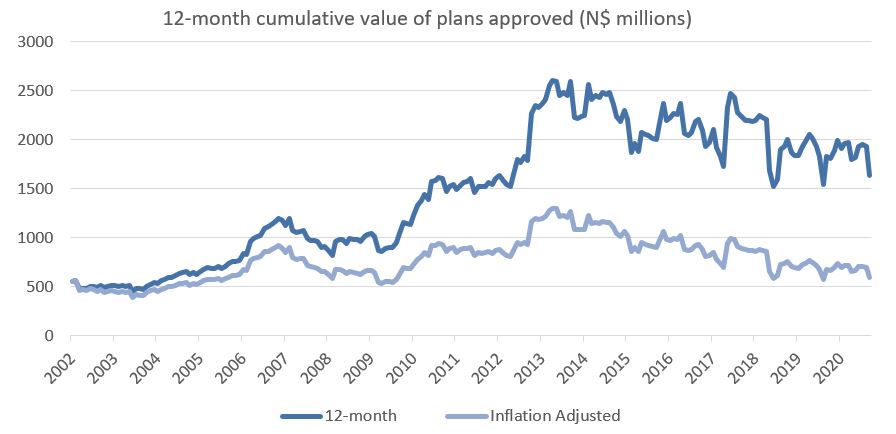

As illustrated in the figure above, the cumulative value of building plans approved continues to trend downward in both nominal and inflation adjusted terms. As approvals is a forward-looking measure of expected construction activity this does not bode well for economic activity in the capital in general. What may be positive however is the ratio of completions to lagged approvals seems to indicate a higher proportion of approved building plans actually being completed. This may partly explain why the approvals data failed to predict the below visible increase in completions. Another possible explanation is that there has been a completions backlog (paperwork backlog) which is now being processed, in which case the below graph does not tell us much about when the actual construction activity took place. We thus caution reading too much into the completions data and continue to look at approvals as a leading economic indicator.