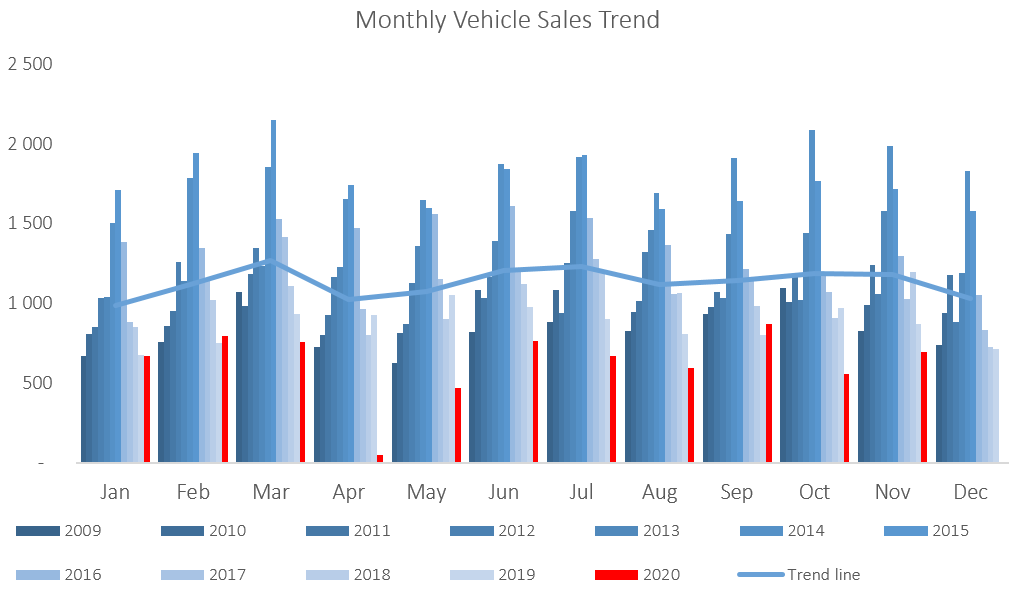

A total of 694 new vehicles were sold in January, which is 6 cars fewer than were sold in December, but represents a 3.3% y/y increase from the 672 new vehicles sold in January 2020. On a twelve-month cumulative basis, a total of 7,636 new vehicles were sold up to the end of January 2021, representing a contraction of 26.5% from the 10,395 new vehicles sold over the same 12 month period a year ago. 2021 is thus off to a slightly better start than January 2020, however, new vehicle sales remain sluggish.

355 new passenger vehicles were sold during January, an increase of 7.6% m/m from the 330 passenger vehicles sold in December, and 21.6% higher y/y from the 292 new passenger vehicles sold in January 2020. On a rolling 12-month basis, new passenger vehicle sales rose 2.0% m/m, but are down 27.2% y/y at the end of January. 12-month cumulative passenger vehicle sales were down 66.7% from the peak in April 2015.

Commercial vehicle sales declined to 339 units in January, representing a contraction of 8.4% m/m and 10.8% y/y. During the month 301 light commercial vehicles, 9 medium commercial vehicles, and 29 heavy commercial vehicles were sold. On a year-on-year basis, light commercial sales fell by 10.1% y/y, medium commercial vehicle dropped by 35.7% y/y, and heavy and extra heavy vehicle sales declined by 6.5% y/y. On a twelve-month cumulative basis, light commercial vehicle sales contracted by 25.3% y/y, medium commercial vehicles declined by 37.2% y/y and heavy commercial vehicle sales fell by 27.3% y/y.

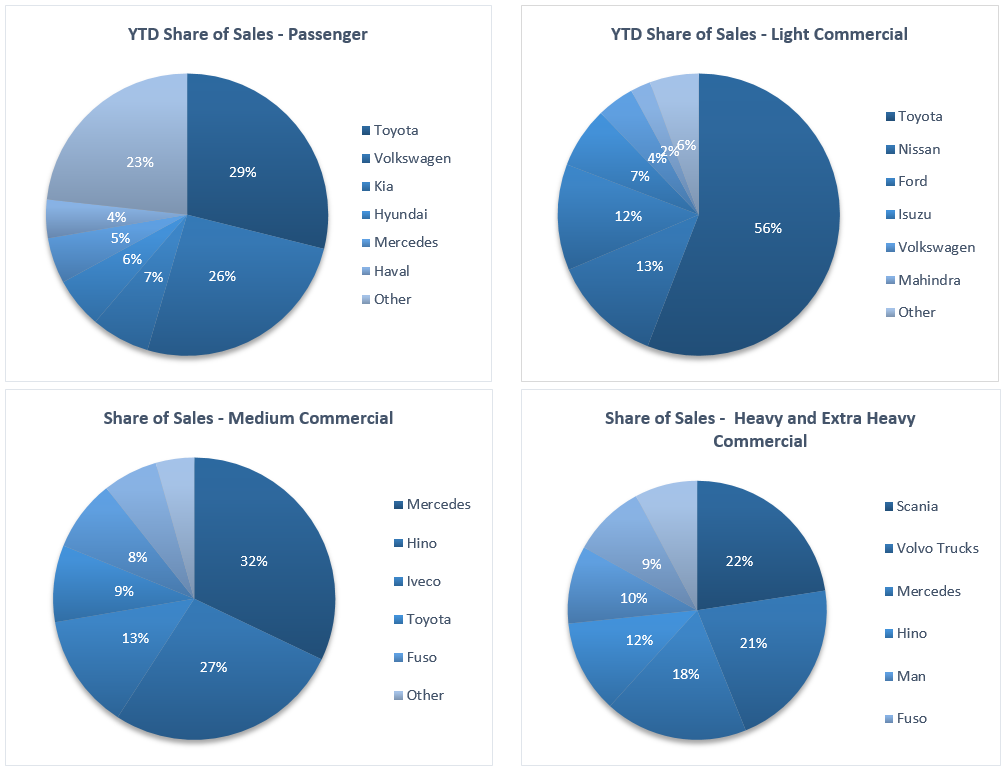

Volkswagen started the year off on a strong foot with a 41.4% market share of new passenger vehicles sold, followed by Toyota with a 25.1% market share. They were followed by Kia and Mercedes who each had a 6.5% market share, while the rest of the passenger vehicle market was shared by several other competitors.

Toyota meanwhile started the year off with a solid grip on the light commercial vehicle market with a 55.1% market share, with Nissan in second place with a 13.3% market share. Ford and Volkswagen claimed 11.3% and 5.0% of the number of new light commercial vehicles sold during the month, respectively. Iveco led the medium commercial vehicle category with 33.3% of sales, while Scania was number one in the heavy and extra-heavy commercial vehicle segment with 27.6% of the market share during the month.

The Bottom Line

New passenger vehicle sales started the year off stronger than in 2020, with passenger vehicle sales increasing by 21.6% y/y. This uptick in sales did not pass through to commercial vehicle sales which had a poor start and contracted by 10.8% y/y. While new vehicle sales in January were higher than the first month of the past two years, it remains considerably lower than the numbers recorded between 2012 and 2016. The likelihood of a recovery in 2021 to the levels witnessed during that period seems very low currently. We expect businesses to hold on to their current fleets for as long as possible and for consumers to mostly stick to the pre-owned market, seeing that there are very few economic growth prospects at present.