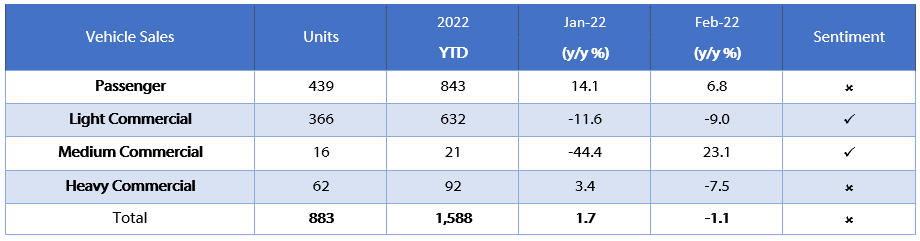

A total of 905 new vehicles were sold in April, a 14.1% m/m contraction but an increase of 19.9% y/y from the 755 vehicles sold in April 2022. Year-to-date 3,550 new vehicles have been sold, of which 1,841 were passenger vehicles, 1,491 light commercial vehicles, and 218 medium and heavy commercial vehicles. By comparison, the first four months of 2021 saw 3,260 new vehicles sold. On a twelve-month cumulative basis, a total of 9,718 new vehicles were sold at the end of April, representing a 13.0% y/y increase from the 8,602 sold over the comparable period a year ago.

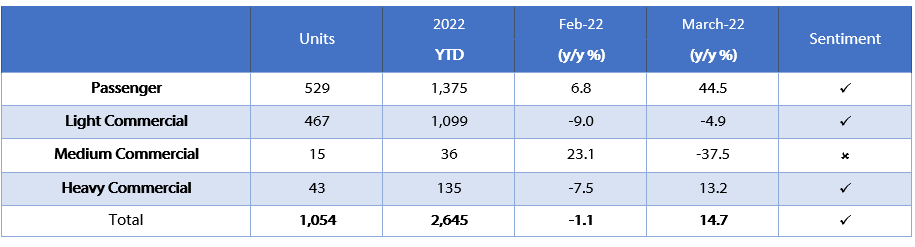

466 new passenger vehicles were sold during April, 11.9% lower than the 529 passenger vehicles sold in March, but an increase of 30.2% from the 358 sold in April 2021. Year-to-date, passenger vehicle sales rose to 1,841, an increase of 23.6% than during the same period last year. On a rolling 12-month basis, passenger vehicle sales rose to 4,836, 29.2% higher than over the same period in 2021.

New commercial vehicle sales displayed a similar trend, declining month-on-month, but are up from the same month last year. 439 new commercial vehicles were sold in April, representing a month-on-month contraction of 16.4%, but a year-on-year increase of 10.6% y/y. 392 Light commercial vehicles, 17 medium commercial vehicles, and 30 heavy and extra heavy commercial vehicles were sold during the month. Light- and heavy commercial vehicle sales fell by 16.1% m/m and 30.2% m/m, respectively, while medium commercial vehicle sales rose by 13.3% m/m. On a twelve-month cumulative basis, light commercial vehicle sales are down 2.0% y/y, while medium commercial vehicle sales rose by 6.7% y/y, and heavy commercial vehicles climbed by 21.1% y/y.

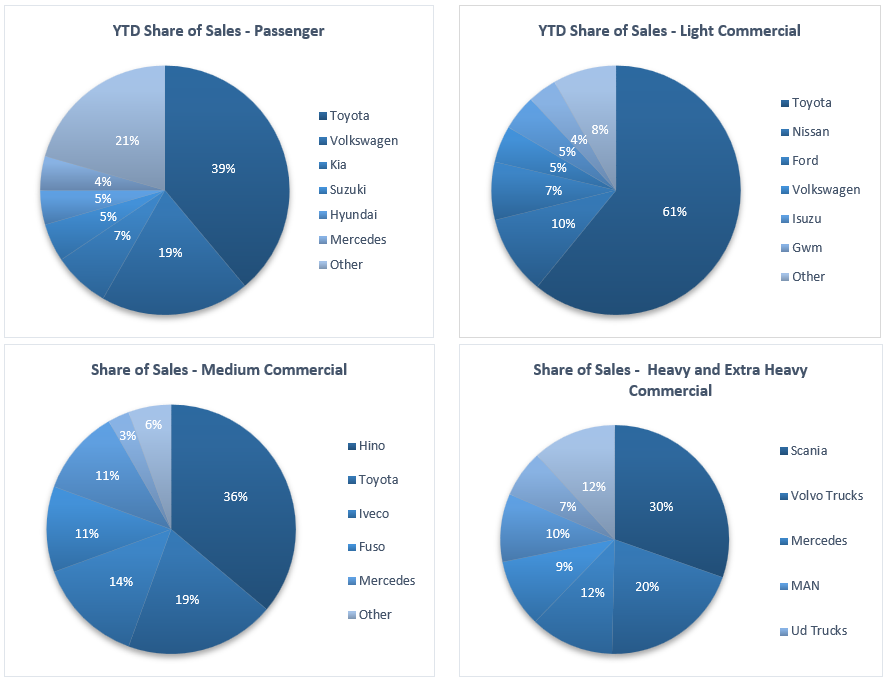

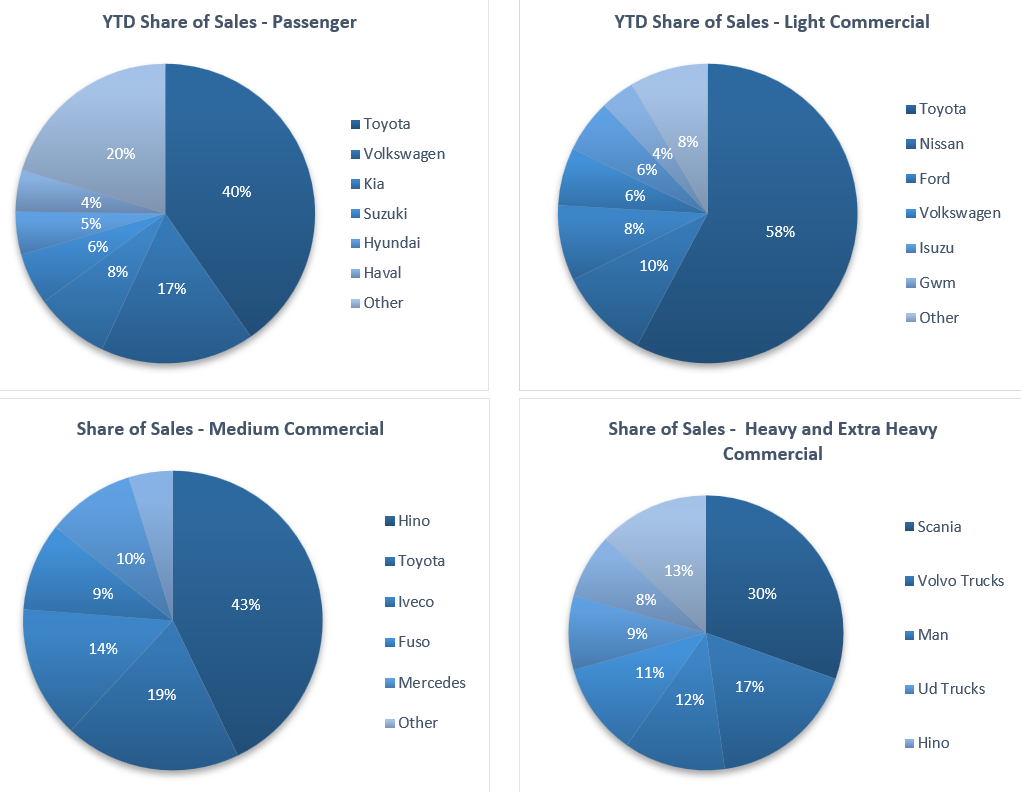

Toyota continues to lead the new passenger vehicle sales segment with 36.8% of the segment sales year-to-date, followed by Volkswagen with 20.4% of the market share. The two top brands maintained their large gap over the rest of the market with Kia and Suzuki following with 7.9% and 6.1% of the market, respectively, leaving the remaining 28.8% of the market to other brands.

On a year-to-date basis, Toyota maintained its dominance in the light commercial vehicle space with a 60.6% market share, followed by Nissan with 10.7% of the market. Hino leads the medium commercial vehicle segment with 37.7% of sales year-to-date. Scania remained number one in the heavy and extra-heavy commercial vehicle segment with 27.3% of the market share year-to-date.

The Bottom Line

We noted in last month’s report that March new vehicle sales generally have a seasonal effect of being slightly higher than the surrounding months, and that we expect to see April’s new vehicle sales to return to the levels witnessed in the last 18 months. This has now transpired with new vehicle sales being 14.1% lower than last month. New vehicle sales were however 19.9% higher than during the same month a year ago and 13.5% higher than the average monthly sales figure over the past twelve months. On a 12-month cumulative basis, new passenger vehicle sales continued to increase, rising for the 17th consecutive month. New commercial vehicle sales however continue to hover around the 4,800 level where it has been trending for the past year.