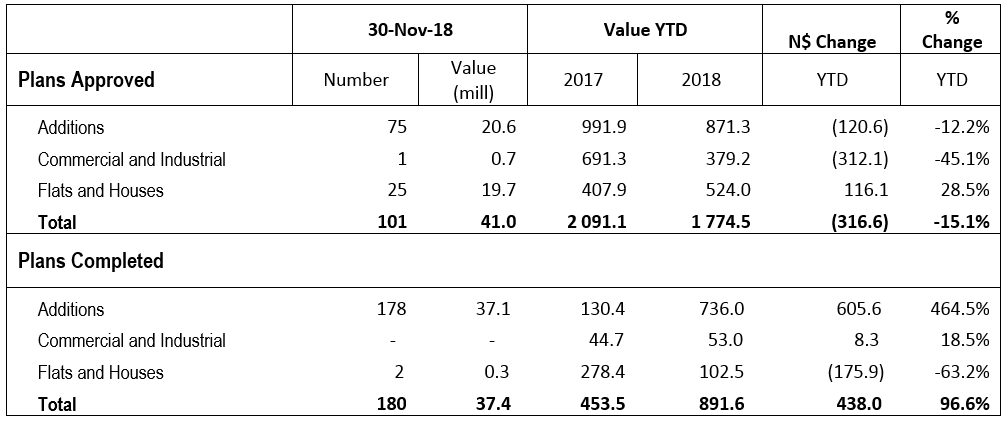

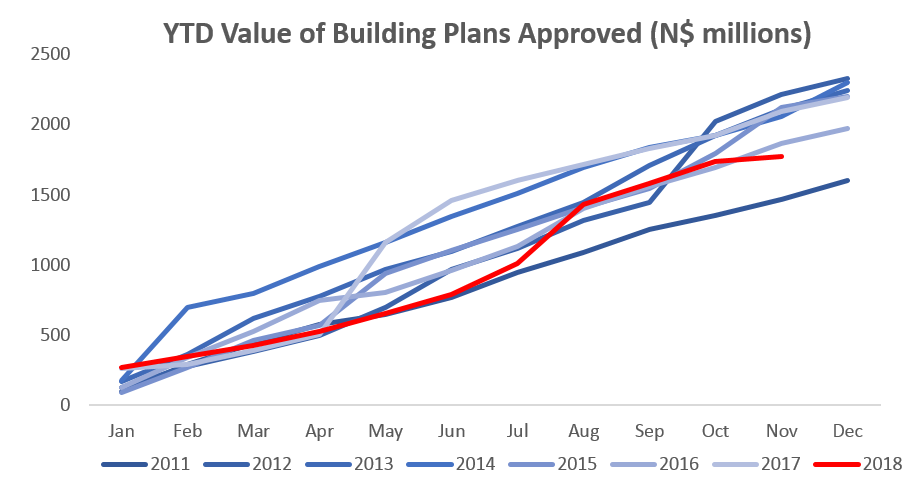

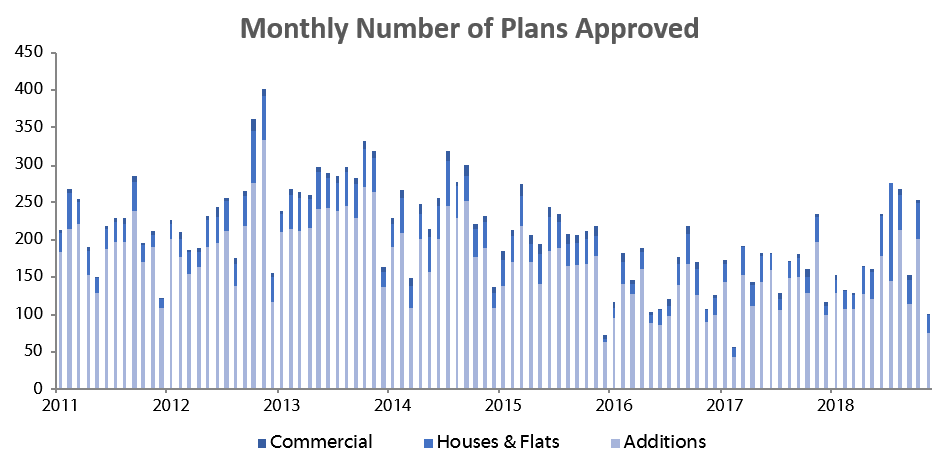

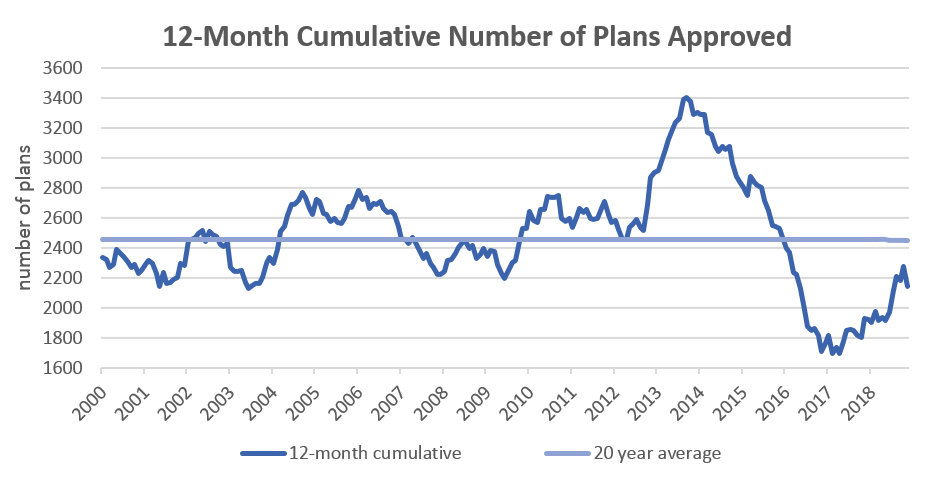

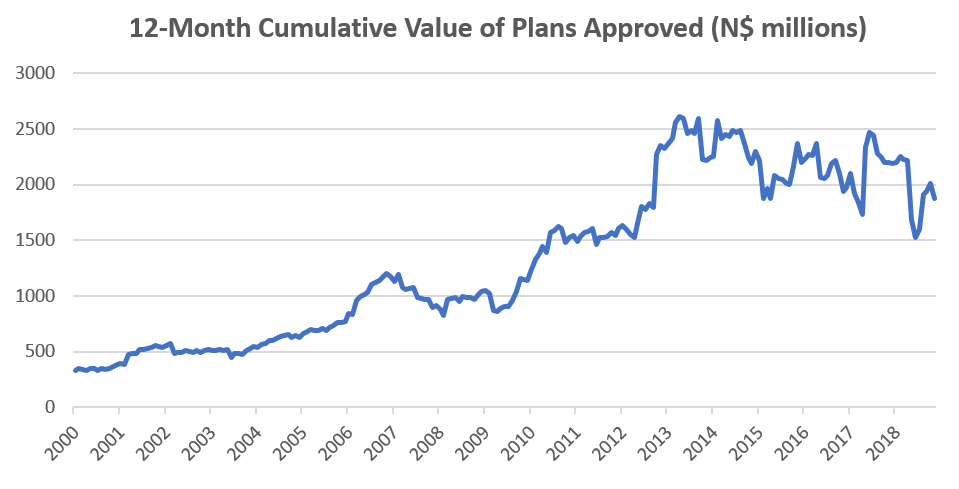

A total of 101 building plans were approved by the City of Windhoek in November which represents a 60.1% m/m decrease from the 253 building plans approved in October. In value terms, approvals fell by N$114.8 million to N$41.0 million, representing a decline of 73.7% m/m and 76.1% y/y. The number of completions for the month of November stood at 180, valued at N$37.4 million. On a year-to-date basis, 2,027 plans have been approved, 220 more than over the same period last year. The year-to-date value of approved building plans currently stands at N$1.77 billion, which is 15.1% lower than during the corresponding period in 2017. On a twelve-month cumulative basis, 2,143 building plans were approved, an increase of 10.9% y/y, worth approximately N$1.87 billion, a decrease of 14.7% in value terms over the prior 12-month period.

The largest portion of building plan approvals in November were made up of additions to properties, from both a number and value perspective. 75 additions to properties were approved with a value of N$20.6 million, 82.2% less in value terms than in November 2017. Year-to-date 1,518 additions to properties have been approved with a value of N$871.3 million, declining 12.2% y/y in terms of value.

New residential units accounted for 25 of the total 101 approvals registered in November, a m/m decrease of 46.8% compared to the 47 residential units approved in October. In value terms, N$19.7 million worth of residential units were approved in November, 55.2% less than the N$44.1 million worth of residential approvals in October. Year-to-date 469 residential units have been approved, 192 more than in the corresponding period in 2017. In monetary terms, N$524 million worth of new residential plans have been approved year-to-date, an increase of 28.5% when compared to the corresponding period last year.

Only 1 new commercial unit valued at N$700,000 was approved in November, bringing the year-to-date number of approvals to 40, worth a total of N$379.2 million. On a rolling 12-month perspective the number of commercial and industrial approvals have slowed to 44 units worth N$385.2 million as at November, compared to the 49 approved units worth N$698.1 million over the corresponding period a year ago.

Building plan approvals took a sharp downturn in November, in terms of both number of approvals and value. Recent private sector credit extension data shows that growth in short-term credit such as overdrafts has been stronger than growth in long-term credit such as mortgage loans for both consumers and businesses. This is an indication that corporates are borrowing simply to stay afloat and are not borrowing to invest in expansionary projects, as is evident in the commercial building plan approval figures. Building plan approvals are a leading indicator for economic activity, which makes November’s low figures somewhat worrisome as it implies that businesses are not investing freely and that the economy is likely to remain under pressure in the short term.