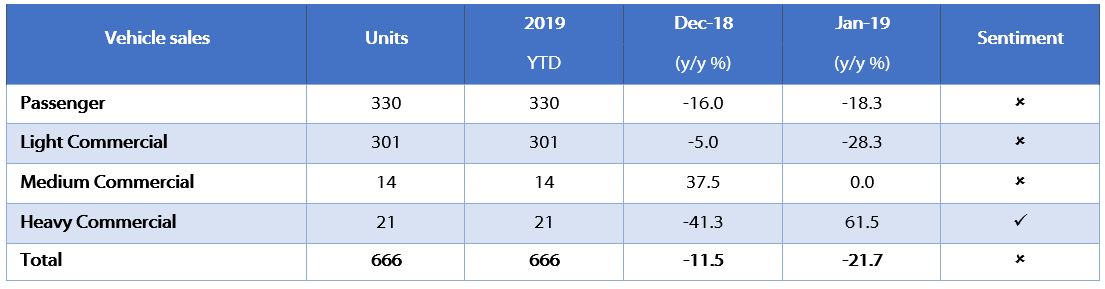

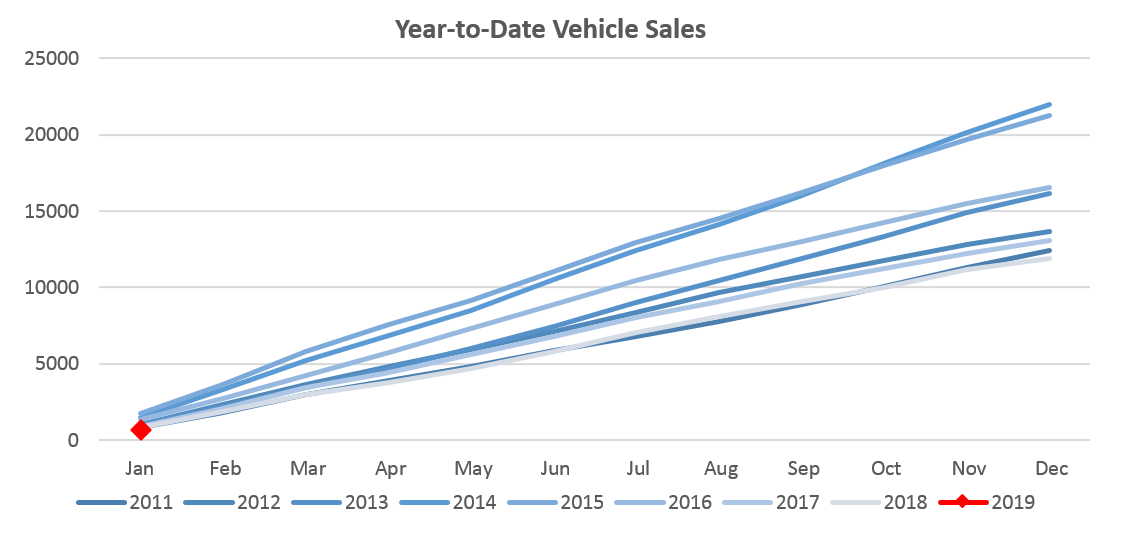

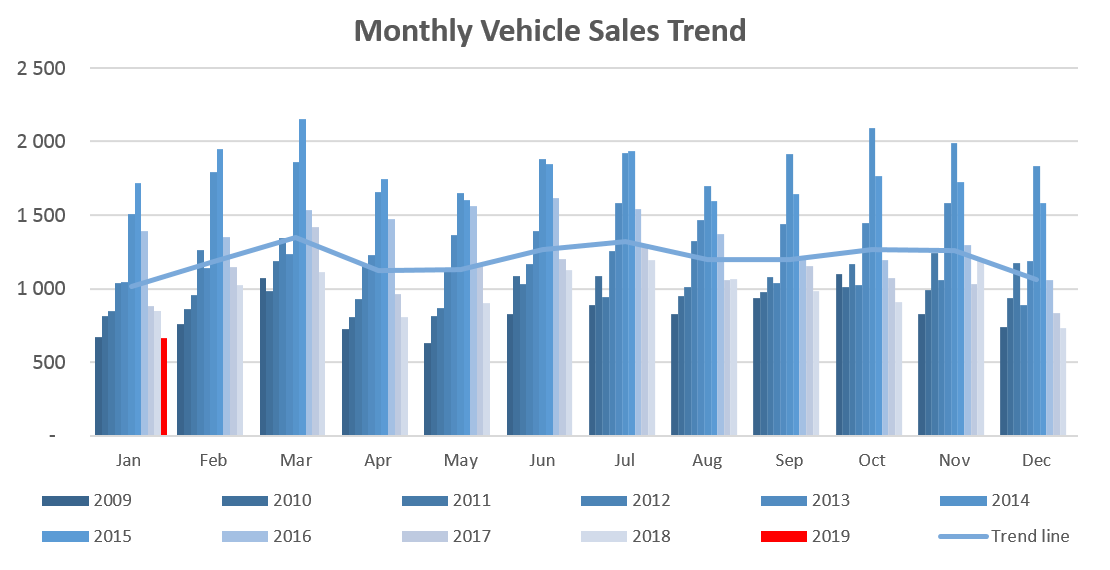

A total of 666 new vehicles were sold in January, which represents an 8.8% m/m decrease from the 730 vehicles sold in December, and a drop of 21.7% from the 851 new vehicles sold in January 2018. On a twelve-month cumulative basis, a total of 11,721 new vehicles were sold at January 2019 representing a contraction of 9.9% from the 13,007 sold over the same period a year ago. 2019 is thus off to a sluggish start as illustrated by the lowest monthly sales number since May 2009.

330 new passenger vehicles were sold during January, 6.5% higher than the 310 passenger vehicle sales sold in December. From a year-on-year perspective however, January 2019 new passenger vehicle sales were 18.3% lower than the 404 sold a year ago. Passenger vehicle sales have been impacted by amendments to the Credit Act that requires tighter credit conditions, as well as by reduced government expenditure and depressed consumer confidence in the current economic climate.

Commercial vehicle sales declined to 336 units in January, representing a contraction of 20.0% m/m and 24.8% y/y. During the month 301 light commercial vehicles, 14 medium commercial vehicles, and 21 heavy commercial vehicles were sold. On an annual basis, light commercial sales have dropped by 21.2%, medium commercial sales rose by 27.3%, and heavy and extra heavy sales have declined by 22.2%. On a twelve-month cumulative basis, light commercial vehicle sales fell 11.2% y/y, while medium commercial vehicle sales rose 11.4% y/y, and heavy commercial vehicle sales dropped 7.3% y/y.

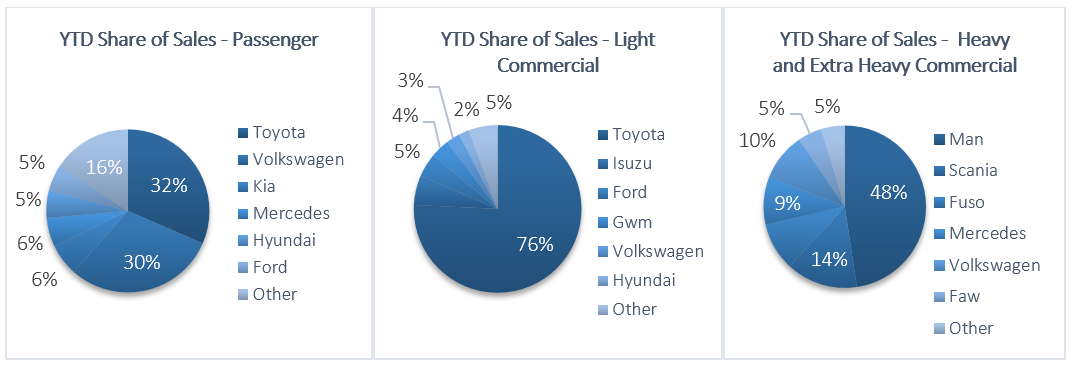

Toyota started the year off with a 31.5% market share of new passenger vehicles sold, followed closely by Volkswagen with a 30.0% market share. They were followed by Kia and Mercedes with 6.4% and 5.8% of the market respectively, while the rest of the passenger vehicle market was shared by several other competitors.

Toyota also started the year off with a firm grip on the light commercial vehicle market with a 75.7% market share, with Isuzu in second place with a 5.6% share. Ford and GWM claimed 4.7% and 3.7% of the number of new light commercial vehicles sold for the year, respectively. Hino and Mercedes jointly lead the medium commercial vehicle category, each with 28.6% of the sales, while Man was number one in the heavy and extra-heavy commercial vehicle segment with 47.6% of the market share in January.

The Bottom Line

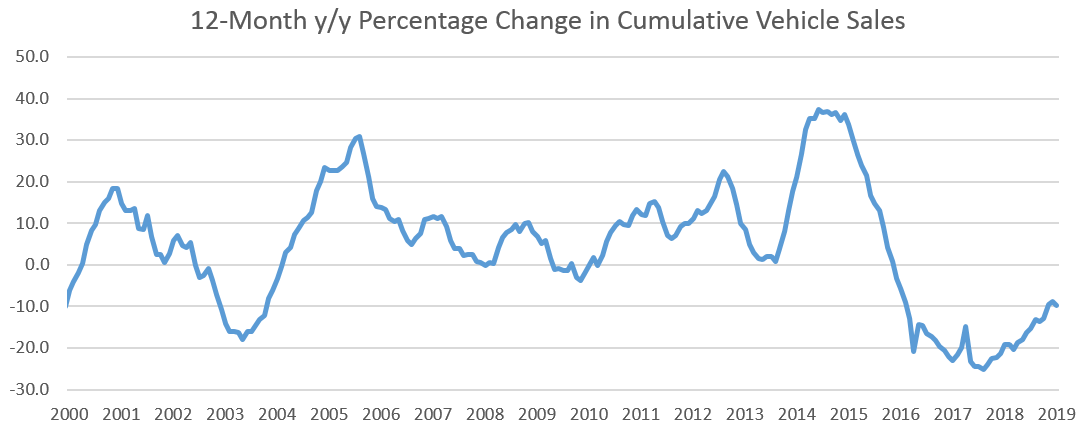

12-month cumulative new vehicle sales have been declining since December 2015, amounting to 11,721 at the end of January, a decline of 48.3% from the peak of 22,664 cumulative new vehicle sales recorded in April 2015. While January new vehicle sales have historically been low when compared to most other months, 2019’s January figure was the lowest since 2006. The prospects for new vehicle sales remain dim in the short- to medium-term as government remains committed to fiscal consolidation and the economy remains in a recession, putting pressure on demand and investment.