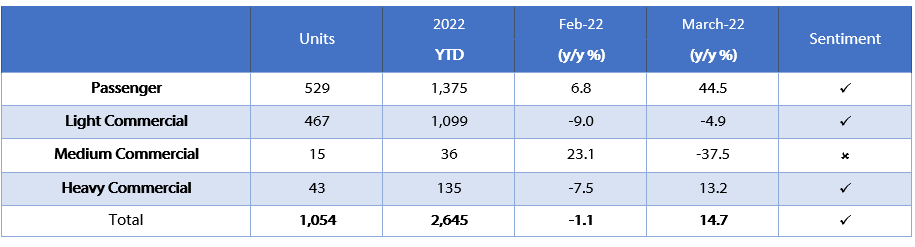

A total of 767 new vehicles were sold in May, down 15.25% m/m from the 905 vehicles sold in April 2022 and down 2.9% y/y from the 790 vehicles sold in May 2021. Year-to-date 4,317 new vehicles have been sold, of which 2,243 were passenger vehicles, 1,800 light commercial vehicles, and 272 medium and heavy commercial vehicles. In comparison, 4,050 new vehicles were sold during the first 5 months of 2021. On a twelve-month cumulative basis, a total of 9,695 new vehicles were sold at the end of May, representing a 9.0% y/y increase from the 8,912 new vehicles sold over the comparable period a year ago.

402 new passenger vehicles were sold in May, the lowest monthly sales figure so far this year, and down 13.7% from the 466 passenger vehicles sold in April, but up 12.3% when compared to the 358 sold in May 2021. Year-to-date, 2,243 new passenger vehicles have been sold, an increase of 21.4% from the 1,847 new passenger vehicles sold over the same period in 2021. On a twelve-month cumulative basis, a total of 4,880 new passenger vehicles were sold, up 26.0% y/y when compared the 3,872 passenger vehicles sold over the comparable period last year. Despite being a somewhat weaker month for new passenger vehicle sales, May’s sales figure is not far off the average monthly sales figure for the past 12 months.

365 new commercial vehicles were sold in May, down 16.9% m/m from the 439 commercial vehicles sold in April and down 15.9% y/y when compared to the 432 commercial vehicles sold in May 2021. Light commercial vehicle sales continue to make up the bulk of the new commercial vehicle sales with 309 sold in May, followed by 47 heavy and extra heavy commercial vehicles and 9 medium commercial vehicles sold during the month. Light- and medium commercial vehicle sales fell by 21.2% m/m and 47.1% m/m, respectively, while heavy and extra heavy commercial vehicle sales rose by 56.7% m/m. On a twelve-month cumulative basis, light commercial vehicle sales fell by 6.5% y/y, while medium commercial vehicle and heavy and extra heavy commercial vehicle sales rose by 0.5% y/y and 12.4% y/y, respectively.

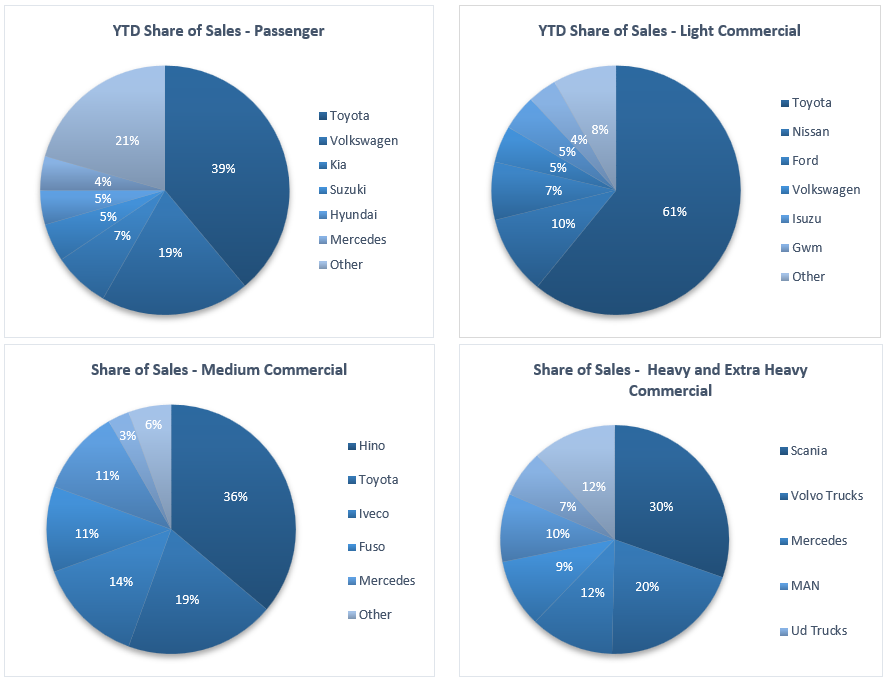

Toyota retained its lead in the new passenger vehicle sales segment with 33.0% of the segment sales year-to-date, despite the significant decline in its monthly vehicles sales figure in May following the closure of its plant in KwaZulu-Natal due to flood damage. Volkswagen, with a 19.8% of the passenger vehicle market share, was second, followed by Kia and Suzuki with 8.8% and 7.8% of the market, respectively, leaving the remaining 30.6% of the market share to other brands.

On a year-to-date basis, Toyota maintained its dominance in the light commercial vehicle space with a 54.9% market share despite also recoding significantly lower sales in this segment, followed by Nissan with 12.1% of the market. Hino continues to lead the medium commercial vehicle segment with 33.9% of sales year-to-date. Scania retains its position as the leader in the heavy and extra-heavy commercial vehicle segment with 31.6% of the market share year-to-date, an increase from last month.

12-month cumulative new passenger vehicle sales continue to increase, rising for the 18th consecutive month, while 12-month cumulative commercial vehicle sales continue to hover around the 4,800 level, where it has been for the last 14 months. While the month of May has historically been a relatively weaker month for new vehicle sales in Namibia, this year’s decline in May was to an extent driven by the closure of the Toyota plant in KwaZulu-Natal, as the manufacturer recorded an over 50% decline in sales in all segments when compared to its monthly average over the past 12 months. Overall year-to-date new vehicle sales are still roughly in line with those of 2021.