Overall

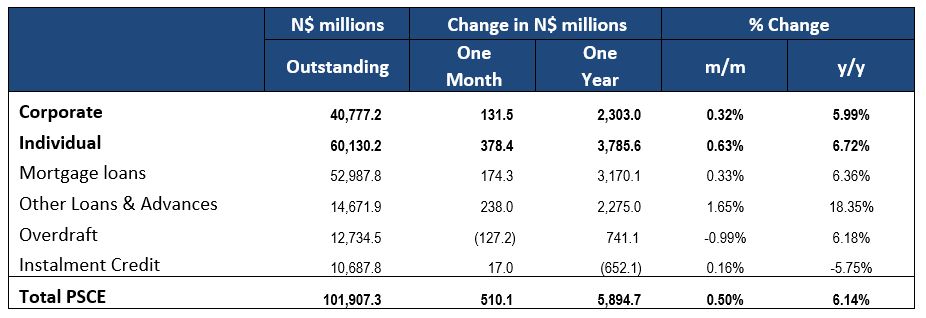

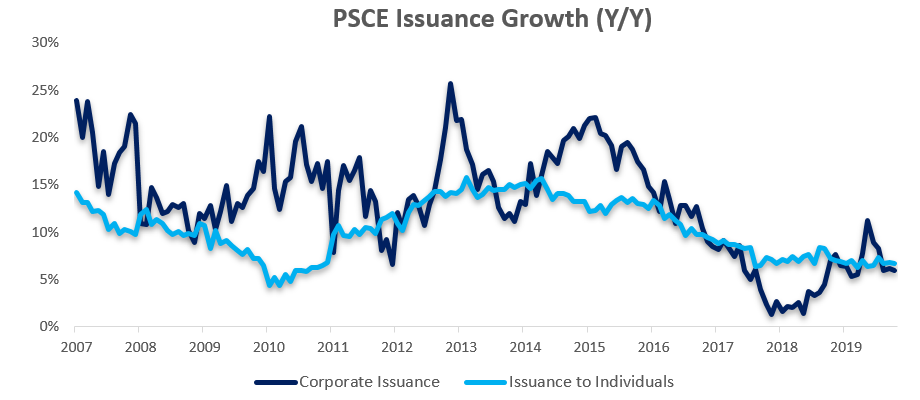

Private sector credit (PSCE) increased by N$1.24 billion or 1.2% m/m in December, bringing the cumulative credit outstanding at the end of 2019 to N$103.7 billion. On a year-on-year basis, private sector credit increased by 6.9% in December, increasing at a quicker rate than the 5.9% recorded in November. From a rolling 12-month basis, N$6.7 billion worth of credit was extended to the private sector, compared to the previous year, the rolling 12-month issuance is down 1.4% from the N$6.8 billion issuance observed by the end of December 2018. Of this cumulative issuance, individuals took up the lion’s share of credit, amassing N$4.1 billion worth of debt while N$2.8 billion was extended to businesses. The non-resident private sector decreased their borrowings by N$170 million.

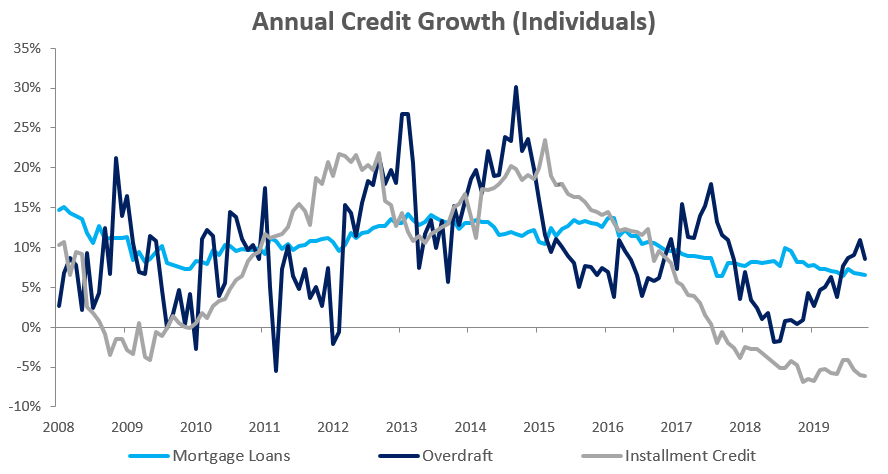

Credit Extension to Individuals

Credit extended to individuals increased by 7.2% y/y in December, compared to 6.6% y/y recorded in November. On a monthly basis, household credit increased by 1.2%, double the pace of the 0.6% growth registered in November. Most of this growth stemmed from an increase in ‘Other loans and advances’ of 5.8% m/m and 32.0% y/y in December. This relatively quick pace can likely be explained by consumers making use of credit cards and payday loans to purchase gifts and pay for travel expenses over the holiday period. Installment credit continued to contract, by 0.1% m/m and 6.0% y/y. Mortgage loans extended to individuals grew by 0.7% m/m and 5.9% y/y, compared to 0.2% m/m and 5.7% y/y in November.

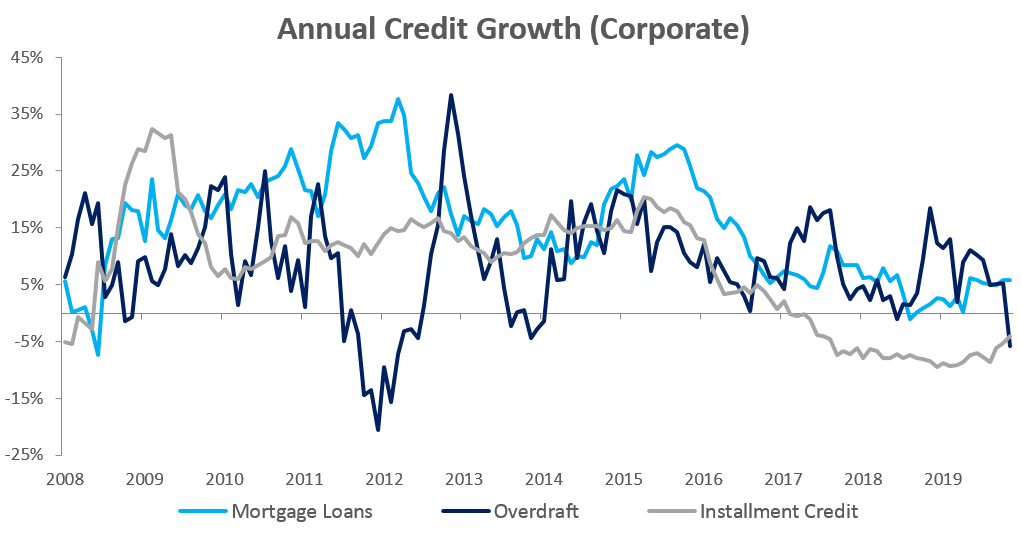

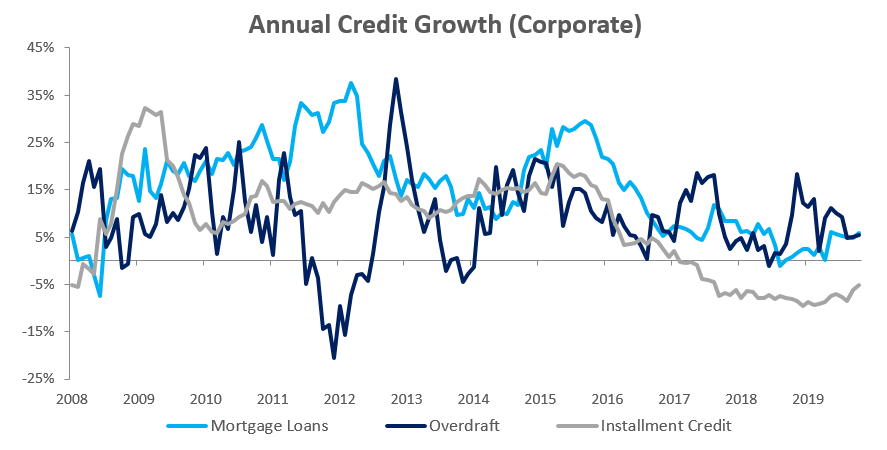

Credit Extension to Corporates

Credit extension to corporates grew by 1.1% m/m and 7.1% y/y in December, following a slow increase of 0.4% m/m and 5.7% in November. On a rolling 12-month basis N$2.76 billion was extended to corporates in 2019, an increase of 17.3% y/y from the N$2.35 billion that was extended to corporates in 2018. Installment credit extended to corporates, which has been contracting on an annual basis since February 2017 remained depressed, contracting by 0.9% m/m and 4.1% y/y in December. Leasing transactions to corporations grew by 1.1 m/m, but declined by 31.7% y/y. Overdraft facilities extended to corporates increased by 3.0% m/m and 1.9% y/y.

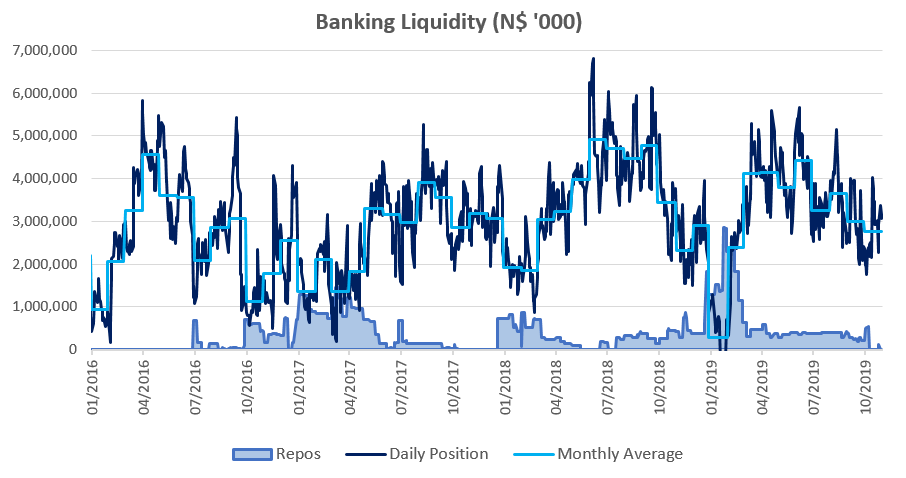

Banking Sector Liquidity

The overall liquidity position of commercial banks deteriorated significantly during December, declining by N$858.3 million to reach an average of N$982.7 million. Bank of Namibia attributed the decline in liquidity to corporate tax payments during December as well as a high uptake of treasury bills and other liquid assets by commercial banks. The relatively low liquidity position has prompted commercial banks to utilize the BoN’s repo facility, with the balance of repo’s outstanding increasing from N$284.7 million at the start of December to N$1.75 billion at the end of the month.

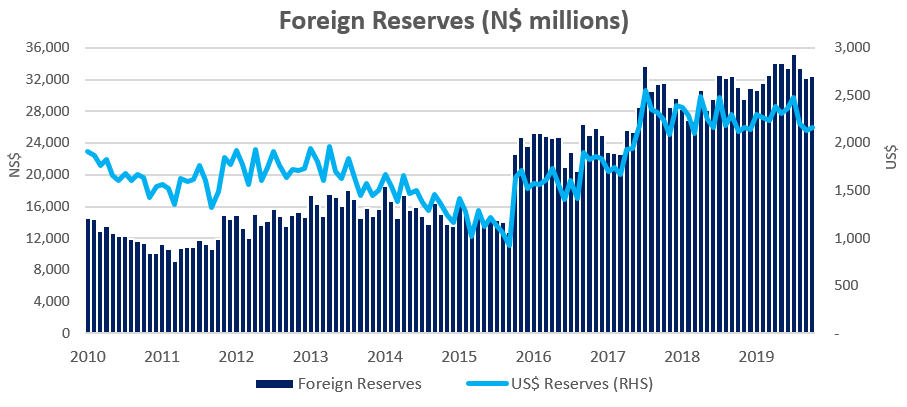

Reserves and Money Supply

As per the BoN’s latest money statistics release, broad money supply rose by N$11.0 billion or 10.5% y/y in December, following a 10.6% y/y increase in November. Foreign reserve balances fell by 3.0% m/m to N$28.8 billion in December. The BoN again stated that the decline was due to the net purchases of South African Rands by commercial banks for import payments coupled with increasing government foreign payments during the month under review.

Outlook

Private sector credit growth figures for 2019 remained largely in the same 6-7% y/y range as in 2018. The rolling 12-month issuance of N$6.7 billion is however down 1.4% from the N$6.8 billion issuance recorded at the end of 2018.

The SARB’s MPC surprised markets with a unanimous decision to cut the repo rate by 25-basis points to 6.25% at its meeting in January. We expect the BoN’s MPC to follow the SARB’s decision at its next meeting later in February, as Namibian inflation figures are trending at very low levels and economic growth is stagnating. Policy changes (and policy certainty) to attract foreign investment will at this moment likely be more effective to revive economic activity than more accommodative monetary policy, although a 25-basis point rate cut should provide some relief to heavily indebted consumers.