Overall

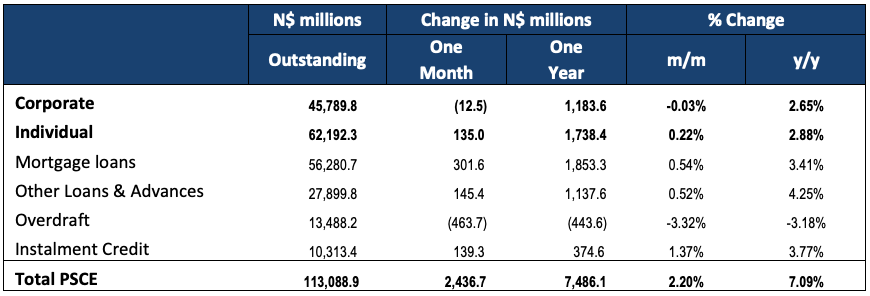

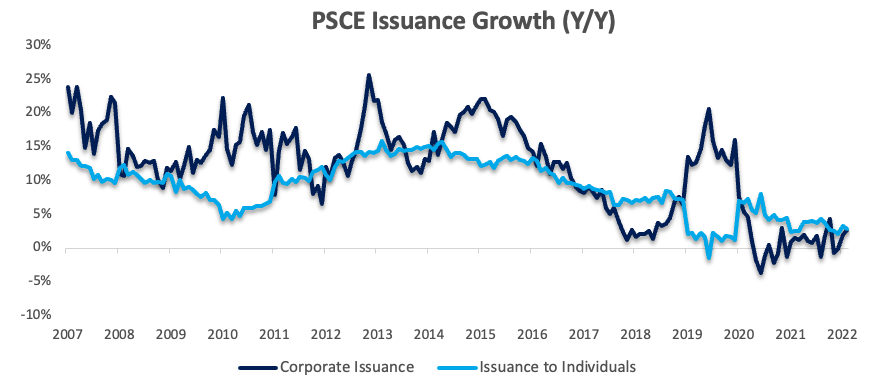

Private sector credit (PSCE) increased by N$1.78 billion or 1.6% m/m in April, bringing the cumulative credit outstanding to N$116.2 billion. On a year-on-year basis, private credit sector credit grew by 10.5% y/y, compared to the 8.7% y/y growth recorded in March. While this was another relatively large monthly increase, this month’s increase was primarily driven by an increase in corporate credit demand versus the prior three months’ increases which were driven by increases in claims on non-resident private sectors. Normalising for the increases in claims on non-resident private sectors the past three months sees annual PSCE growth at 3.4% y/y. On a 12-month cumulative basis N$11.0 billion worth of credit was extended to the private sector. The non-resident private sector has taken up the bulk of this issuance with debts over the past 12 months summing to N$7.05 billion, while corporates have taken up N$2.58 billion and individuals have taken up N$1.37 billion.

Credit Extension to Individuals

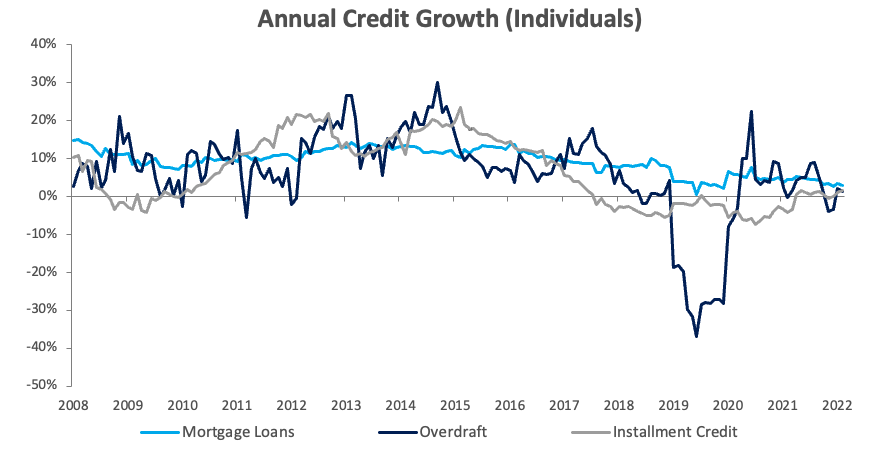

Credit extended to individuals increased by 0.5% m/m and 2.2% y/y in April. Mortgage loans to individuals rose by 0.6% m/m and 2.3% y/y. Overdraft facilities increased by 1.8% m/m, but contracted by 1.0% y/y. Other loans and advances (consisting of credit card debt, personal- and term loans) rose by 0.4% m/m and 4.1% y/y.

Credit Extension to Corporates

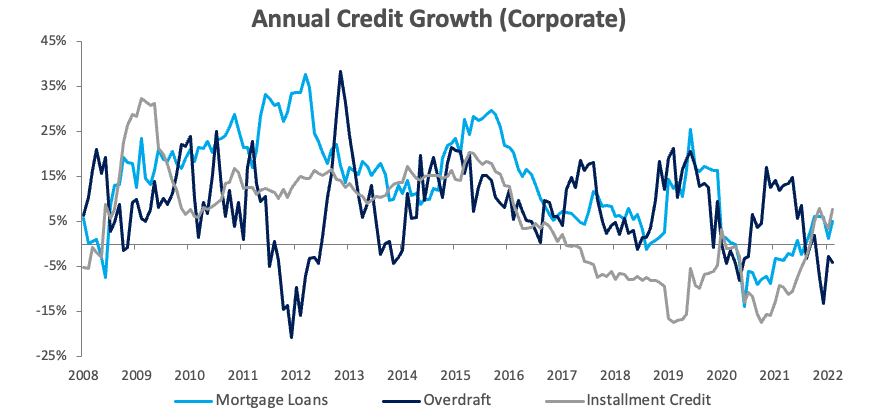

Credit extension to corporates grew by 3.1% m/m, following two months of declines. Growth in credit extension to corporates accelerated to 5.9% y/y in April, compared to 1.9% y/y growth registered in March. The increase was largely driven by a 6.4% m/m increase in ‘other loans and advances’. The Bank of Namibia (BoN) ascribed the increase to increased demand by corporates in the transport-, commercial property- and agricultural services sectors. Overdraft facilities to corporates rose by 1.9% m/m, but fell 4.4% y/y. Instalment credit by corporates fell by 0.6% m/m, although still recorded growth of 14.2% y/y.

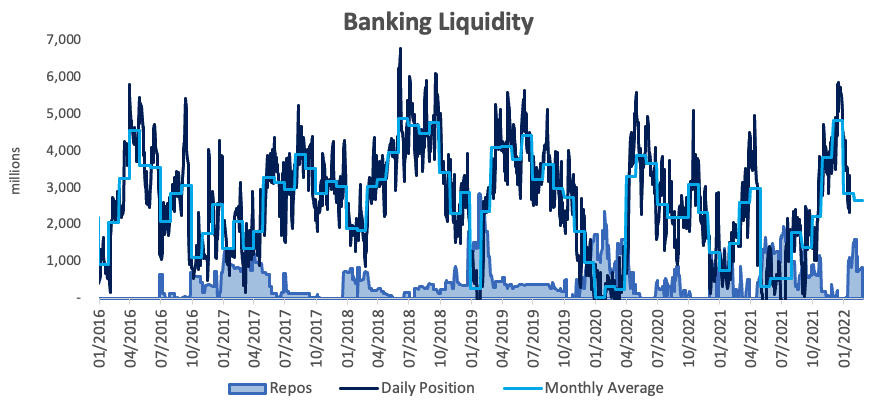

Banking Sector Liquidity

The overall liquidity position of the commercial banks fluctuated markedly in April, with the average position increasing by N$437.2 million to N$3.00 billion, while the daily position on the 29th was down N$1.21 billion from the N$3.70 billion recorded at the end of March. According to the BoN, the change was due to increased demand at the bond auctions held during the month. The repo balance rose to N$1.97 billion at the end of the month after ending March at N$936.8 million.

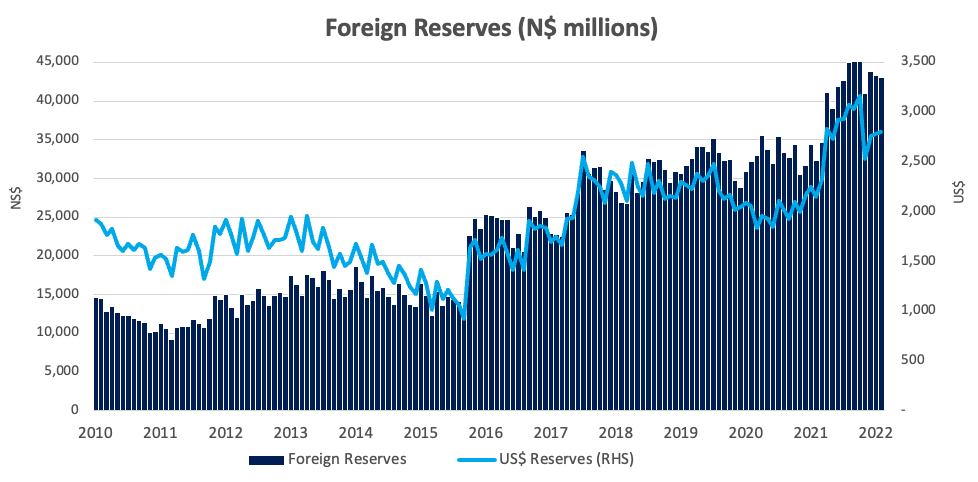

Reserves and Money Supply

The BoN’s latest figures show broad money supply (M2) increased by N$1.76 billion or 1.4% y/y to N$126.4 billion. The central bank’s stock of international reserves rose by 5.6% m/m or N$2.27 billion to N$43.0 billion. The BoN noted that the increase was due to SACU revenue inflows and the depreciation of the Namibian dollar.

Outlook

As mentioned earlier in the report, the relatively strong PSCE growth in April was largely driven by an increase in corporate credit demand, specifically in the ‘other loans and advances’ category. While an increase in corporate credit demand is generally positive, the specific category that drove this increase in April is made up of shorter term debt. Short-term debt is generally used to cover short-term cash needs, and not to expand operations, thus meaning that the increase in corporate demand in April is not necessarily an indication of investment in fixed capital, but may be into working capital.

On a 12-month cumulative basis, private sector credit issuance increased by a rather substantial 292.1% y/y to N$11.0 billion. 64.1% of this increase was however due to the large increases recorded in claims on non-resident private sectors in the first three months of the year, which the BoN previously attributed to a loan uptake by one of the commercial banks from its parent company in South Africa.