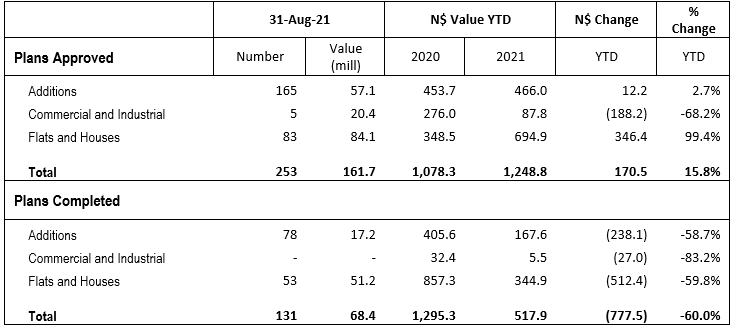

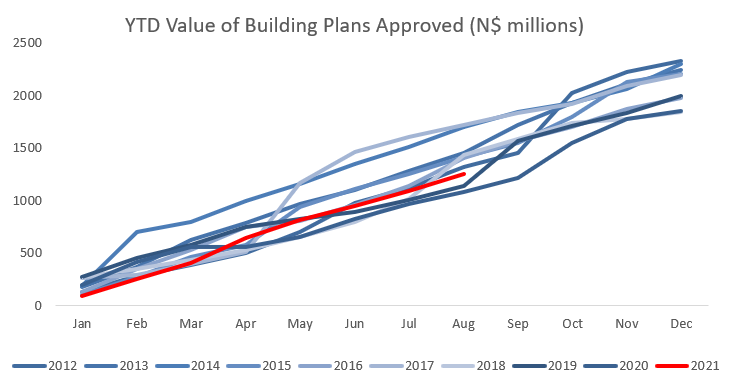

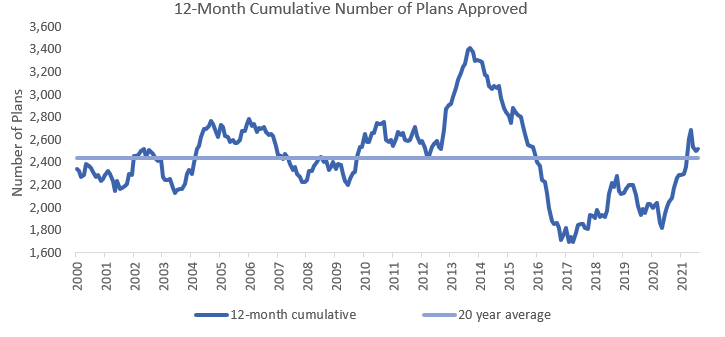

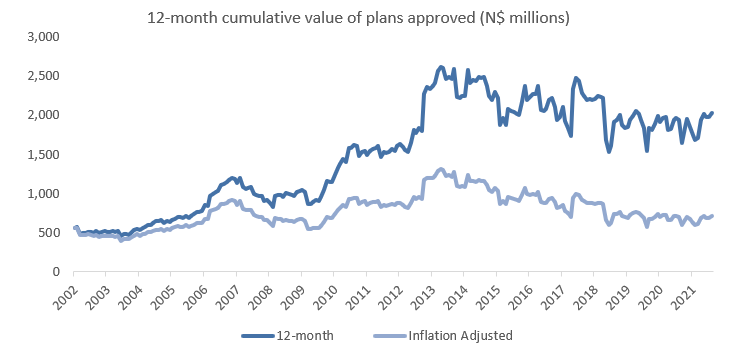

The City of Windhoek approved 253 building plans in August, a 19.9% m/m increase from the 211 approved in July. The value of approvals increased by 11.1% m/m to N$161.7 million. Year-to-date there have been 1,591 approvals, valued at N$1.25 billion, 15.8% higher in value terms and 17.3% higher in number terms than at the same time last year. On a 12-month cumulative basis, the number of building plan approvals rose by 22.8% y/y to 2,517 as the value of approvals rose by 4.5% y/y to N$2.02 billion. In August, 131 construction projects were completed at a value of N$68.4 billion. This is a marked increase from the number of completions in July when only 36 projects were completed, the second-lowest figure for the year. Year-to-date, 969 plans, valued at N$517.9 million have been completed, a 60.0% contraction in value terms compared to the same period a year ago.

Additions to properties made up 65% of total approvals in August. 165 additions were approved at a value of N$57.1 million, a 20.4% m/m increase in number, but a 12.0% m/m decrease in value from the N$64.9 worth of addition approvals in July. Year-to-date, 983 additions have been approved at a value of N$466.0 million, a 3.4% decrease in number, but a 2.7% increase in value terms. In August, 78 additions were completed at a value of N$17.18 million. Although the number and value of additions completed per month trend to vary widely – August’s figures sit close to the year-to-date averages.

New residential units were the second largest contributor to the total number of building plans approved with 83 approvals registered in August. In terms of value, the N$84.1 million worth of residential units approved in August represents a 4.7% m/m increase. Year-to-date 583 units worth N$694.9 million have been approved, double the value of residential approvals achieved this time last year. On a 12-month cumulative basis, the number of residential units approved increased by 123.1% y/y and 98.0% in value terms. 53 new residential units worth N$51.2 million were completed in August. This represents a year-to-date decrease in value of 59.8% compared to this time last August. On a 12-month cumulative basis, the number of residential units completed stands is 526 at a value of N$531.8 million. As such, the 12-month cumulative value of completed residential units decreased, by 45.1% y/y, for the first time in over a year.

In August five commercial units, valued at N$20.4 million, were approved. Year-to-date, 25 commercial buildings at a value of N$87.8 million have been approved. No commercial building projects have been completed since March. This is the longest run of zero completions in the commercial construction sector since independence. Commercial projects continue to be approved; they are not being completed.

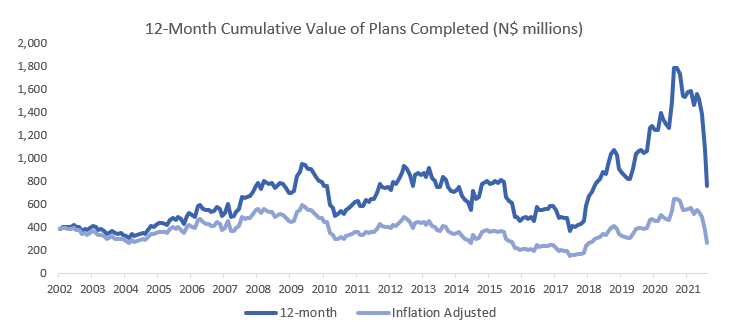

On a 12-month cumulative basis, the number of buildings completed fell by 42.9% y/y, translating to a 57.4% y/y decrease in value. There is a simple, mechanical explanation for this. Namibia’s first hard lockdown of 2020 put a pause on all building projects. In April of that year no construction projects; be that additions, residential units or commercial projects were completed. This is likely to have created a glut of unfinished construction projects. As construction sites reopened, the following five months saw a massive spike in the value of completed projects. For example, in August of 2020 the value of completed construction projects was N$395.0 million – the most ever added in one month. This August’s figure for the 12-month cumulative value of completed construction projects is the first this year to not consider the large, distorted, values of completed projects from the May 2020 – September 2020 post-lockdown period. The 12-month cumulative value of plans completed now, despite the large decrease recorded this August, gives a more accurate picture of the short-term trends and current conditions in the Namibian construction industry.