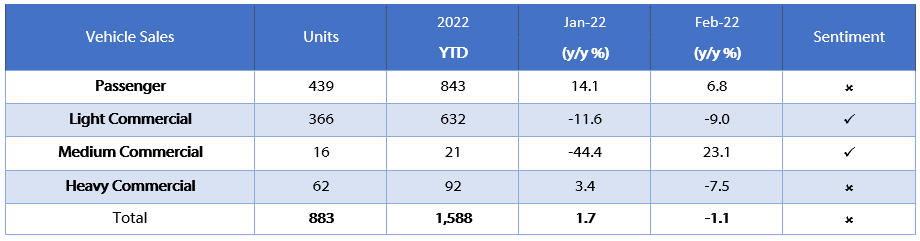

A total of 883 new vehicles were sold in February, which is 178 more than were sold in January but represents a 1.1% y/y decrease from the 893 vehicles sold in February 2021. During the first two months 1,588 new vehicles have been sold, of which 843 were passenger vehicles, 632 light commercial vehicles, and 113 medium and heavy commercial vehicles. By comparison, the first two months of 2021 saw 1,586 new vehicles sold. 2022 is thus off to a similar start compared to last year. On a 12-month cumulative basis, new vehicle sales have grown by 22.0% y/y to 9,430.

439 new passenger vehicles were sold during February, an increase of 8.7% m/m from the 404 sold in January, and an increase of 6.8% y/y from the 411 vehicles sold in February 2021. On a 12-month cumulative basis, new passenger vehicle sales have increased by 36.5% y/y to 4,562. Encouragingly, on a year-to-date basis, new passenger vehicle sales for February have exceeded 2020 and 2021 levels, with the 843 sold so far this year, 78 more than in 2021 and 209 higher than over the same period in 2020.

444 commercial vehicles were sold in February, a 47.5% m/m increase but 7.9% y/y decrease. While all three sub-categories recorded better sales than last month, the monthly increase was primarily driven by a strong increase in light commercial vehicle sales of 37.6% m/m following the relatively sharp decline in January. Medium commercial vehicle sales rose by 23.1% y/y while heavy commercial vehicle sales fell by 7.5% y/y. On a twelve-month cumulative basis, light commercial vehicle sales have increased by 6.6% y/y, medium commercial vehicles rose by 27.0% y/y, and heavy commercial vehicles recorded an increase of 46.7% y/y.

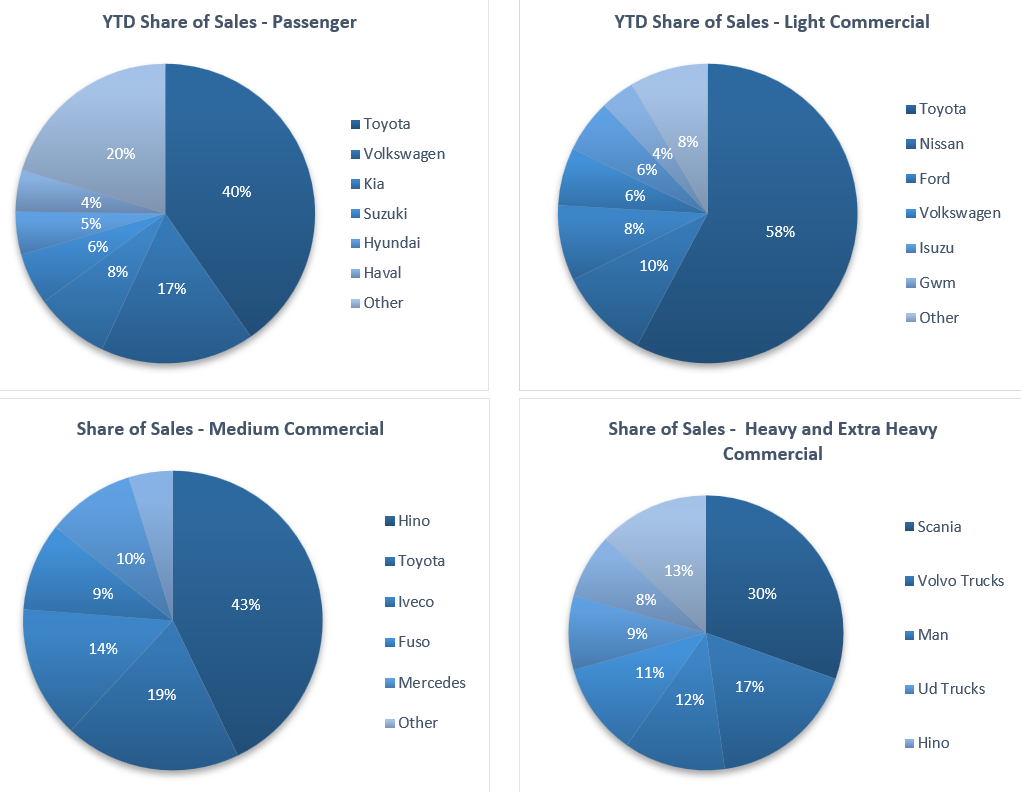

Toyota enjoys a strong lead in the passenger vehicle sales segment with a with a 40.3% of the segment sales year-to-date, followed by Volkswagen with 16.6% of the market share. Both manufacturers have started the year off on a strong foot that will make it difficult for other manufacturers to catch up. They were followed by Kia and Suzuki with 8.1% and 5.6% of the market, respectively, leaving the remaining 29.4% of the market to other brands.

On a year-to-date basis, Toyota remained the leader in the light commercial vehicle space with a 57.8% market share. Nissan came in second place claiming a market share of 9.9%. Hino claimed 42.9% of the market for medium commercial vehicles, followed by Toyota with a market share of 19.0%. There appears to be relatively stronger competition in the heavy and extra-heavy commercial vehicle space as Scania, Volvo Trucks and MAN achieved market shares of 30%, 17% and 12% respectively.

The Bottom Line

February’s new vehicle sales figure of 883 was the highest number since March 2021, when 919 new vehicles were sold. On a 12-month cumulative basis, new passenger vehicle sales have encouragingly increased 15 consecutive months, possibly reflecting a minor uptick in consumer confidence. As mentioned last month, the strong increase in commercial vehicle sales is positive news, as it indicates that a few companies and mines are starting to upgrade their fleets. This indicates improving business optimism. While we estimate new vehicle sales to be marginally higher than the previous two years as the economy starts recovering, we do not expect to see a major uptick in sales the short-term. The recently tabled 2022/23 national budget also indicated that the government will not be a major buyer of new vehicles in the coming financial year.