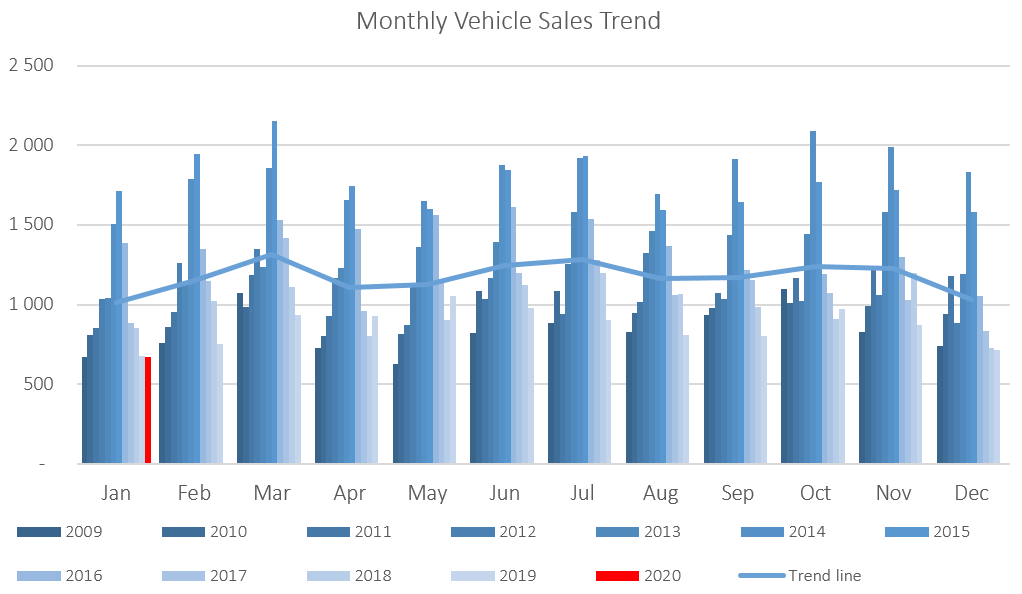

A total of 671 new vehicles were sold in January, which represents 6.0% m/m decrease from the 714 vehicles sold in December, and a drop of 1.0% from the 678 new vehicles sold in January 2019. On a twelve-month cumulative basis, a total of 10,394 new vehicles were sold as at January 2020, representing a contraction of 11.4% from the 11,733 sold over the same period a year ago. 2020 is thus off to sluggish start as illustrated by the lowest monthly new vehicles sales number since May 2009.

291 new passenger vehicles were sold during January, a contraction of 7.3% m/m from the 314 passenger vehicles sold in December, and a decline of 14.9% y/y from the 342 new passenger vehicles sold in January 2019. On a rolling 12-month basis, new passenger vehicle sales fell 1.1% m/m and 10.6% y/y at the end of January, and were down 54.2% from the peak in April 2015.

Commercial vehicle sales declined to 380 units in January, representing a contraction of 5.0% m/m, but an increase of 13.1% y/y. During the month 335 light commercial vehicles, 14 medium commercial vehicles, and 31 heavy commercial vehicles were sold. On a year-on-year basis, light commercial sales have increased by 11.3%, medium commercial vehicles were flat, and heavy and extra heavy vehicle sales rose 47.6% y/y. On a twelve-month cumulative basis, light commercial vehicle sales have declined by 14.9% y/y, medium commercial vehicles rose by 9.0% y/y, and heavy commercial vehicles sales rose 17.6% y/y.

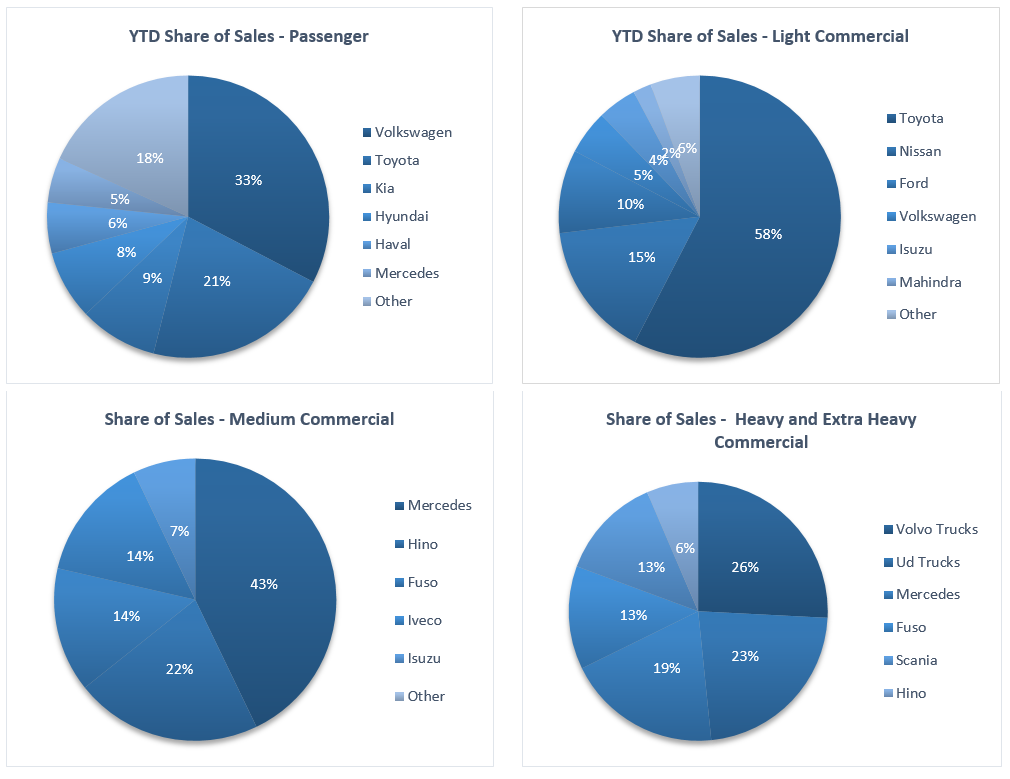

Volkswagen started the year off with a 32.6% market share of new passenger vehicles sold, followed by Toyota with a 21.3% market share. They were followed by Kia and Hyundai with 8.9% and 7.9% of the market respectively, while the rest of the passenger vehicle market was shared by several other competitors.

Toyota meanwhile started the year off with a solid grip on the light commercial vehicle market with a 57.6% market share, with Nissan in second place with a 15.5% market share. Ford and Volkswagen claimed 9.6% and 5.1% of the number of new light commercial vehicles sold during the month, respectively. Mercedes lead the medium commercial vehicle category with 42.9% of sales, while Volvo was number one in the heavy and extra-heavy commercial vehicle segment with 25.8% of the market share during the month.

The Bottom Line

Cumulative new vehicle sales fell to the lowest level in ten years on a rolling 12-month basis. This is a consequence of the incessant recessionary environment we find ourselves in, which is characterised by depressed business and consumer confidence, as well as lower government spending. The low sales figures show that both consumers and businesses continue to face economic hardship, with many preferring to hold on to their existing vehicles for longer, or opting to buy second-hand vehicles instead. The prospects for new vehicle sales in 2020 are likely to remain dim as economic conditions are expected to remain difficult for the rest of the year.