Twitter Timeline

[custom-twitter-feeds]

Categories

- Calculators (1)

- Company Research (300)

- Capricorn Investment Group (52)

- FirstRand Namibia (54)

- Letshego Holdings Namibia (26)

- Mobile Telecommunications Limited (7)

- NamAsset (3)

- Namibia Breweries (45)

- Oryx Properties (59)

- Paratus Namibia Holdings (6)

- SBN Holdings Limited (18)

- Economic Research (663)

- BoN MPC Meetings (13)

- Budget (19)

- Building Plans (142)

- Inflation (143)

- Other (28)

- Outlook (17)

- Presentations (2)

- Private Sector Credit Extension (142)

- Tourism (7)

- Trade Statistics (4)

- Vehicle Sales (144)

- Media (25)

- Print Media (15)

- TV Interviews (9)

- Regular Research (1,820)

- Business Climate Monitor (75)

- IJG Daily (1,623)

- IJG Elephant Book (12)

- IJG Monthly (108)

- Team Commentary (250)

- Danie van Wyk (61)

- Dylan van Wyk (27)

- Eric van Zyl (16)

- Hugo van den Heever (1)

- Leon Maloney (11)

- Top of Mind (4)

- Zane Feris (12)

- Uncategorized (6)

- Valuation (4,530)

- Asset Performance (117)

- IJG All Bond Index (2,103)

- IJG Daily Valuation (1,821)

- Weekly Yield Curve (488)

Meta

Category Archives: Economic Research

PSCE – November 2019

Overall

Private sector credit (PSCE) increased by N$586.8 million or 0.58% m/m in November, bringing the cumulative credit outstanding to N$102.5 billion. On a year-on-year basis, private sector credit increased by 5.92% in November, somewhat slower than the 6.14% growth rate recorded in October. On a rolling 12-month basis, N$5.7 billion worth of credit was extended to the private sector, with individuals taking up N$3.7 billion while N$2.2 billion was extended to corporates, and the non-resident private sector has decreased their borrowings by N$205.0 million.

Credit Extension to Individuals

Credit extended to individuals increased by 6.6% y/y in November, almost unchanged from the 6.7% y/y growth recorded in October. On a monthly basis household credit increased by 0.6%, once again a similar pace to the 0.5% growth registered in October. Mortgage loans extended to individuals grew by 0.2% m/m and 5.7% y/y, compared to 0.6% m/m and 6.5% y/y in October. Household appetite for instalment credit remains subdued as reflected in the contractions of 0.4% m/m and 5.8% y/y in November. Other loans and advances grew at a relatively quick pace of 4.3% m/m and 27.3% y/y during the month, indicating that consumers remain stretched as they are taking on more credit card debt, personal, and term loans.

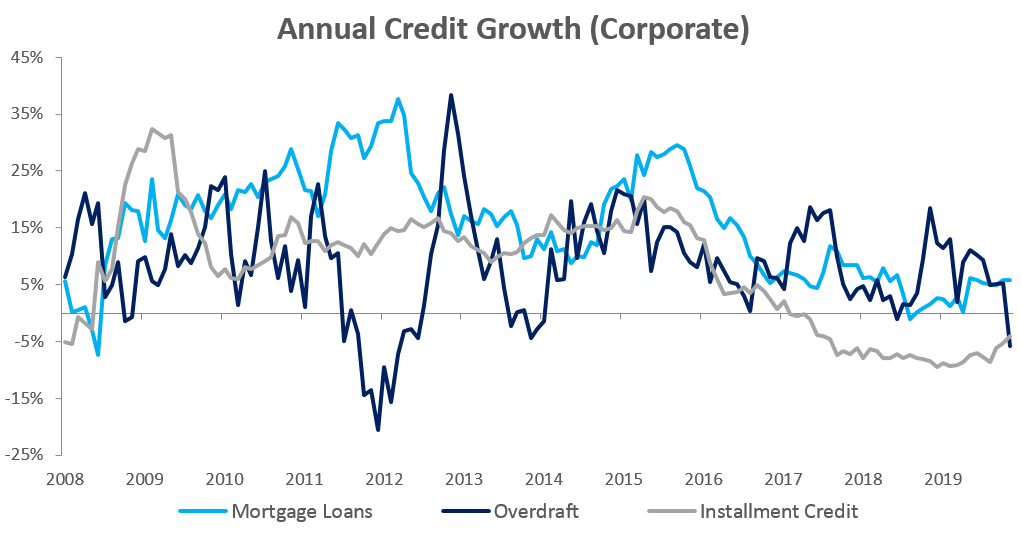

Credit Extension to Corporates

Credit extension to corporates grew by 0.4% m/m and 5.7% y/y in November, compared to the growth of 0.3% m/m and 6.0% y/y recorded in October. On a rolling 12-month basis N$2.2 billion was extended to corporates, a far cry from the highs of over N$5.3 billion recorded for the 12 months ending in February 2015. Installment credit extended to corporates printed flat m/m, but contracted by 4.1% y/y in November. Leasing transactions to corporations declined by 2.4% m/m and 34.2% y/y. Overdraft facilities extended to corporates contracted by 2.6% m/m and 5.8% y/y, making it the first contraction on an annual basis since June 2018. Whether corporates will continue to pay back overdraft facilities going forward remains to be seen, although it seems unlikely as economic conditions remain challenging. Mortgage loans extended to corporates grew by 0.5% m/m and 5.9% y/y, while other loans and advances grew by 2.9% m/m and 15.8% y/y.

Banking Sector Liquidity

The overall liquidity position of commercial banks deteriorated during November, declining by N$925.3 million to reach an average of N$1.84 billion. Bank of Namibia attributed the decline in liquidity to higher issuance of BoN bills and the issuance of a new Treasury Bill, coupled with cross border payments made during November.

Reserves and Money Supply

Broad money supply rose by 9.3% y/y in November, following a 6.7% y/y increase in October, as per the BoN’s latest money statistics release. Foreign reserve balances fell by 8.4% m/m to N$29.8 billion in November. The BoN stated that the decline was due to the net purchases of South African Rands by commercial banks for import payments coupled with increasing government foreign payments during the month under review.

Outlook

Overall PSCE growth in November moderated for a third consecutive month on a year-on-year basis, increasing by 5.9%. Rolling 12-month private sector credit issuance is down 21.0% from the N$7.2 billion issuance observed at the end of November 2018, with individuals taking up most (65.2%) of the credit extended over the past 12 months.

Low economic activity and a lack of demand means that growth opportunities for businesses remain limited. Consumer confidence will first need to improve before corporate demand for credit will increase. Increased consumer demand results in more business production that must satisfy this demand, thus incentivising businesses to borrow in order to fund capital and expansionary projects. Until such a time that consumer confidence increase, we do not expect to see any significant growth in PSCE. It is unlikely that monetary policy will drive PSCE growth in the coming year, as interest rates are not far off historically low levels.

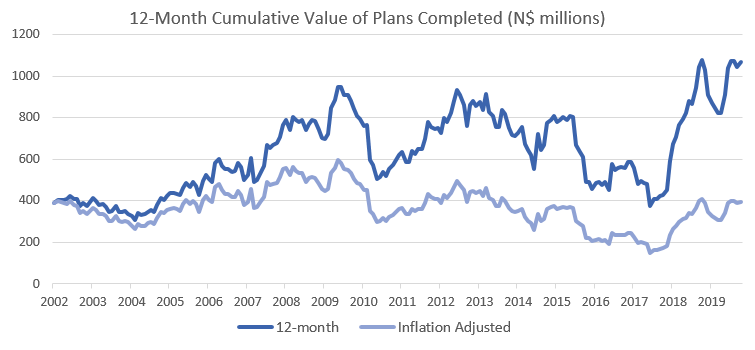

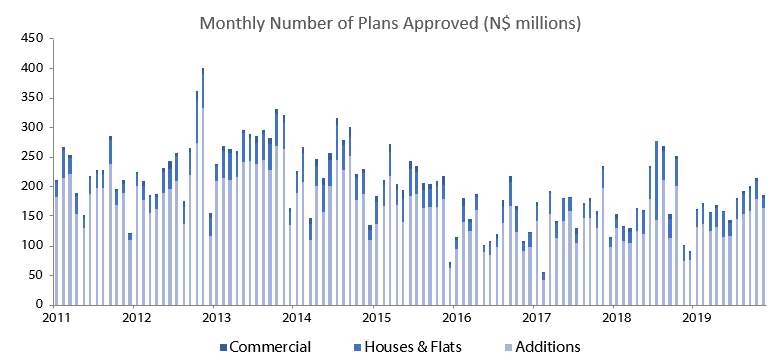

Building Plans – November 2019

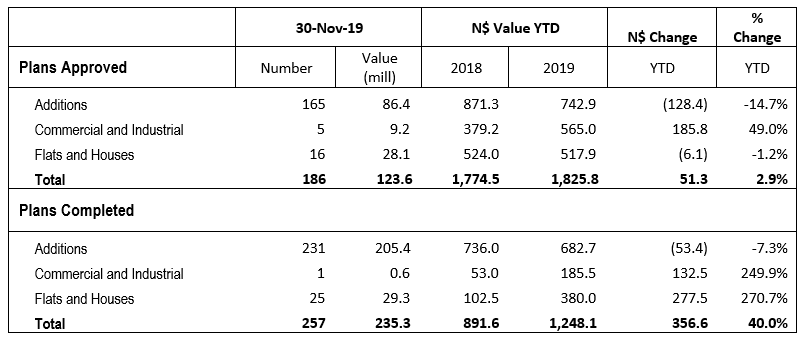

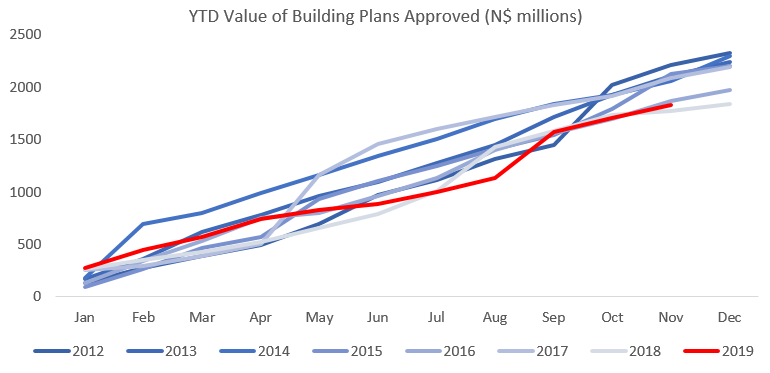

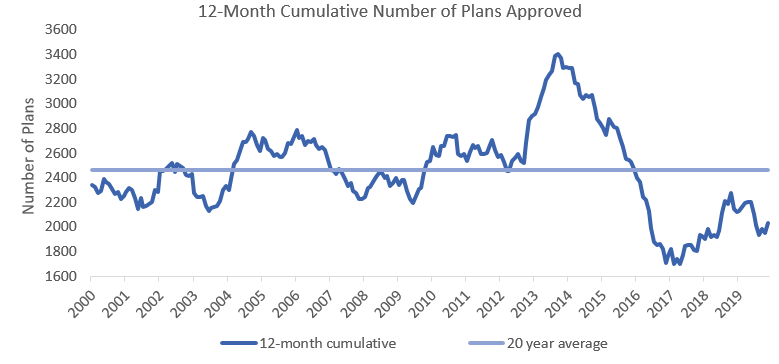

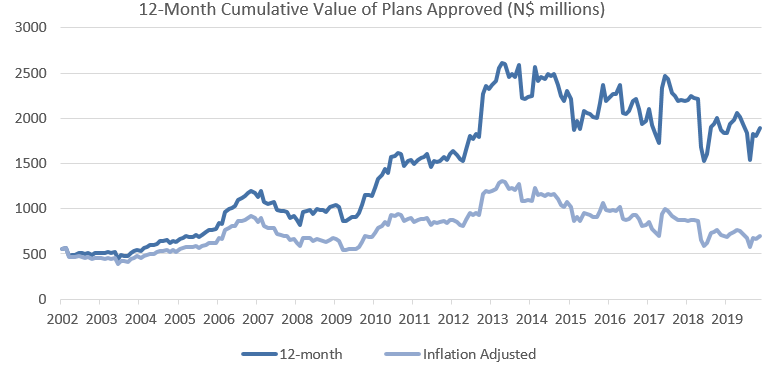

A total of 186 building plans were approved by the City of Windhoek in November. This is a 13.1% contraction in the number of plans approved on a monthly basis when compared to the 214 building plans approved in October. The approvals were valued at N$123.6 million, a decrease of N$11.0 million or 8.2% compared to the prior month. The number of completions for the month of November stood at 257, valued at N$235.3 million. The year-to-date value of approved building plans currently stands at N$1.83 billion, 2.9% higher than at the end of November 2018. On a twelve-month cumulative basis 2,032 building plans worth approximately N$1.89 billion have been approved, a decrease of 5.2% y/y in number but an increase of 0.8% in value terms over the prior 12-month period.

The largest portion of building plan approvals was once again made up of additions to properties. 165 additions to properties were approved in November, a 120.0% increase year-on-year but 7.8% decrease over the number of additions approved in October. Year-to-date 1,565 additions to properties have been approved with a cumulative value of N$742.9 million, a decline of 14.7% y/y in terms of value compared to the same period in 2018. Completed additions amounted to 231, valued at N$205.4 million, an increase of 7.4%% m/m in number and 149.6% m/m in value. Year-to-date 1,259 additions have been completed to a value of N$682.7 million, a drop of 43.1% y/y in number and 7.3% y/y in value.

New residential units were the second largest contributor to the number of building plans approved with 16 approvals registered in November, compared to 31 in October. In value terms, N$28.1 million worth of residential units were approved in November, a decreases of 41.3% m/m but an increase of 42.2% y/y. 332 New residential units valued at N$517.9m were approved in the first eleven months of 2019, 29.2% y/y less in number and 1.2% y/y less in value than during the corresponding period in 2018. 25 Residential units valued at N$29.3 million were completed in November bringing the year-to-date number to 279, up 350% y/y, and value to N$380 million, up 270.7% y/y.

Commercial and industrial building plans approved in November amounted to 5 units, worth N$9.2 million. The number of approvals for commercial and industrial properties has been languishing in single digit territory since September 2016 and has an average approval rate of less than 4 approvals per month over the last 12 months. On a year-to-date basis, the number of commercial and industrial approvals increased by 10.0% y/y in November to 44 units, worth approximately N$565.0 million, an increase of 49.0% in value terms over the period ending November 2018. One commercial and industrial building plan was recorded as completed in November, valued at N$600,000.

During the last 12 months, 2,032 building plans have been approved, decreasing by 5.2% y/y. These approvals were worth a combined N$1.89 billion, an increase in value of 0.8% y/y. The last 3 months have seen a steady uptick in the 12-month cumulative value of plans approved in the capital although this measure is still trending downward from a longer term perspective. The value of plans completed has however recovered more significantly as can be seen in the below figure.