Twitter Timeline

[custom-twitter-feeds]

Categories

- Calculators (1)

- Company Research (300)

- Capricorn Investment Group (52)

- FirstRand Namibia (54)

- Letshego Holdings Namibia (26)

- Mobile Telecommunications Limited (7)

- NamAsset (3)

- Namibia Breweries (45)

- Oryx Properties (59)

- Paratus Namibia Holdings (6)

- SBN Holdings Limited (18)

- Economic Research (663)

- BoN MPC Meetings (13)

- Budget (19)

- Building Plans (142)

- Inflation (143)

- Other (28)

- Outlook (17)

- Presentations (2)

- Private Sector Credit Extension (142)

- Tourism (7)

- Trade Statistics (4)

- Vehicle Sales (144)

- Media (25)

- Print Media (15)

- TV Interviews (9)

- Regular Research (1,820)

- Business Climate Monitor (75)

- IJG Daily (1,623)

- IJG Elephant Book (12)

- IJG Monthly (108)

- Team Commentary (250)

- Danie van Wyk (61)

- Dylan van Wyk (27)

- Eric van Zyl (16)

- Hugo van den Heever (1)

- Leon Maloney (11)

- Top of Mind (4)

- Zane Feris (12)

- Uncategorized (6)

- Valuation (4,530)

- Asset Performance (117)

- IJG All Bond Index (2,103)

- IJG Daily Valuation (1,821)

- Weekly Yield Curve (488)

Meta

Category Archives: Economic Research

New Vehicle Sales – December 2019

714 New vehicles were sold in December, down 18.4% m/m from the 875 vehicles sold in November, and a decrease of 2.2% y/y from the 730 new vehicles sold in December 2018. Year-to-date 10,401 vehicles have been sold, a 12.6% contraction from December last year and the lowest annual vehicle sales figure since 2009. Of the 10,401 new vehicles sold during the year, 4,550 were passenger vehicles, 5,101 were light commercial vehicles, and were 750 medium and heavy commercial vehicles.

A total of 314 new passenger vehicles were sold during December, representing a 9.5% m/m contraction, but a 1.3% y/y increase. 4,550 passenger vehicles were sold in 2019, a 10.7% decline from 2018 and lower annual sales than the preceding nine years. Passenger vehicle sales made up 43.7% of the total number of new vehicles sold during 2019, broadly in line with the trend over the last 5 years.

Commercial vehicle sales declined to 400 units in December, a 24.2% m/m, and 4.8% y/y contraction. During the month 335 light commercial vehicles, 21 medium commercial vehicles, and 44 heavy commercial vehicles were sold. On a year-on-year basis, light commercial sales have declined by 12.3%, medium commercial vehicles rose by 90.9%, and heavy and extra heavy vehicle sales rose 37.5% y/y. On a twelve-month cumulative basis, light commercial vehicle sales dropped 17.1% y/y, while medium commercial vehicle sales rose 9.0% y/y, and heavy commercial vehicle sales rose 17.5% y/y.

Volkswagen lead the market for new passenger vehicle sales in 2019, claiming 30.5% of the market, followed by Toyota with a 28.3% share. They were followed by Kia and Mercedes at 5.8% and 5.5% respectively, while the rest of the passenger vehicle market was shared by several other competitors.

Toyota remained the leader in the commercial vehicle space in 2019 with 57.3% market share, with Nissan in second place with a 12.4% share. Ford and Isuzu claimed 9.3% and 7.6% respectively of the number of new light commercial vehicles sold for the year. Hino lead the medium commercial vehicle category with 39.8% of sales while Scania was number one in the heavy and extra-heavy commercial vehicle segment with 35.5% of the market share during the year.

The Bottom Line

New vehicle sales figures were quite dismal in 2019 with the cumulative number of new vehicles sales for the year amounting to 10,401, a decline of 12.6% from the cumulative number of vehicles sold in 2018 and a 54.1% contraction from the peak, on a cumulative 12-month basis, of 22,664 new vehicle sales recorded in April 2015. We expect new vehicle sales to remain under pressure in 2020 as there is little sign that the economy will show any meaningful growth. December new vehicle sales have historically been low when compared to most other months, but 2019’s December figure was the lowest since 2008, showing just how badly the ongoing recession has impacted demand and investment.

NCPI – December 2019

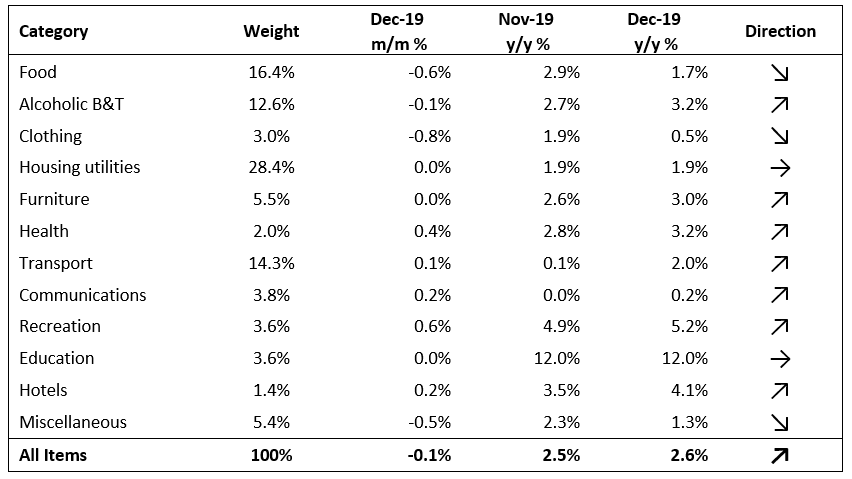

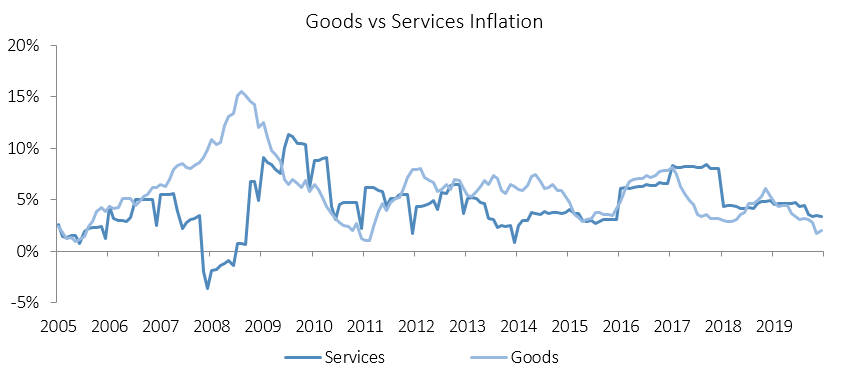

The Namibian annual inflation rate increased marginally to 2.6% in December, following the 2.5% y/y increase in prices recorded in December. Prices in the overall NCPI basket decreased by 0.1% m/m. The annual average inflation rate for 2019 was 3.7%, compare to 4.3% in 2018 and 6.2% in 2017. On a year-on-year basis, overall prices in seven of the twelve basket categories rose at a quicker rate in December than in November, with three categories recording slower rates of inflation and two categories recorded increases consistent with the prior month. Prices for goods increased by 2.0% y/y while prices for services increased by 3.4% y/y.

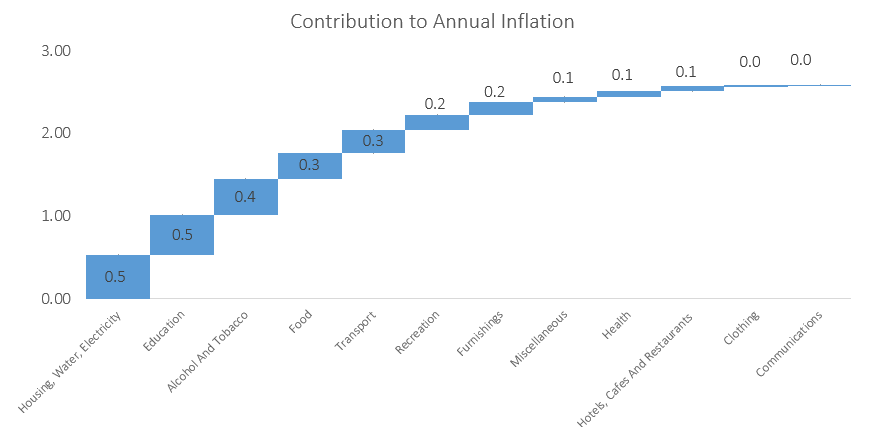

In December the housing and utilities category was once again the largest contributor to annual inflation due to its large weighting in the basket, accounting for 0.5 percentage points of the total 2.6% annual inflation rate. Price inflation for this category came in at 1.9% y/y for a third consecutive month and remained relatively flat month-on-month. Prices in the electricity, gas and other fuels subcategory remained flat m/m, but declined by 0.8% y/y. The regular maintenance and repair of dwellings subcategory registered an increase in prices of 5.0% y/y. Month-on-month, prices in this subcategory fell by 0.7%. Annual inflation for rental payments remained unchanged at 2.3% y/y in December.

The education basket recorded inflation of 12.0% y/y, with the cost of pre-primary and primary education growing at a rate of 12.6% y/y, while secondary- and tertiary education recorded price increases of 11.0% y/y and 12.7% y/y, respectively. All three subcategories printed no price increases on a month-on-month basis.

The alcohol and tobacco category displayed a decrease of 0.1% m/m, but an increase of 3.2% y/y. The main driver in this basket category was alcohol prices which increased by 4.9% y/y while tobacco prices were down 4.3% y/y. A 7.8% m/m decrease in tobacco prices, recorded in May, is the cause for annual decrease in tobacco prices. The Namibia Statistics Agency (NSA) has not provided any explanation for this decrease in any of its bulletins since May.

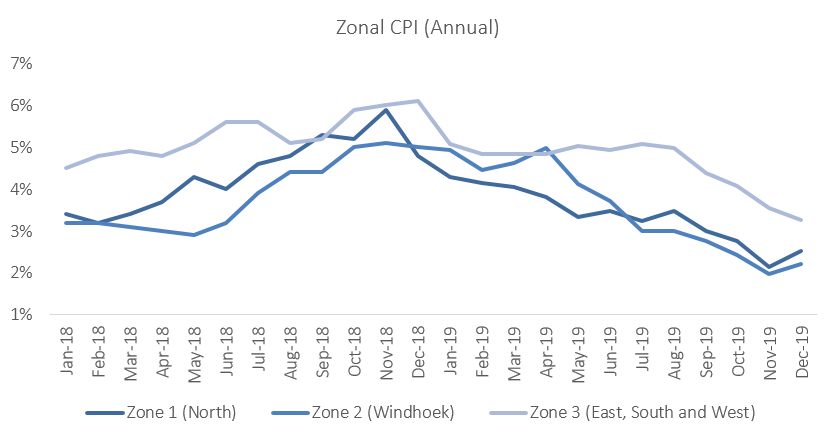

The zonal data shows that prices fell by 0.3% m/m in the northern regions, and by 0.1% m/m in the east, south and western regions, while rising by 0.1% m/m in the central region. On an annual basis, the Central region recorded the lowest inflation rate at 2.2% in December, with the mixed zone 3 covering the south, east and west of the country recording the highest rate of inflation at 3.3%. Inflation in the northern region of the country increased to 2.5% y/y.

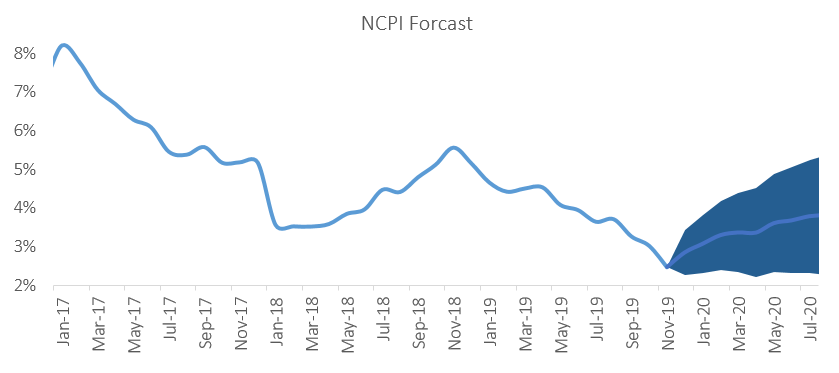

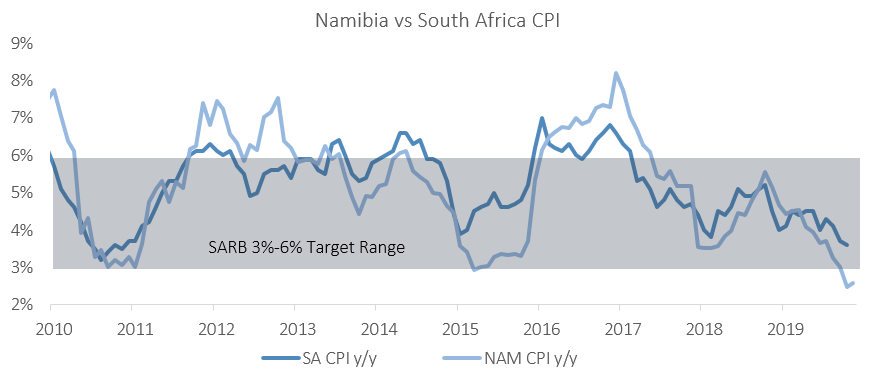

The Namibian annual inflation rate of 2.6% for December continues to trend lower than that of neighbouring South Africa’s November inflation figure of 3.6%. Inflationary pressure in Namibia has been particularly low in the second half of 2019 due to a lack of demand for both goods and services. IJG’s inflation model forecasts an average inflation rate of 3.5% y/y in 2020. The largest upside risk to this forecast is higher food costs and fuel prices. Although the northern and central regions received an encouraging amount of rainfall in December, large parts of the southern region are yet to receive their first rains. Food prices will likely increase if the country experiences another year of below average rainfall.

Geopolitical tension between the US and Iran seems to have calmed down (for the moment at least) and the price of Brent Crude oil has ‘normalised’ at US$64 at the time of writing after spiking to US$71 last week. However, peace in the middle east is all-but-certain and the situation can escalate within the wink of an eye, which will send the price of oil up again. Another potential risk for the oil price is if OPEC goes ahead with the implementation of its plan to cut production by 500,000 barrels per day. Such shocks in the oil price will result in the Ministry of Mines and Energy increasing fuel pump prices for Namibians which will translate into higher transport inflation.