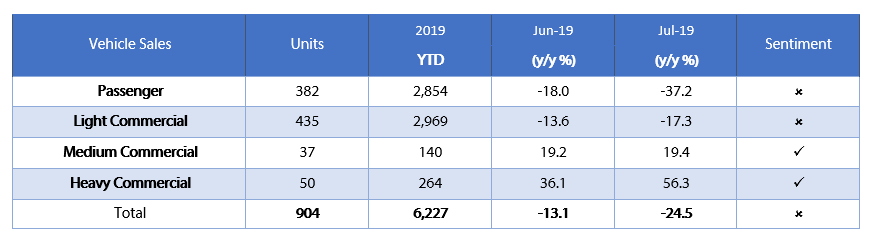

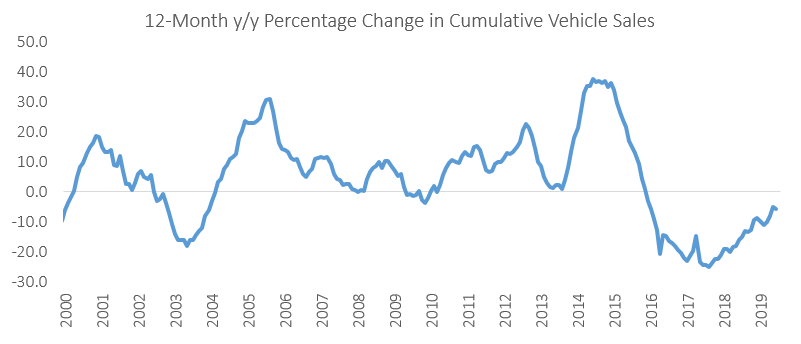

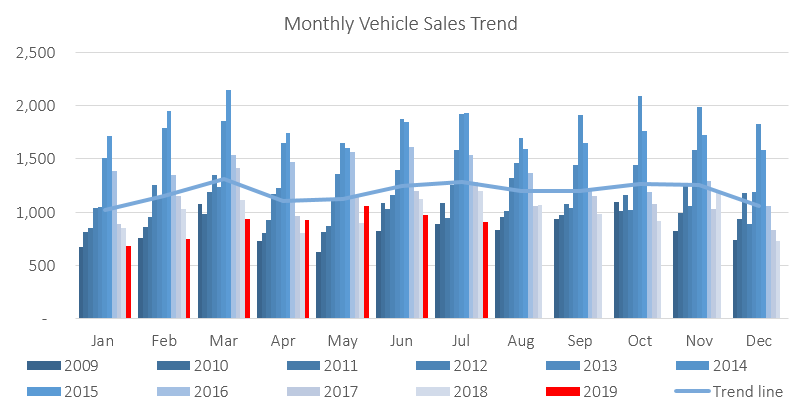

A total of 904 new vehicles were sold in July, representing a 7.5% m/m decrease from the 977 vehicles sold in June. Year-to-date, 6,227 vehicles have been sold of which 2,854 were passenger vehicles, 2,969 were light commercial vehicles, and 404 were medium and heavy commercial vehicles. On an annual basis, twelve-month cumulative new vehicle sale continued on a downward trend, contracting by 7.5% from the 11,119 new vehicles sold over the comparable period a year ago.

382 New passenger vehicles were sold in July, increasing by 1.1% m/m, but contracting by 37.2% y/y. Year-to-date passenger vehicle sales rose to 2,854 units, down 11.1% when compared to the year-to-date figure recorded in July 2018. On an annual basis, twelve-month cumulative passenger vehicle sales fell 4.6% m/m and 8.9% y/y as figures continue to reflect weakness in the number of passenger vehicles sold.

A total of 522 new commercial vehicles were sold in July, representing a contraction of 12.9% m/m and 11.4% y/y. Of the 522 commercial vehicles sold in July, 435 were classified as light commercial vehicles, 37 as medium commercial vehicles and 50 as heavy or extra heavy commercial vehicles. On a twelve-month cumulative basis, light commercial vehicle sales dropped 8.8% y/y, while medium commercial vehicle sales remained flat, and heavy commercial vehicle sales rose by 28.8% y/y. While heavy commercial vehicles continue to record growth on a twelve-month cumulative basis, the light segment of the market continues to see lower volumes sold than in 2018.

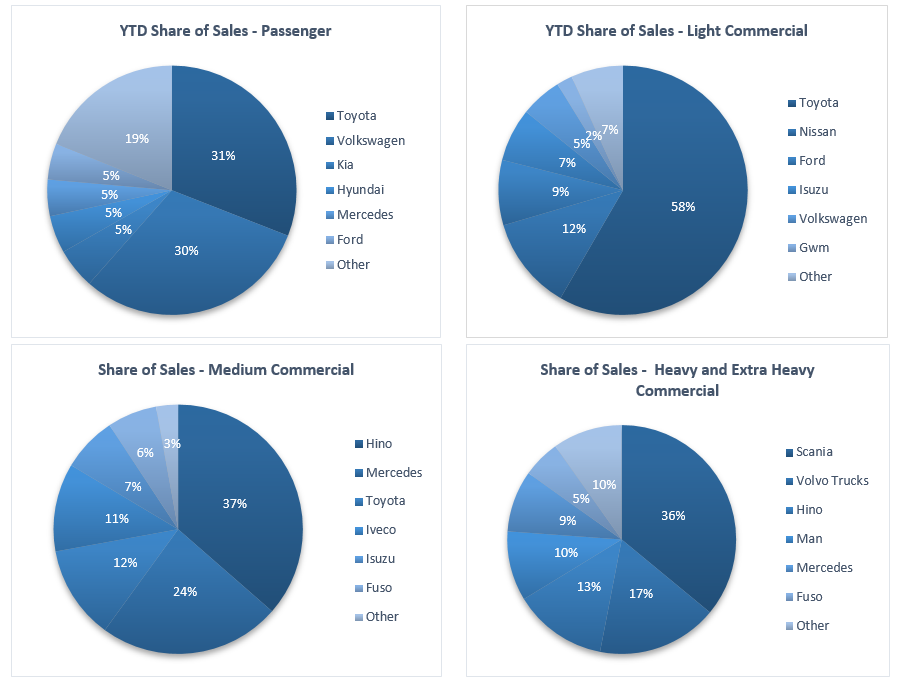

Toyota once again leads the passenger vehicle sales segment with 30.9% of the segment sales year-to-date. Volkswagen dropped to second place by this measure with 30.6% of the market-share as at the end of July. Kia, Hyundai, Mercedes and Ford each command around 5.0% of the market in the passenger vehicles segment, leaving the remaining 18.9% of the market to other brands.

Toyota with a strong market share of 58.4% year-to-date commands the light commercial vehicles sales segment. Nissan remains in second position in the segment with 12.1% of the market, while Ford makes up third place with 8.5% of the year-to-date sales. Hino leads the medium commercial vehicle segment with 36.4% of sales year-to-date, while Scania was number one in the heavy- and extra-heavy commercial vehicle segment with 36.0% of the market share year-to-date.

The Bottom Line

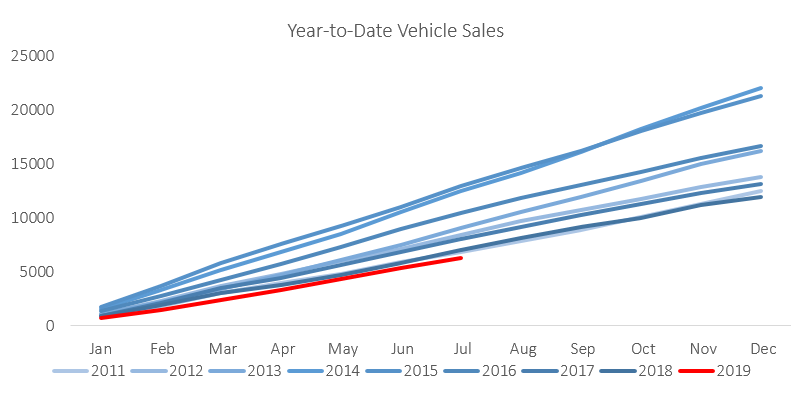

Vehicle sales remain under pressure, with the year-to-date new vehicle sales in 2019 currently below 2011 levels, and the total new vehicle sales for the last 12 months down 7.5% from the same period in 2018. The prospects for new vehicle sales remain dim in the short- to medium-term as government remains committed to fiscal consolidation. Business and consumer confidence remain depressed as a result of the of the recessionary environment we find ourselves in.