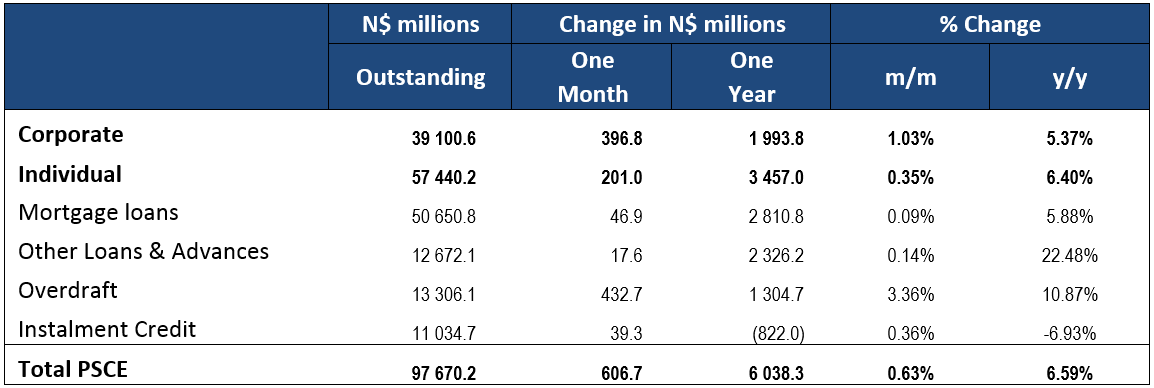

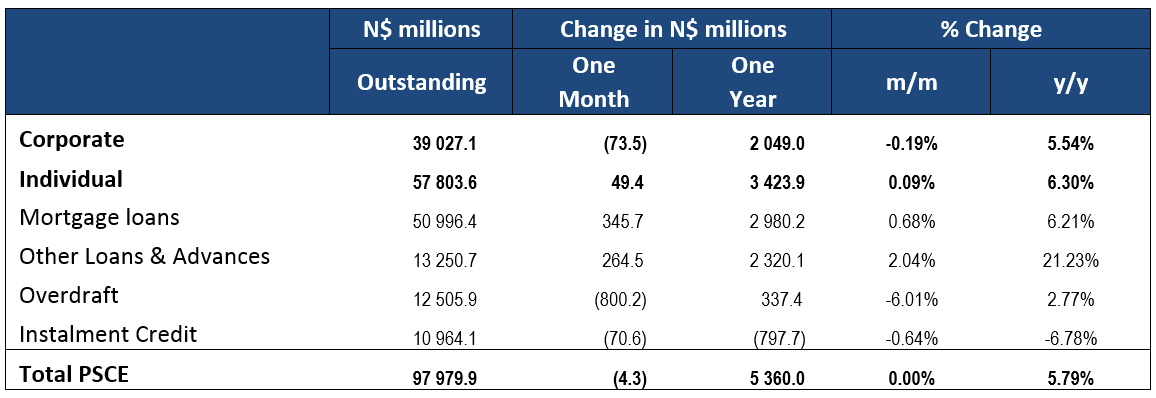

Overall

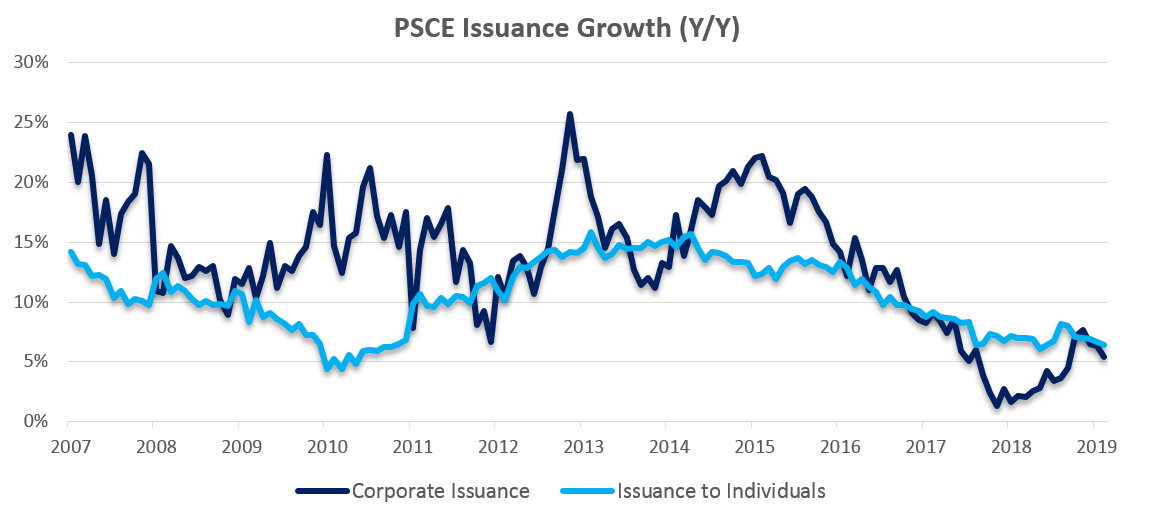

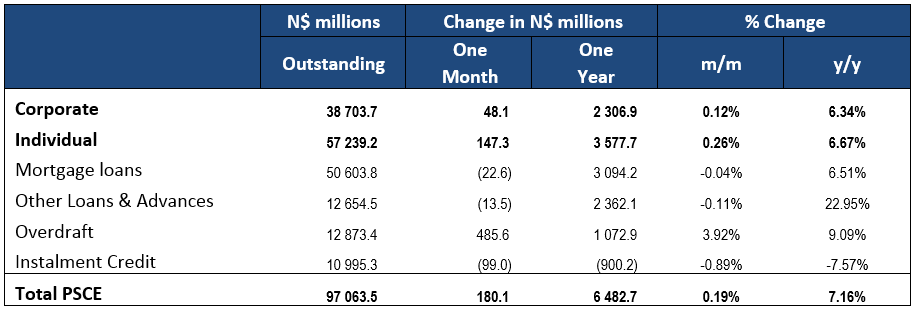

Total credit extended to the private sector (PSCE) decreased by N$4.3 million from a revised N$97.984 billion cumulative credit outstanding in February to N$97.979 billion in March. This is the first time since June 2017 that we have seen a month-on-month contraction in credit extension. On a year-on-year basis, private sector credit extension grew by 5.79% in March, compared to 6.93% recorded in February. N$2.05 billion worth of credit has been extended to corporates and N$3.42 billion to individuals on a 12-month cumulative basis, while the non-resident private sector has decreased their borrowings by N$112.9 million.

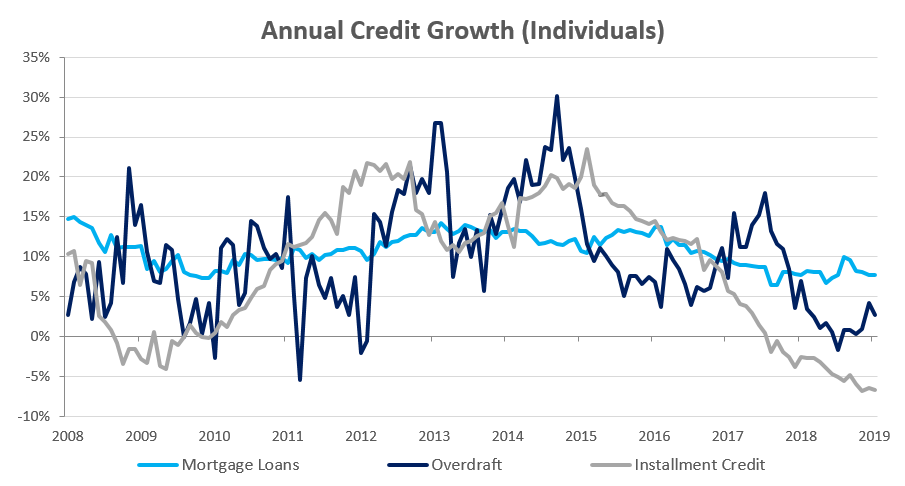

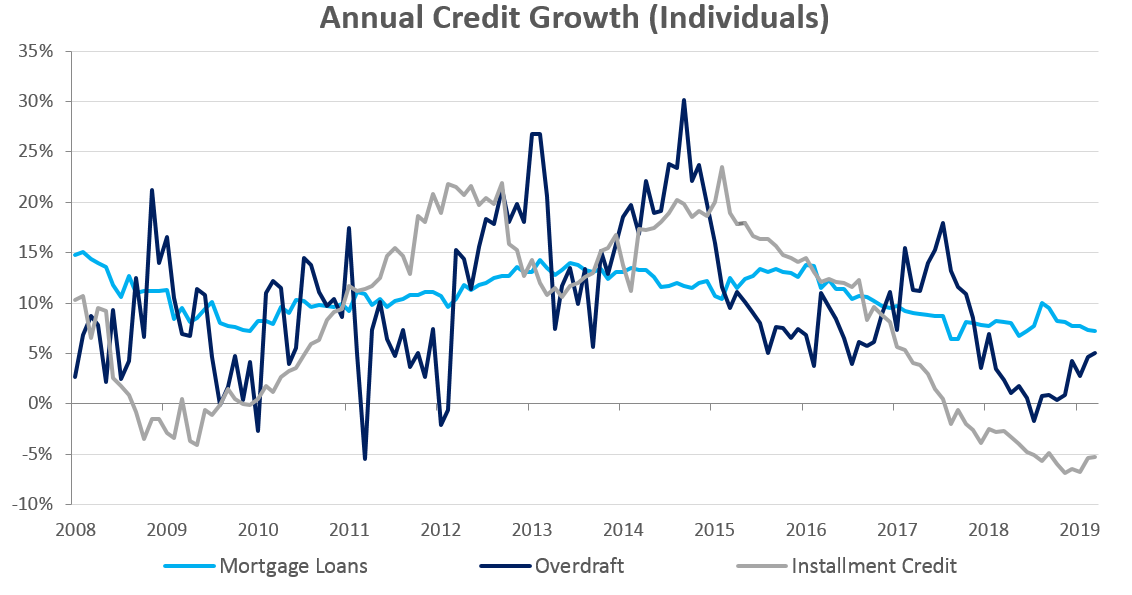

Credit Extension to Individuals

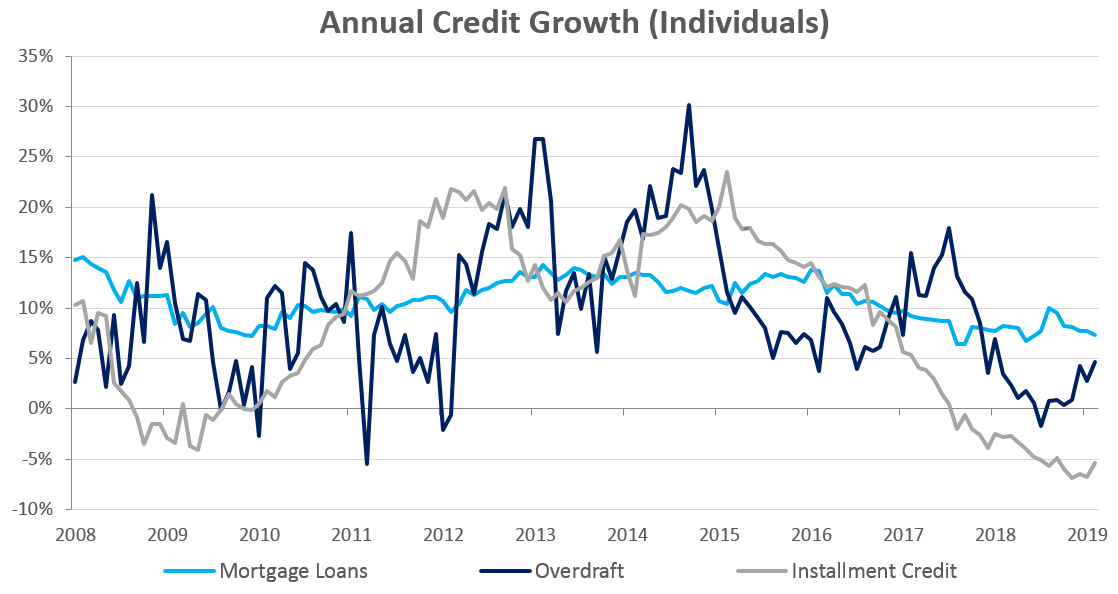

Growth in credit extension to individuals moderated to 0.1% m/m and 6.3% y/y, compared to 7.0% y/y growth recorded in February. Installment credit remained depressed, contracting by 0.6% m/m and 5.2% y/y. Individuals started to repay their overdrafts, resulting in a decline of 1.4% m/m, but increase of 5.0% y/y. Growth in mortgage loans remained at a similar rate as in February, increasing by 0.4% m/m and 7.2% y/y. Other loans and advances recorded growth of 2.9% m/m and 20.4% y/y.

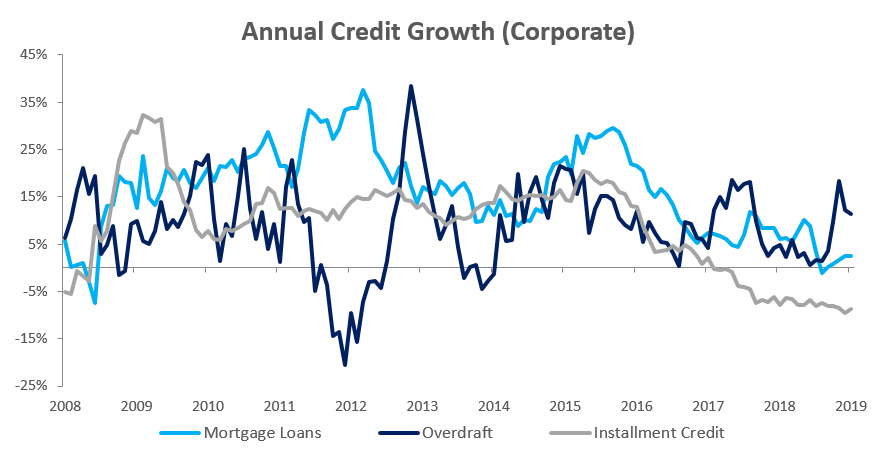

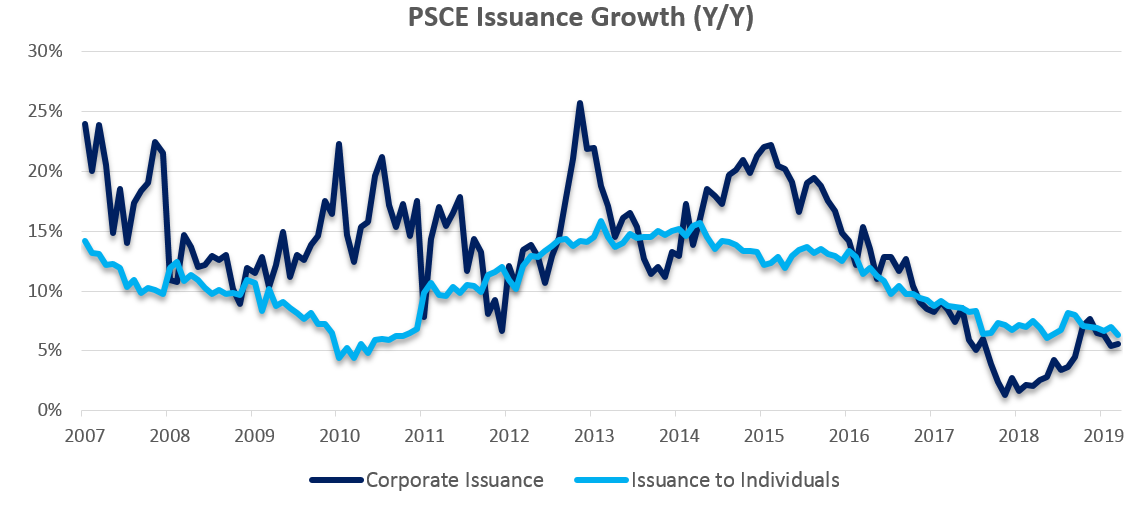

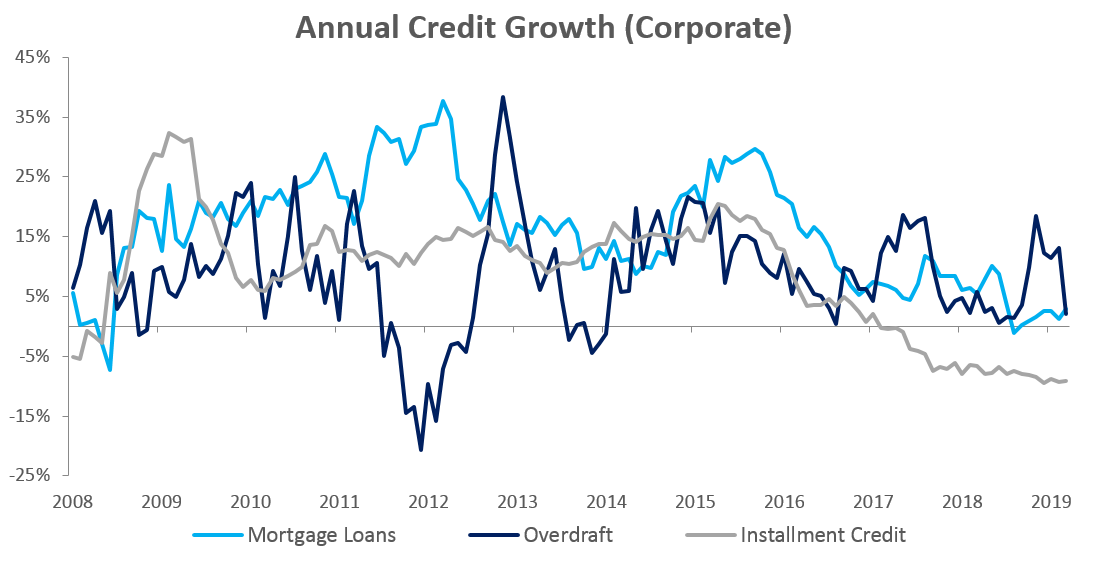

Credit Extension to Corporates

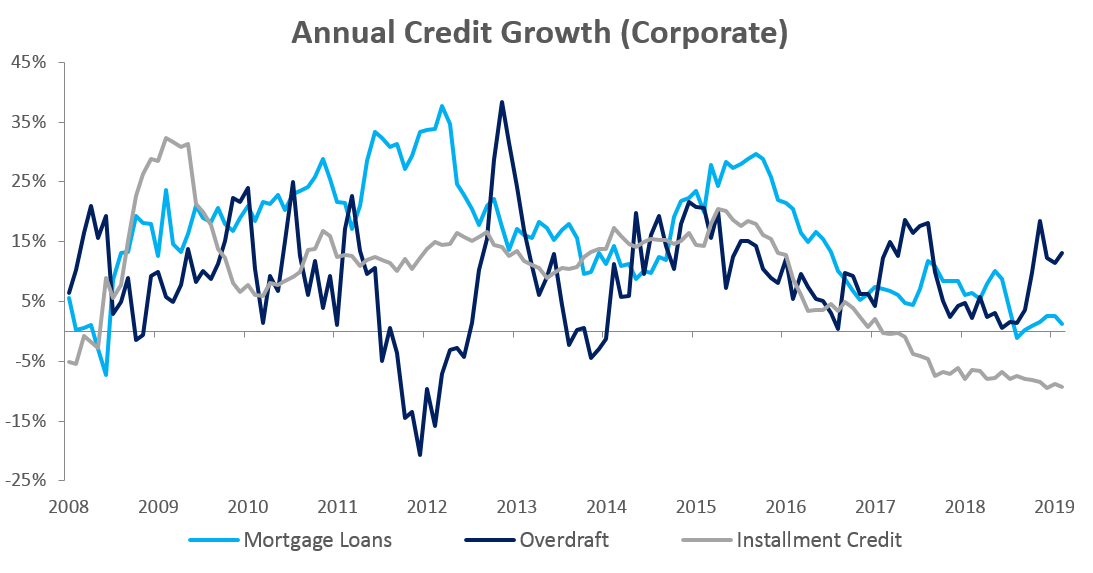

Credit extended to corporates contracted by 0.2% m/m in March after increasing by 1.0% m/m in February. On an annual basis credit extension to corporates increased by 5.5% y/y in March. The month-on-month contraction is mostly caused by businesses paying back overdrafts. Overdraft facilities extended to corporates decreased by 7.5% m/m, but increased by 2.0% y/y. Mortgage loans to corporates contracted by 1.8% m/m, but increased 2.9% y/y. Installment credit extended to corporates, which has been contracting since February 2017 on an annual basis, remained depressed, contracting by 0.6% m/m and 9.1% y/y in March.

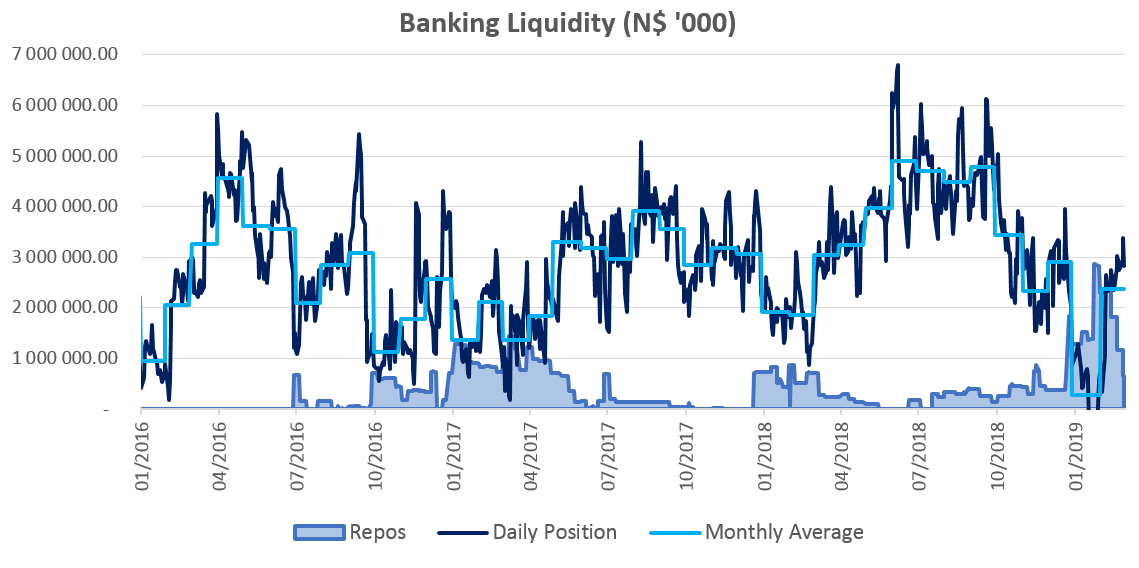

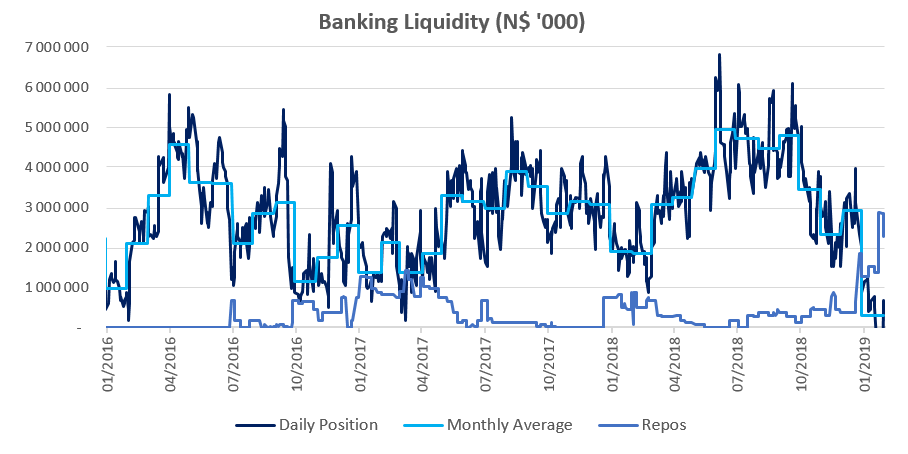

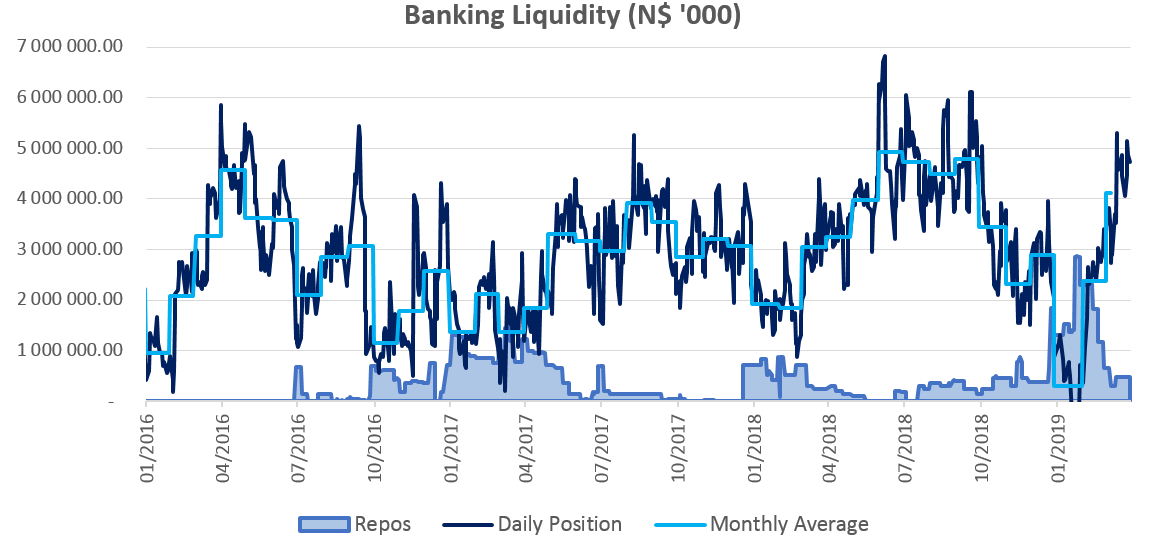

Banking Sector Liquidity

The overall liquidity position of commercial banks improved during March, increasing by N$1.74 billion to reach an average of N$4.11 billion. According to the Bank of Namibia (BoN), the increase is attributable to increased mineral sales proceeds as well as higher government expenditure which, it says, is customary towards the end of a fiscal year. The higher liquidity resulted in a further decrease in use of the BoN’s repo facility by commercial banks, with the outstanding balance of repo’s decreasing from N$645.7 million at the start of March to N$479.3 million by month end.

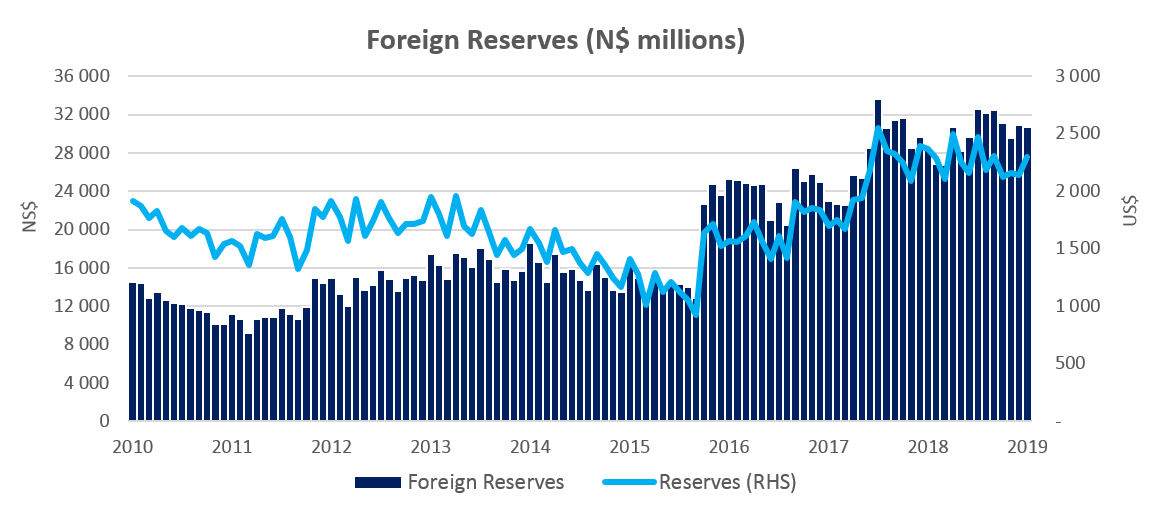

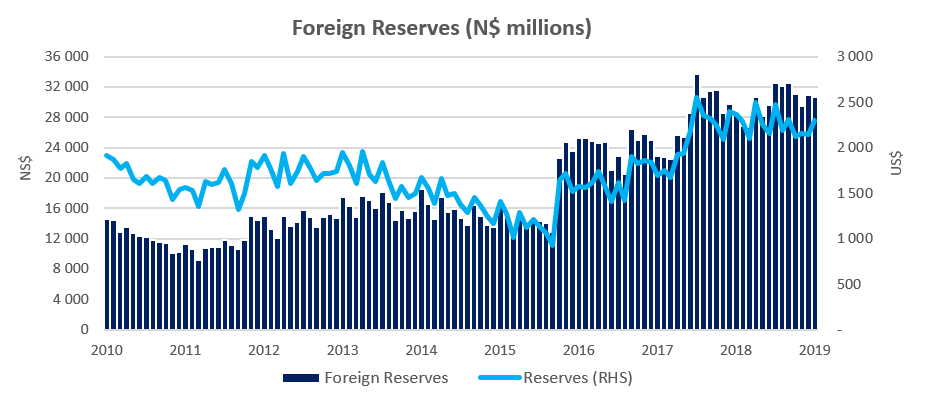

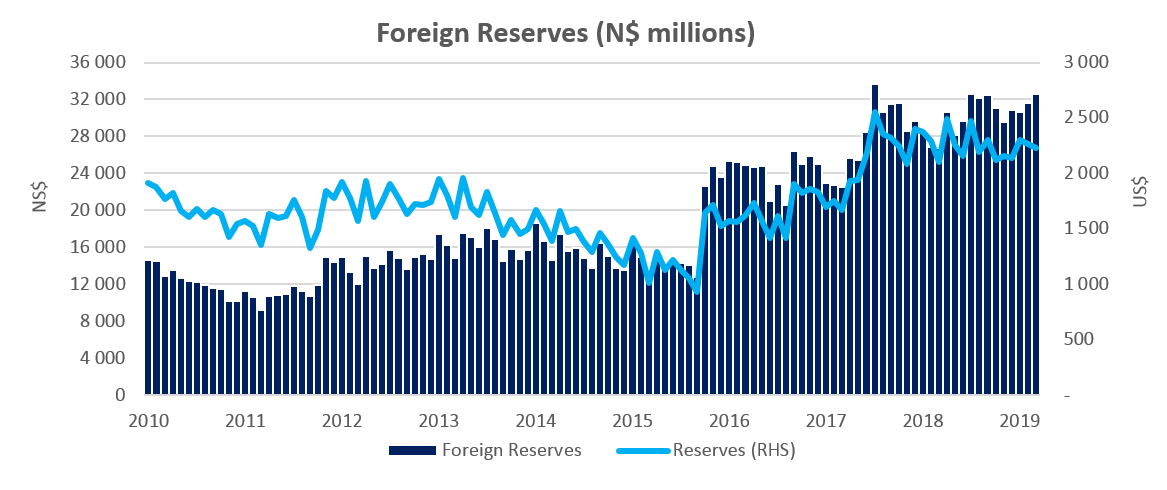

Reserves and Money Supply

As per the BoN’s latest money statistics release, broad money supply rose by N$6.74 billion or 6.9% y/y in March following a 10.5% y/y increase in February. Foreign reserve balances rose by 3.0% m/m to N$32.6 billion in March. The BoN stated the increase is solely due to the depreciation of the Namibian dollar against the US dollar. The Namibian dollar depreciated by 3.0% against the US dollar during March reaching N$14.50/US$ at the end of the month. The rand (and subsequently the Namibian dollar) has been relatively volatile since May 2018 as a result of rising interest rates in the US, political uncertainty in South Africa caused by the upcoming election, and continuous bailouts of SOE’s by the South African government.

Outlook

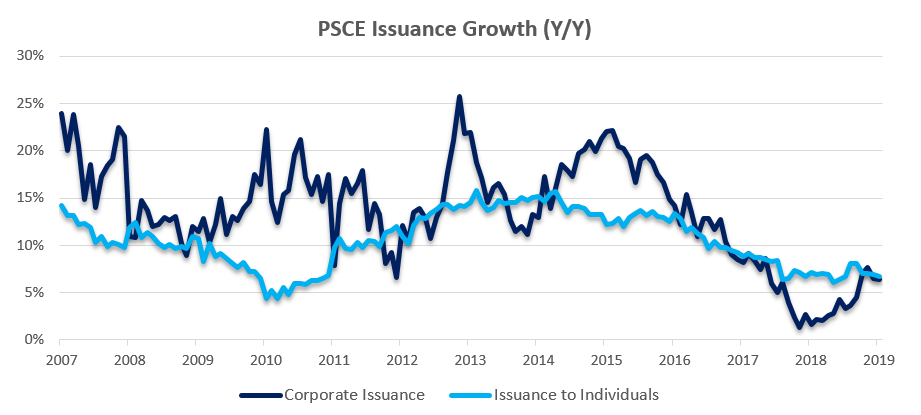

Private sector credit extension remained depressed at the end of March, increasing by only 5.8%, with annualised growth slowing for a fourth consecutive month. From a 12-month rolling perspective, credit issuance is down 0.3% from the N$5.37 billion issuance observed at the end of March 2018, with individuals taking up most (63.9%) of the credit extended over the past 12 months.

Both individuals and corporates have started repaying overdraft facilities during the month, resulting in a 6.0% decrease in total overdrafts. As we have stated in the past, short-term borrowing satisfies short-term needs and as such, the repayment of overdrafts is a positive sign in our view as extension of overdraft facilities was unlikely to drive meaningful expansion of productive capacity.