Overall

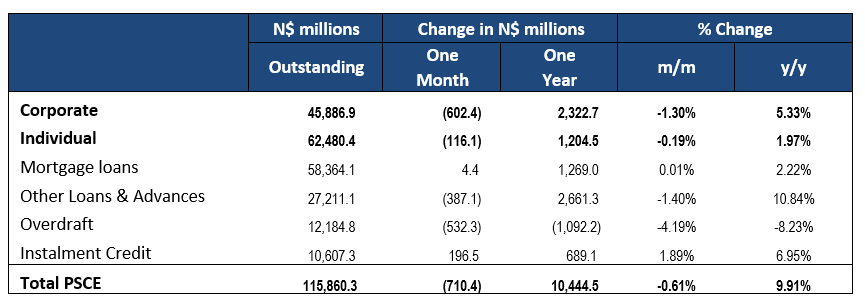

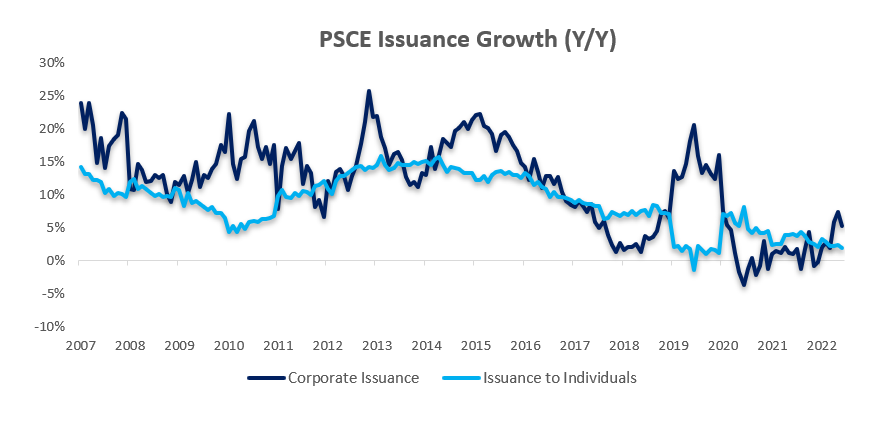

Private sector credit (PSCE) rose by N$342.9 million or 0.3% m/m in July, bringing the cumulative credit outstanding to N$116.2 billion. On a year-on-years basis, private sector credit grew by 10.6% y/y. Normalising for the large increases in claims on non-resident private sectors observed between January and March this year sees PSCE growth at 3.5% y/y. Cumulative credit extended to the private sector over the last 12-months amounted to N$11.1 billion, up 287.2% y/y over the same period last year (26.7% y/y on a normalised basis). Claims on non-resident private sectors have taken up the bulk of the issuance with debts over the past 12 months summing to N$6.97 billion or 63% of the total debt issuance, followed by corporates which took up N$2.84 billion (or 26%) and individuals at N$1.32 billion (12%).

Credit Extension to Individuals

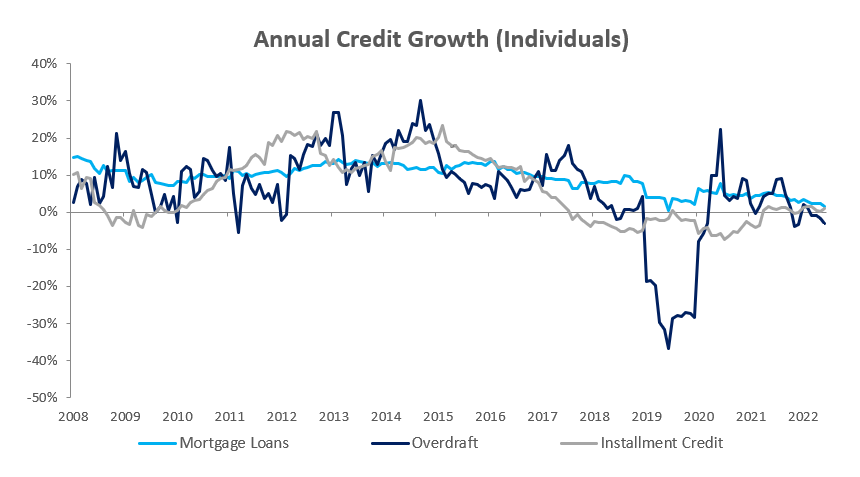

Credit extended to individuals increased by 0.1% m/m and 2.2% y/y in July, due to an increased demand in mortgage credit and ‘other loans and advances’ according to the BoN. Mortgage loans to individuals rose by 0.4% m/m and 1.9% y/y. Other loans and advances (consisting of credit card debt, personal- and term loans) increased 1.0% m/m and 7.9% y/y. Annual growth in other loans and advances to individuals has steadily been ticking up since November last year, with July’s print the quickest since October 2020. Overdraft facilities however contracted by 7.8% m/m and 10.7% y/y, following a 2.1% m/m and 3.0% y/y contraction in June.

Credit Extension to Corporates

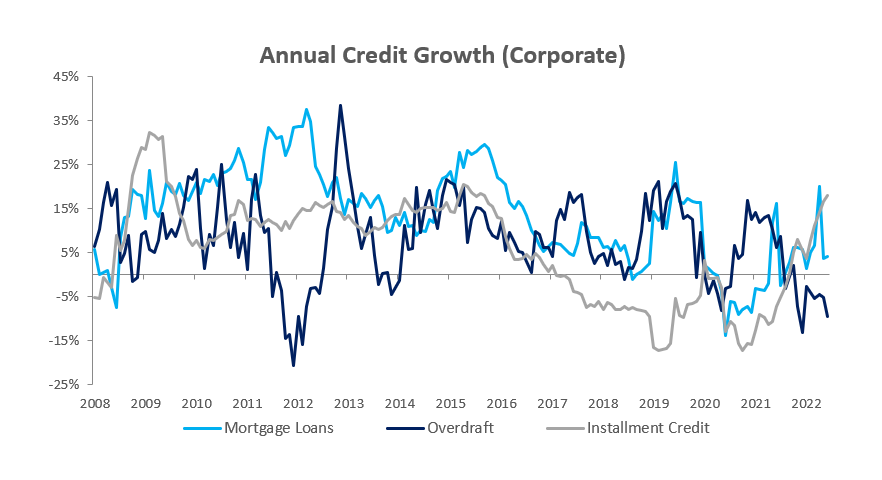

Credit extended to corporates contracted by 6.5% y/y in July, following the 5.2% y/y increase recorded in June. On a month-on-month basis, credit extension to corporates rose by 0.7% m/m. According to the BoN, the increase was due to a rise in demand for mortgage credit and other loans and advances from corporates in the mining-, health-, and services sectors. Mortgage loans contracted by 1.0% m/m but rose 4.6% y/y while other loans and advances rose by 0.01% m/m and 15.7% y/y. Instalment credit increased by 1.6% m/m and 14.9% y/y. Overdrafts rose by 4.1% m/m but fell 6.1% y/y, the ninth consecutive month that overdraft facilities to corporates recorded a decline on an annual basis.

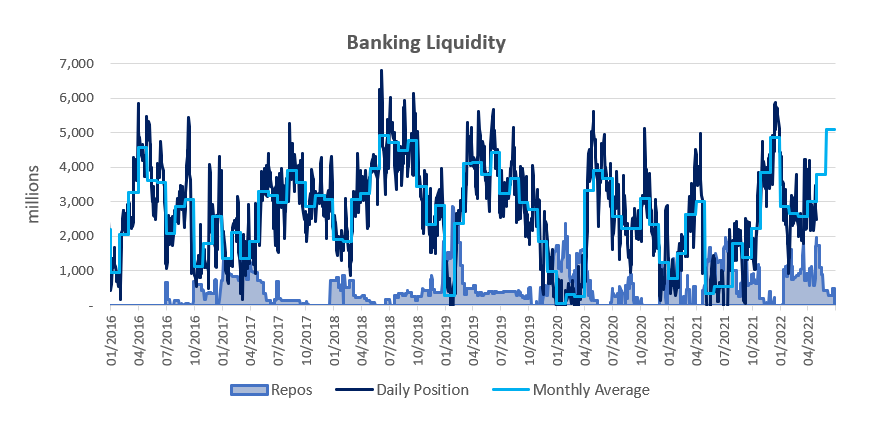

Banking Sector Liquidity

The overall liquidity position of the commercial banks rose significantly in July, rising by N$1.4 billion to an average of N$6.5 billion, and ended the month at N$10.2 billion. According to the BoN, the increase is partly attributed to an increase in diamond sales proceeds and from investment liquidations by other non-banking financial corporations. The repo balance subsequently fell to N$293.0 million at the end of the month, after ending at N$488.0 million in June.

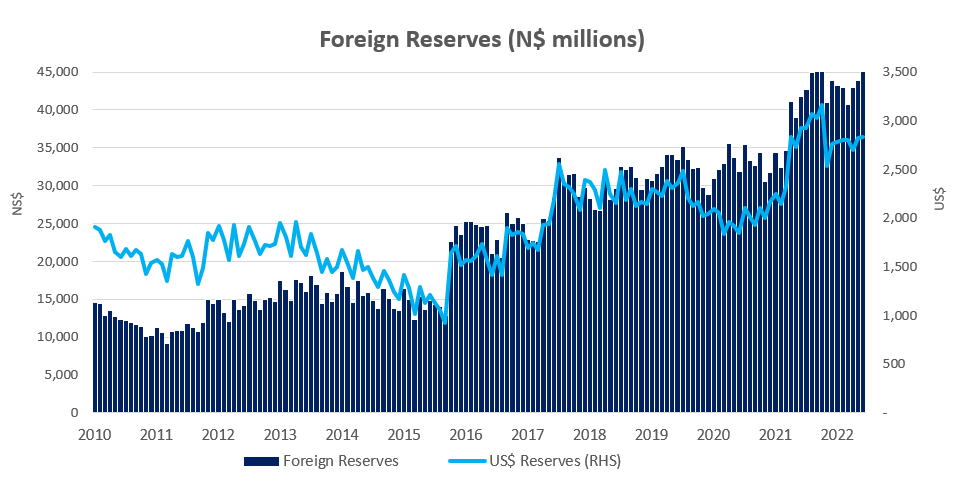

Reserves and Money Supply

The Bank of Namibia’s latest figures show Broad Money Supply rising significantly by N$6.5 billion or 11.0% y/y to N$134.9 billion in July. The increase in the M2 growth was ascribed to a rise in the net foreign assets of depository corporations, as well as growth in domestic claims on other sectors. Foreign reserves rose by 7.1% or N$3.3 billion, the quickest growth in 13 months, to N$49.2 billion. The BoN attributes the boost to the increase in commercial banks foreign currency and SACU receipts.

Outlook

Normalised PSCE growth has steadily been ticking up from the lows of 2021, but remains about half the rates seen prior to the pandemic. With economic activity expected to remain relatively muted over the short- to medium term, we do not expect to see drastic increases in PSCE growth soon. We do however expect to see additional rate hikes by both the SARB and the BoN over the coming months, as inflationary pressures remain high.

Ultra-accommodative interest rates over the past two years provided relief to indebted consumers, but did not stimulate credit uptake, as evidenced by the low PSCE growth figures since the start of the Covid-19 pandemic when the central bank aggressively cut rates. Even with another 75 – 100 bp worth of increases, local interest rates will still be accommodative by historical standards. We could possibly see commercial banks being more willing to extend credit in the rising interest rate environment as they experience margin expansion, provided that they do not expect non-performing loans to increase.