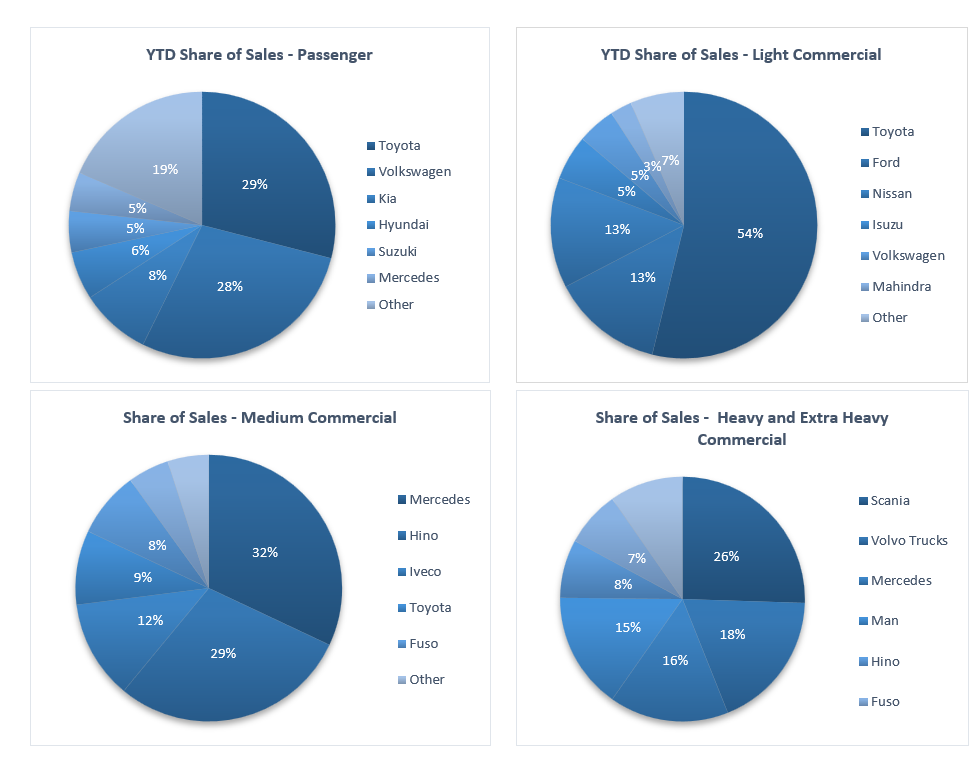

On a

year-to-date basis, Toyota maintained its dominance in the light commercial

vehicle space with a 53.8% market share, Ford climbed to second place with

13.5% of the market, followed by Nissan, with a market share of 13.4%. Mercedes

leads the medium commercial vehicle segment with 32.0% of sales year-to-date. Scania

remained number one in the heavy and extra-heavy commercial vehicle segment

with 25.5% of the market share year-to-date.

June was a respectable month for new

vehicle sales, despite a raging third wave of Covid-19 infections in the

country, coupled with the introduction of new lockdown restrictions. An average

of 379 new passenger vehicles were sold per month in the first half of 2021, which

is well above the average of 254 in the comparable period of 2020, but still

trails slightly below the average of 411 in the first 6 months of 2019. On the

commercial front, total commercial vehicle sales in the first half of the year

are 31.7% higher than the comparable period in 2020, with light and medium

commercial vehicle sales increasing by 25.6% and 22.0% year-on-year,

respectively, while heavy commercial vehicle sales recorded the largest

increase of 114.4% y/y. Despite these increases, the commercial sector lags

well behind the comparable period’s 10-year pre-Covid-19 average (2010-2019)

when total new commercial vehicle sales were 50.1% higher than they are now.

Overall, this reflects a long path to recovery in the commercial sector.

The City of

Windhoek approved a total of 187 building plans in May, representing a 25.2%

m/m decrease from the 250 building plans approved in April. In monetary terms,

the approvals were valued at N$173.0 million, a 26.1% m/m decrease. 183

buildings with a value of N$67.13 million were completed during May, a 27.9%

m/m decrease in value terms. Year-to-date building approvals are 66.3% and 24.8%

higher in number and value terms, respectively, than during the same period in

2020. This increase is however mostly due to stagnant construction activity during

the lockdown last year. Year-to-date, the number of completed buildings

increased by 23.3% y/y to 678, while the value of these completions fell marginally

by 3.6% y/y from N$380.0 million in 2020 to N$366.5 million in 2021. On a

twelve-month cumulative basis, 2,684 buildings with the value of N$2.01 billion

were approved, an increase of 47.7% y/y in number, and 10.7% y/y in value.

In May, 105 additions to properties

were approved with a value of N$55.4 million,

while 125 additions worth N$28.1 million were completed during the month, as

the category continues as the main contributor to the total approvals and

completions. Additions to properties approved fell 36.7% m/m in number and

40.4% m/m in value terms.

New

residential units were the second largest contributor to the total number of

building plans approved in May, and the largest contributor in value terms. 78

new units worth N$92.6 million were approved in May, representing a 28.5% m/m decrease

from the N$129.5 million worth of approvals in April. On a 12-month cumulative

basis, residential units approvals recorded a 125.3% y/y increase in value. 58 new

residential units worth N$39.0 million were completed during the month,

representing an increase in value of 17.7% m/m, but

a decrease of 21.6% y/y.

Four new commercial units, valued at

N$25.0 million, were approved in May, translating to a 115.3% m/m increase in

value terms. Year-to-date, there have been sixteen commercial building

approvals valued at N$51.1 million, which is 33.3% lower in number terms and a 79.3%

decrease in value terms compared to the same period last year. On a rolling

12-month perspective, the number of commercial and industrial approvals have

slowed to 33 units worth N$135.3 million as at May, compared to the 56 approved

units worth N$652.9 million over the corresponding period a year ago. No

commercial and industrial units were completed in May.

Private sector credit (PSCE) fell by N$214.2

million or 0.20% m/m in May, bringing the cumulative credit outstanding to

N$105.0 billion. On a year-on-year basis, private sector credit grew by 2.66%

in May, compared to the 2.74% y/y growth recorded in April. On a rolling

12-month basis, N$2.72 billion worth of credit was extended to the private

sector. N$2.34 billion worth of credit has been extended to individuals on a

12-month cumulative basis, while N$498.1 million was issued to corporates. The

non-resident private sector decreased their borrowings by N$112.2 million.

Credit

Extension to Individuals

Credit extended to individuals increased by 3.98%

y/y in May, compared to the increase of 3.91% y/y recorded in April. On a

monthly basis, household credit grew by 0.1%, following the increase of 0.6%

m/m recorded in the previous month. Mortgage demand by individuals was

unchanged on a monthly basis but rose 5.2% y/y. Instalment credit increased by

0.4% m/m and 1.5% y/y, the second consecutive month of increase on an annual

basis, following twenty consecutive months of decline. Overdraft facilities

extended to individuals increased 1.1% m/m, but increased by 5.1% y/y. Other

loans and advances (OLA) rose by 0.2% m/m and 1.3% y/y, displaying a slightly

faster rate of increase from the 0.8% y/y growth recorded in April.

Credit

Extension to Corporates

Credit extension to corporates contracted for a fourth

consecutive month declining by 1.2% m/m, following the 0.8% m/m contraction

recorded in April. On an annual basis, growth in credit extension to corporates

slowed to 1.2% y/y in May, compared to the 2.1% y/y growth registered in April.

On a monthly basis, growth in mortgage loans, other loans and advances (OLA)

and overdraft facilities extended to corporates were all stagnant. On a

year-on-year basis, mortgage loans contracted 2.4%, while OLA and overdrafts

increased 1.4% and 14.9% respectively.

Banking

Sector Liquidity

The overall liquidity position of commercial

banks deteriorated substantially during May, decreasing by N$2.7 billion to

reach an average of N$340.8 million. The BoN attributed the diminishing liquidity

position to net transfers by investment managers as well as several

cross-border transfers during the period under review. The outstanding balance

of repo’s subsequently rose to N$1.1 billion at the last week of the month.

Reserves and Money Supply

As per the BoN’s latest money statistics release, broad money supply contracted by N$1.6 billion or 1.3% y/y in May, compared to the 3.1% y/y increase recorded in April. Foreign reserve balances declined by N$2.2 billion to N$39.0 billion in May. The BoN ascribed the decrease to an increase in government payments as well as foreign currency repurchases by commercial banks.

Despite the historically low interest rates, economic

activity remains subdued, with individuals unwilling or financially incapable

of taking out loans to increase consumption, and corporates who lack

confidence to invest in capital projects would rather use the opportunity to

de-lever their balance sheets. With Namibia experiencing a third wave of

Covid-19 infections, and with it, stricter lockdown measures which hampers

economic activity, credit extension is unlikely to improve in the short-term.