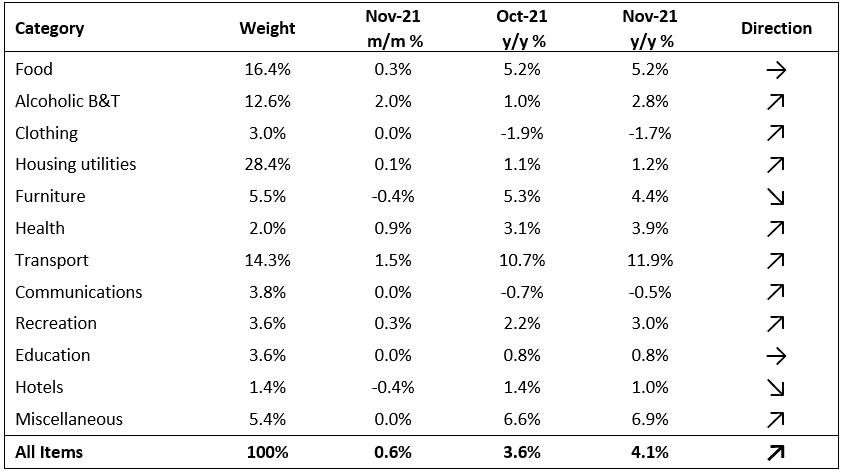

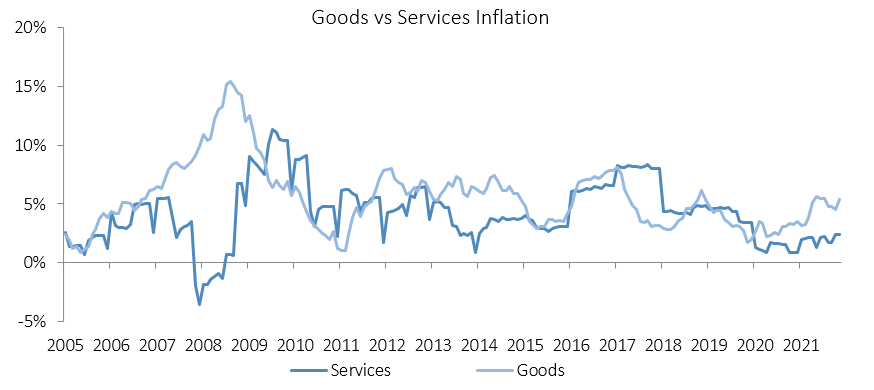

Namibia’s annual inflation rate rose to 4.5% y/y in December, with prices in the overall NCPI basket increasing by 0.4% m/m. The annual average inflation rate for 2021 was 3.6%, compared to 2.2% in 2020 and 3.7% in 2019. Year-on-year, overall prices in three of the twelve categories rose at a quicker rate in December than in November, six categories experienced disinflation and three categories posted steady inflation. Prices for services rose by 2.7% y/y and prices for goods rose by 5.8% y/y.

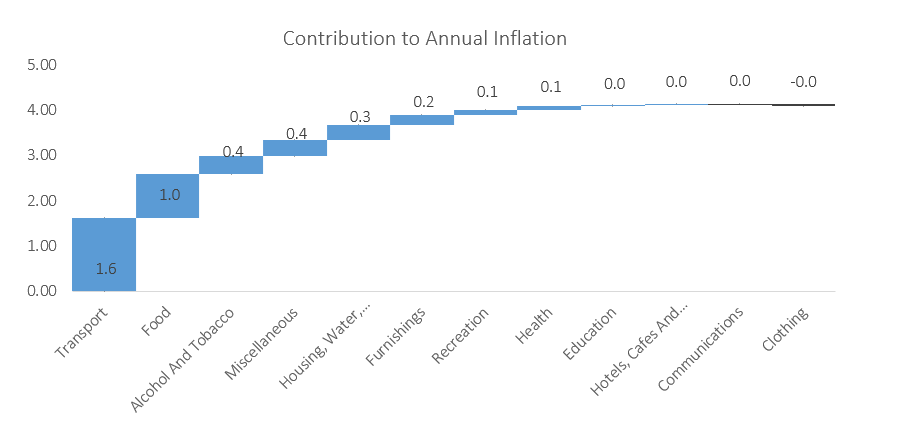

Transport continues to be the largest contributor to annual inflation, with prices in this category increasing by 2.1% m/m and 14.3% y/y. This basket item contributed 2.0 percentage points to the annual inflation rate in December. Prices in two of the three sub-categories recorded price increases, with the “operation of personal transport equipment” increasing by 19.7% y/y. This is mostly attributable to a 36.1% y/y increase in the price of petrol and diesel. This was the largest year-on-year increase in fuel prices for 2021. Current forecasts are that global oil prices will continue to increase this year with some analysts predicting that a lack of production capacity and limited investment in the sector will result in demand outstripping supply. We thus expect fuel prices to remain elevated for the majority of 2022.

Food & non-alcoholic beverages was the second biggest contributor to the annual inflation rate in December, contributing 0.9 percentage points. Prices in this basket item remained steady on a monthly basis but increased by 5.1% y/y. Only one sub-category, vegetables, recorded a decrease in prices on an annual basis of 1.1%. The twelve other sub-categories all recorded price increases on an annual basis. Fruit prices increased by 14.9% y/y, oils and fats by 11.9% y/y and meat prices by 11.8%.

Alcohol & Tobacco inflation accelerated from 2.8% y/y in November to 3.8% y/y in December and was the third-largest contributor to December’s annual inflation rate. The prices of tobacco products rose by 0.8% m/m and 6.2% y/y, while the prices of alcoholic beverages increased by 0.4% m/m and 3.2% y/y.

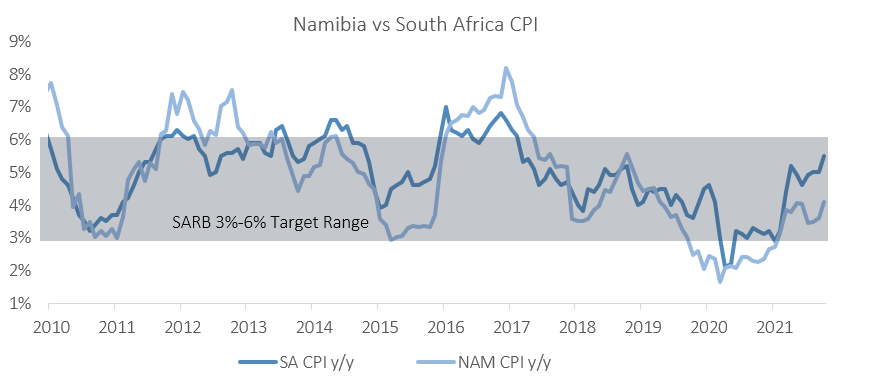

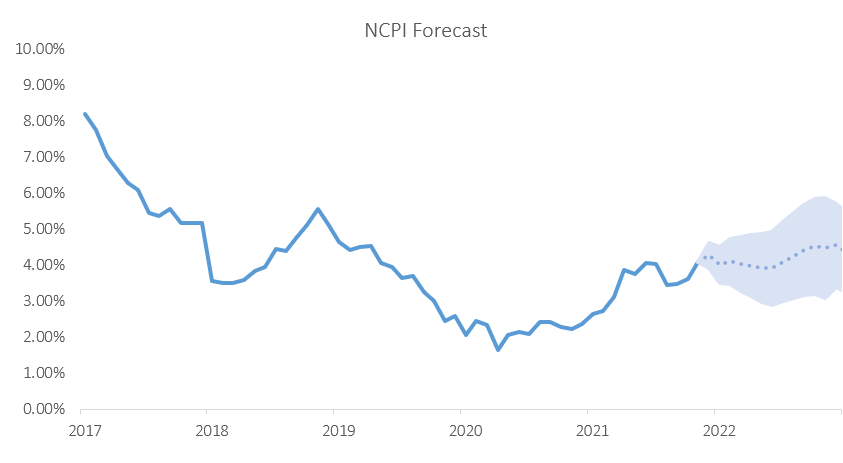

The 4.5% y/y annual inflation rate for December was in line with IJG’s average inflation forecast of 4.3% y/y for the month. IJG’s inflation model forecasts an average inflation rate of 4.3% y/y in 2022 and 3.5% in 2023. Following the SARB’s 25 basis point hike last year, South Africa’s inflation rate accelerated to 5.5% y/y in November, uncomfortably close to the SARB’s upper bound of 6.0% y/y. The MPC committee will meet again on 27 January, which will set the stage for the BoN’s next meeting scheduled for 16 February. We expect the BoN to follow suit on any rate decisions made by the SARB.