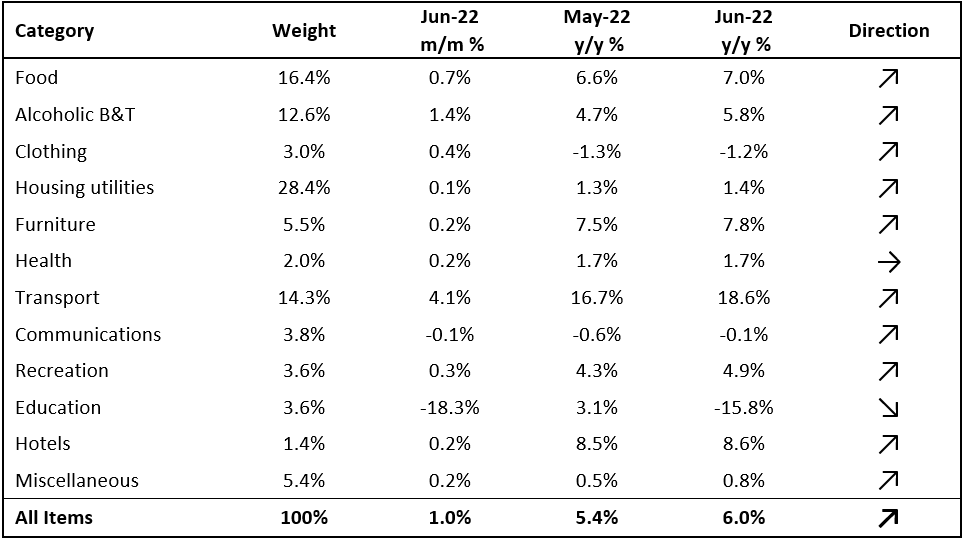

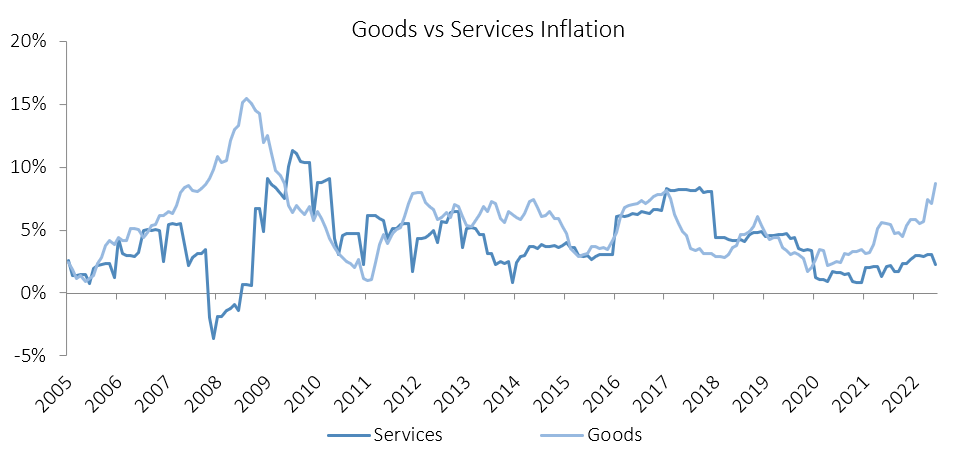

Namibia’s annual inflation rate rose to 6.0% y/y in June, following the 5.4% y/y increase in prices recorded in May. June’s CPI print was the highest since June 2017. Prices in the overall NCPI basket rose by 1.0% m/m. On a year-on-year basis, overall prices in ten of the twelve basket categories rose at a quicker rate in June than in May, one recorded a slower rate and one remained steady. Prices for goods increased by 8.7% y/y, the quickest increase in 13 years, while prices for services increased by 2.2% y/y.

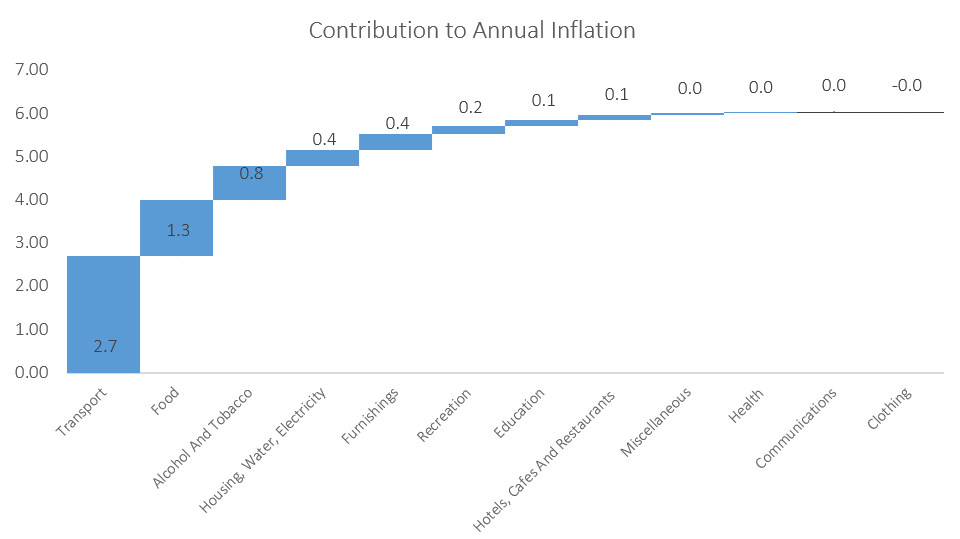

Transport was unsurprisingly again the largest contributor to the annual inflation rate in June, contributing 2.7 percentage points to the annual inflation rate. The category recorded price increases of 4.1% m/m and 18.6% y/y. All three sub-categories in this basket recorded increases on a month-on-month basis with the operation of personal transport equipment sub-category recording the largest increase in prices of 6.4% m/m and 32.0% y/y on the back of the Ministry of Mines and Energy’s decision to increase fuel at the beginning of June. Petrol prices rose by 250 cents per litre and diesel increased by 150 cents per litre, resulting in fuel price inflation reaching 56.9% y/y in June. The purchase of vehicles sub-category recorded inflation of 0.6% m/m and 4.4% y/y. Prices of public transportation services rose 0.01% m/m, in line with last month’s rate, but fell 4.2% y/y. Transport inflation is expected to remain elevated over the short- to medium-term as July saw another fuel price increase by the Ministry of Mines and Energy and the temporary drop in fuel levies are expected to be reversed in August. Global crude oil prices have retreated somewhat from the highs recorded in June, but the weakness in the South African rand has offset some of this.

Food & non-alcoholic beverages was the second biggest contributor to the annual inflation rate in June, contributing 1.3 percentage points. Overall, prices in this basket item rose 0.7% m/m and 7.0% y/y. As seen in prior months, all thirteen sub-categories in this basket recorded price increases on an annual basis. The largest increases were recorded in the prices of oils and fats which rose by 26.2% y/y, followed by fruit, which recorded an increase of 18.1% y/y. According to the United Nations’ FAO Food Price Index, which measures the monthly change in international prices of a basket of food commodities, prices fell by 2.3% m/m in June but is still 23.1% higher than a year ago. This was a third consecutive decline, and could potentially lead to lower local food prices, should the international trend continue.

Alcohol & tobacco inflation quickened from 4.7% y/y in May to 5.8% y/y in June. On a month-on-month basis, prices in the basket rose by 1.4%. The prices of alcoholic beverages increased 1.7% m/m and 5.9% y/y while tobacco prices fell by 0.1% m/m but rose by 5.0% y/y.

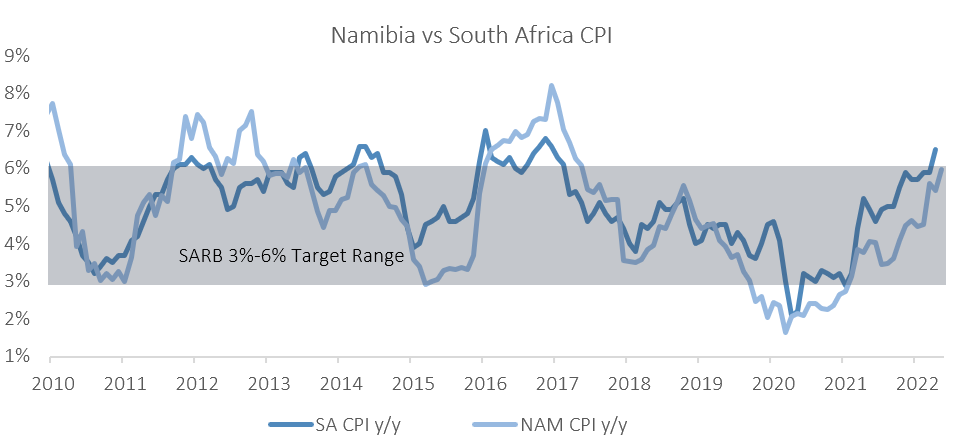

Namibia’s annual inflation rate continues to trend above its 12-month average of 4.5%. Transport inflation alone accounted for nearly half (45%) of the inflation print in June with rising fuel prices driving most of the increase. Inflationary pressures are expected to remain high for the rest of the year. The low services inflation print points to subdued domestic economic activity and again indicates that inflation is very much supply side driven at present. South Africa’s inflation rate of 6.5% in May breached the SARB’s 3-6% target band for the first time since 2017 and will mean that we can expect to see further rate hikes by the SARB’s MPC. We expect the BoN to respond in kind to any rate decisions taken by the SARB. IJG’s inflation model currently forecasts inflation to average between 5.9% and 6.3% in 2022.