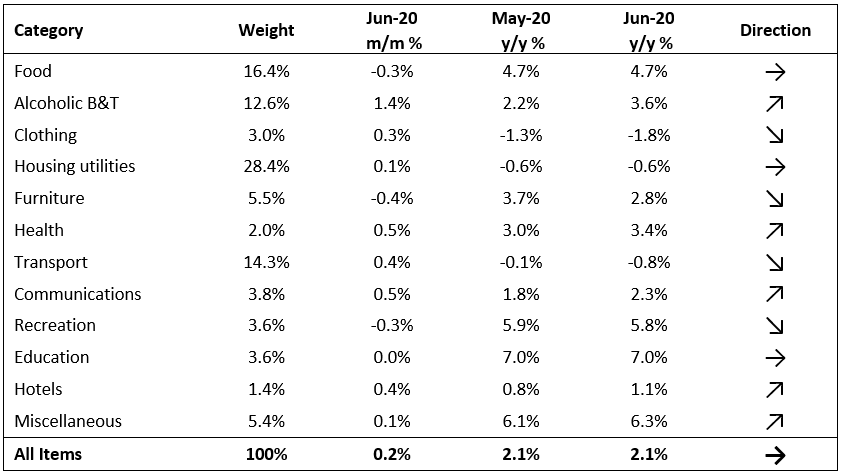

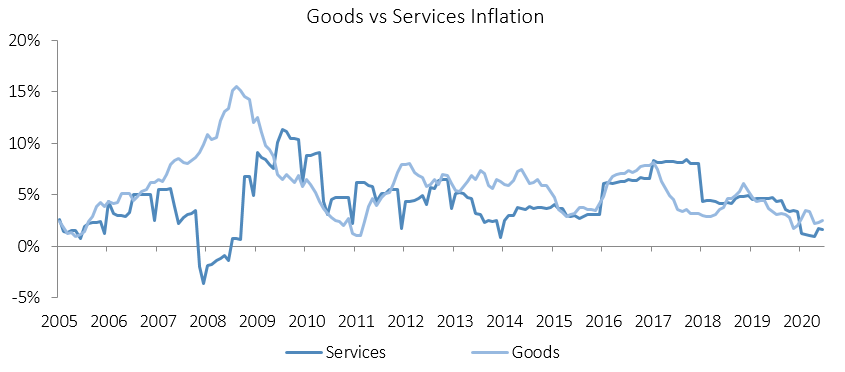

The Namibian annual inflation rate remained at 2.1% in June, unchanged from May. On a month-on-month basis, prices increased by 0.2%, following the 0.4% m/m increase in May. Overall, prices in five of the twelve basket categories rose at a faster annual rate than during the preceding month, four at a slower rate and three grew at a steady pace. Price for goods rose by 2.5% y/y in June, while prices for services grew by 1.6% y/y.

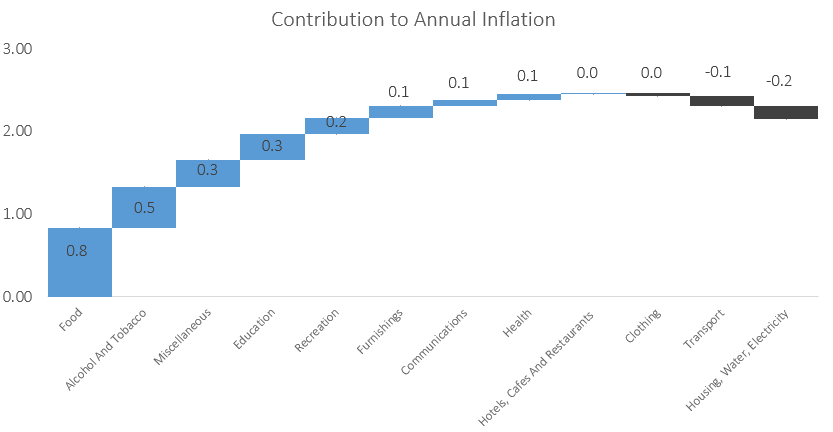

The food & non-alcoholic beverages category displayed prices decreases of 0.3% m/m, but an increase of 4.7% y/y in June, making it the largest contributor to annual inflation, accounting for 0.84 percentage points of the total 2.1% annual inflation rate. Prices in twelve of the thirteen sub-categories recorded increases on a year-on-year basis. The largest increases were observed in the prices of fruit which increased by 21.2% y/y and vegetables which increased by 11.7% y/y. The price of bread and cereals saw price decreases of 0.9% y/y.

The alcoholic beverages and tobacco basket item was the second largest contributor to the annual inflation rate in June, with prices of the basket item increasing by 1.4% m/m and 3.6% y/y. Prices for tobacco products decreased by 0.3% m/m, but increased 3.9% y/y. The prices of alcoholic beverages meanwhile rose by 1.8% m/m and 3.6% y/y.

The miscellaneous goods & services basket recorded inflation of 0.1% m/m and 6.3% y/y, and contributed 0.32 percentage points to the overall annual inflation figure. Only two subcategories showed price increases on a month-on-month basis, with personal effects increasing by 0.4% m/m and personal care rising by 0.2%. Prices in all the subcategories remained steady during the month.

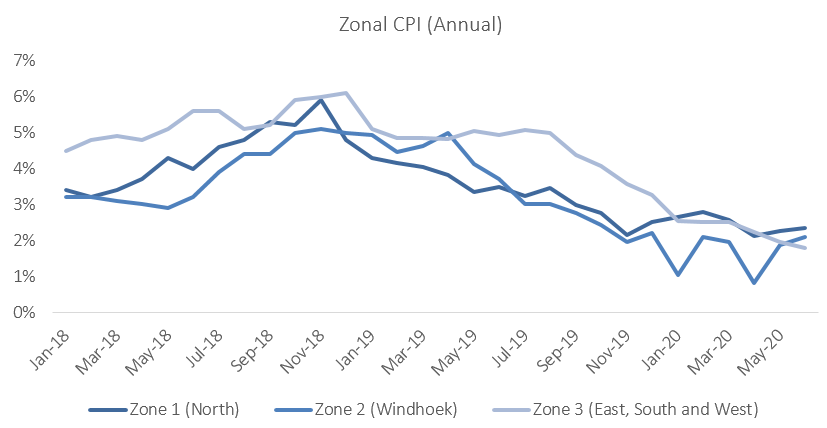

The NSA’s regional CPI data shows that on a monthly basis prices increased by 0.2% in the northern zone 1, 0.2% in the central zone, and 0.1% in the mixed eastern, southern and western zone. On an annual basis the northern region recorded the highest inflation rate at 2.3% y/y in June, followed by the central zone at 2.1% y/y and the mixed zone 3 at 1.8% y/y.

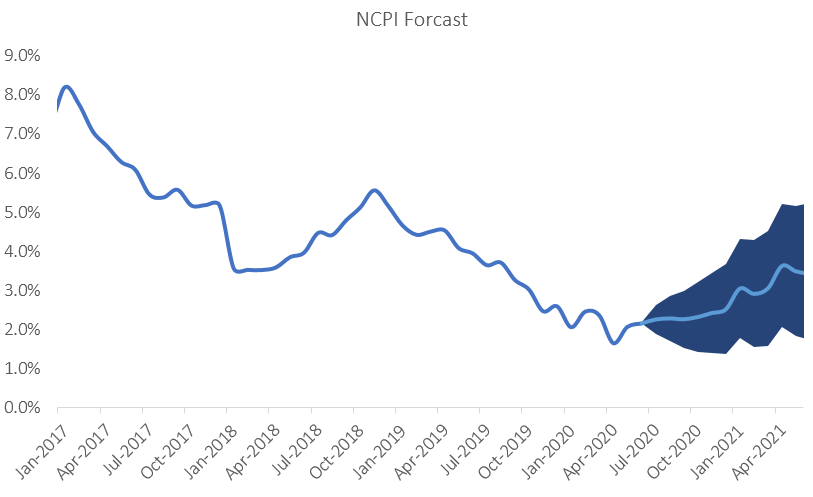

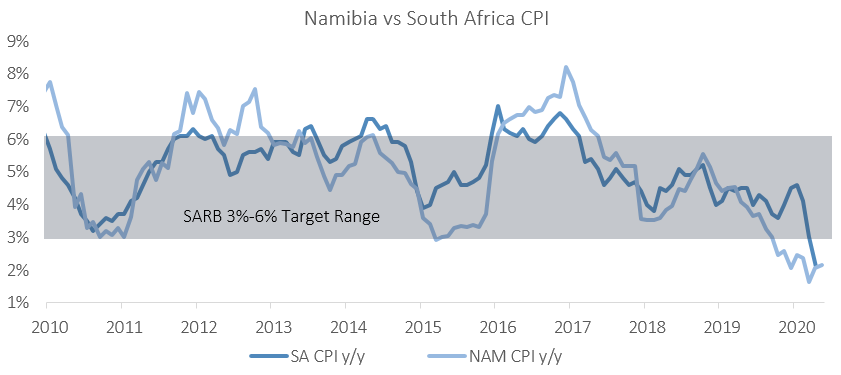

Namibian annual inflation at 2.1% in June remains benign as economic activity remains weak after the relaxation of the lockdown restrictions, and is on par with South Africa’s May inflation figure of 2.1% y/y. South Africa’s inflation has breached the lower end of the SARB’s 3-6% target range in April, and remained at or below the 4.5% midpoint for 18 consecutive months. If the SARB expects inflation to trend at current levels for some time, it could decide to cut interest rates further. The market currently expects the SARB to cut rates by 25-50 basis points at its July MPC meeting next week, although a 25-basis point cut is more likely in IJG’s view. Regardless of the outcome, we expect the BoN to follow the SARB’s at its August MPC meeting, as Namibian inflation will likely remain muted for at least the rest of the year. IJG’s inflation model forecasts an average inflation rate of 2.2% y/y 2020 and 3.8% in 2021. The biggest risk to this forecast is fuel price increase due to the steady increase in the international oil price.